Stable subscriptions, slow advertising: What Q3 reveals about TV industry

The quarter reflects a clear trend across television ecosystem: subscription revenues are proving more stable for broadcasters, while advertising remains uneven and closely tied to FMCG demand cycles

by

by

Published: Feb 9, 2026 8:57 AM | 6 min read

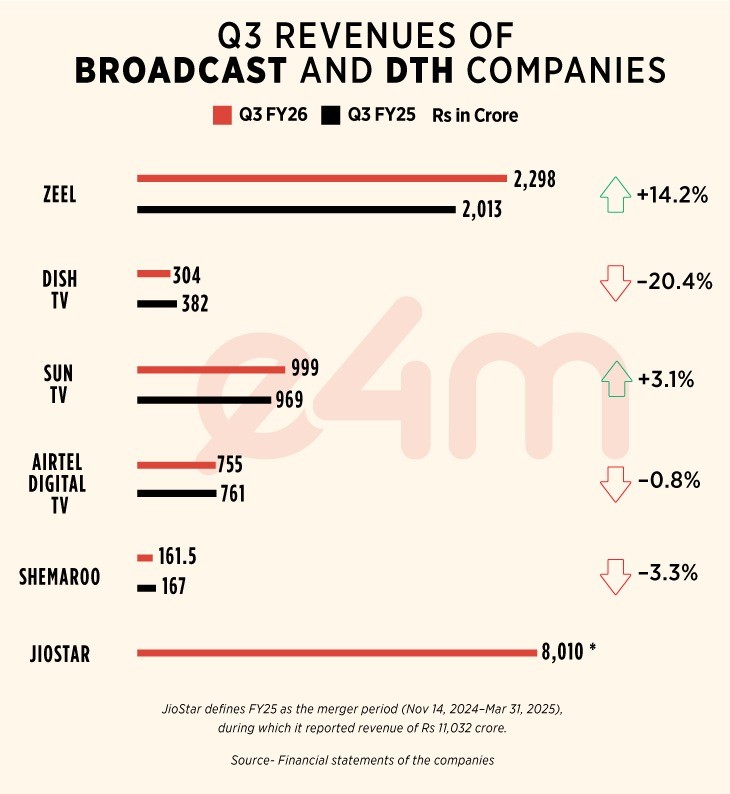

India’s television broadcast and distribution sector delivered a mixed financial performance in the third quarter of FY26, with modest revenue growth at broadcasters such as Zee Entertainment Enterprises (ZEEL) and Sun TV Network offset by continued pressure on advertising and deepening stress in the direct-to-home (DTH) segment. While subscription income offered some stability for general entertainment networks, a broader slowdown in FMCG-led ad spends and persistent cord-cutting trends weighed heavily on traditional linear and satellite TV businesses.

ZEEL reported a steady quarter, with total revenue rising to ₹2,298 crore in Q3 FY26 from ₹2,013 crore in the year-ago period, marking a 14.2% increase. The growth was led by subscription revenues, which climbed 6.9% to ₹1,050 crore from ₹982 crore. Advertising revenue, however, declined 9.4% year-on-year to ₹852 crore compared with ₹940 crore, reflecting the continued softness in the ad market.

Read: Zee’s Q3 FY26 revenue up 15% YoY to Rs 2,280 cr

The company had earlier flagged that the previous year’s festive quarter saw muted advertising momentum, with broad consumption weakness, especially in FMCG, dampening spends across urban and Hindi-speaking markets. ZEEL noted that while there was a pickup around Diwali, demand tapered off soon after, keeping ad growth under pressure even as its OTT platform ZEE5 and linear subscription base provided support.

Sun TV Network, too, posted only marginal top-line growth amid similar headwinds. Total income for Q3 FY26 stood at ₹999 crore, up 3.1% from ₹969 crore a year ago. Subscription revenue rose 8.7% to ₹473 crore from ₹435 crore, but advertising income fell 12% to ₹292 crore from ₹332 crore, underscoring the industry-wide slowdown in brand spending.

Read: Sun TV Q3 ad revenue stands at nearly Rs 292 cr

Rising costs further squeezed profitability at the broadcaster. Quarterly expenses increased 11.4% to ₹558 crore, while profit declined 11% to ₹324 crore. EBITDA dropped 5.2% to ₹409.79 crore, indicating margin pressure despite stable revenues. For the nine-month period, revenue grew 10.8% to ₹3,918 crore, but expenses surged at a faster pace, climbing 25.4%, dragging overall profitability lower. The company’s performance highlighted a clear divergence between relatively resilient subscription streams and volatile advertising income.

JioStar, formed after the merger of Disney Star and Reliance’s media assets, emerged as the largest player by scale, but it does not disclose advertising and subscription revenues separately. The company reported total revenue of ₹8,010 crore in Q3 FY26. For FY25, defined as the merger period from November 14, 2024 to March 31, 2025, the company had recorded gross revenue of ₹11,032 crore, making direct year-on-year quarterly comparisons difficult.

Read: JioStar posts Rs 8,010 cr revenue in Q3; 9-month revenue crosses Rs 26,000 cr

However, during the earnings call, JioStar CEO-Entertainment, Kevin Vaz said the TV advertising market remains under pressure due to FMCG and consumer electronics spend cuts, but December showed encouraging post-GST recovery signs.

“Our operating revenue for the quarter, a strong Rs 6,896 crores, an EBITDA of Rs 1,303 crores. A healthy EBITDA performance in spite of a tough macroeconomic environment. A strong performance in subscription revenue across both digital and TV," he had said.

“The TV ad market continues to be challenging due to spend cuts from FMCG and consumer electronics. But the good part is post-GST, December month has shown great signs of recovery, and we are hoping that continues as we go forward. Lastly, it is not fair to compare year to a year comparison, as the previous quarter we started the merger only from November 14th. So, we have had strong momentum growth sustained despite the macroenvironment conditions,” Vaz said.

JioStar reported a revenue of Rs 8,010 crore in Q3 FY26 and Rs 26,464 crore for the nine-month period ended FY26. In the preceding quarter, Q2 FY26, the company had posted a revenue of Rs 7,232 crore.

Sun TV too offers DTH service but the financials do not disclose its earnings separately.

In contrast to broadcasters, DTH operators continued to grapple with structural challenges as subscribers migrate to OTT and broadband-led bundled services.

Dish TV’s numbers reflected this stress sharply. Total revenue fell 20.4% year-on-year to ₹304 crore in Q3 FY26 from ₹382 crore. Subscription revenue, its core income stream, plunged 32.2% to ₹224.5 crore from ₹331.1 crore. Advertising revenue nearly doubled to ₹4.8 crore from ₹2.5 crore, but the increase was too small to materially offset the steep decline in subscriptions.

Read: Dish TV’s ad income jumps 92% in Q3 FY26; subs rev falls 32%

Higher costs compounded the pain. Total expenditure jumped 36.1%, pushing the company to a loss of ₹276.2 crore, compared with a loss of ₹46.5 crore last year. Management said it is repositioning the business toward hybrid offerings that combine live TV, OTT and smart features, alongside deeper integration of its Watcho platform and creator monetisation initiatives, as it seeks to remain relevant in a rapidly evolving home entertainment market.

Bharti Airtel’s Digital TV arm painted a similar picture. Revenue remained largely flat at ₹755 crore in Q3 FY26 versus ₹761 crore last year, but the business slipped further into the red, reporting a loss of ₹63.7 crore. For the nine months, it posted a loss of ₹112 crore compared with a profit in the same period last fiscal. The company has been shifting focus to IPTV and converged home services while tightening subsidies and costs to improve cash flows, even as subscriber attrition continues in the satellite TV segment. Airtel does not separately disclose advertising and subscription revenues for its DTH business.

Shemaroo Entertainment’s performance underscored how ad weakness is disproportionately hurting smaller and traditional media players. The company reported a 3.3% decline in total revenue to ₹161.5 crore in Q3 FY26 from ₹167 crore a year earlier. While it does not break out advertising and subscription income, management said softer ad revenues affected overall performance. Its digital media segment grew 13.8% year-on-year to ₹80.7 crore, but the traditional business fell 14.4% to ₹80 crore.

Higher expenses led to an EBITDA loss of ₹67.4 crore and a net loss of ₹54.9 crore for the quarter, both wider than last year. The company attributed the weakness partly to reduced FMCG advertising, the re-entry of major broadcasters on DD FreeDish, and a crowded sports calendar diverting budgets. It remains cautiously optimistic about a gradual recovery in ad spends in the coming quarters.

Taken together, the quarter reflects a clear trend across the television ecosystem: subscription revenues are proving more stable for broadcasters with strong channel portfolios, while advertising remains uneven and closely tied to FMCG demand cycles. Meanwhile, DTH operators continue to face structural declines as viewers shift to digital platforms, forcing them to rethink their business models.

Read more news about Television Media, Digital Media, Advertising India, Marketing News, PR and Corporate Communication News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News