How DPDP is redesigning India’s ad architecture

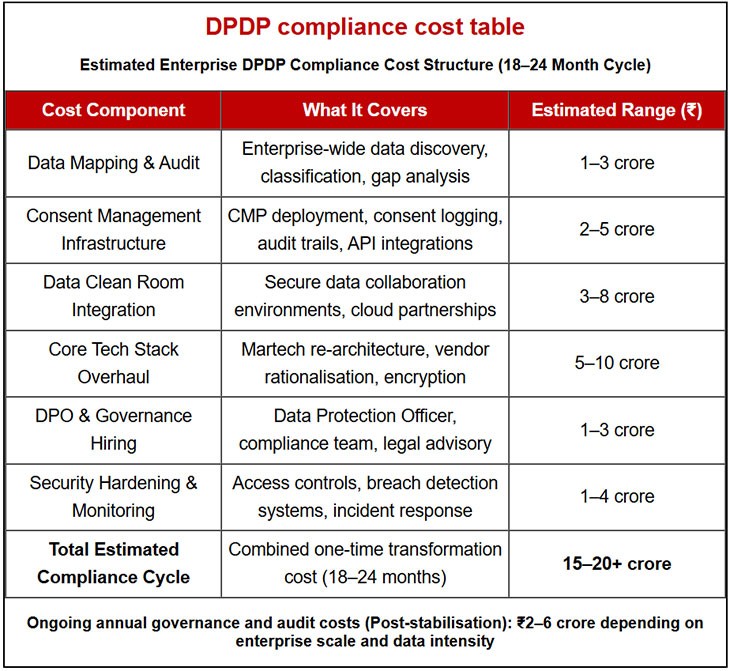

Industry estimates suggest that one-time DPDP compliance costs for large organisations could range between roughly ₹2.5 crore and ₹18 crore over an 18–24-month cycle

by

by

Published: Mar 4, 2026 8:51 AM | 8 min read

Now with its Wild West days truly in the rear-view mirror, India’s digital advertising economy is accelerating toward a trillion-rupee future. According to the Pitch Madison Advertising Report 2026, India’s total ad market reached ₹1,55,105 crore in 2025, with digital commanding roughly 60% of that pie, and is forecast to grow toward ₹1,11,976 crore (64%) in 2026 under its expanded definition.

This structural tilt toward digital underscores why compliance infrastructure now sits directly under the fastest-growing part of the economy.

And yet, before a single rupee of that expanding budget is deployed, large enterprises may need to invest cumulatively in the tens of crores simply to remain compliant.

Industry estimates suggest that one-time DPDP compliance costs for large organisations could range between roughly ₹2.5 crore and ₹18 crore over an 18–24-month cycle, with total investment figures in complex cases approaching ₹19 crore. Beyond individual firms, some industry forecasts peg aggregate compliance investments across India at nearly ₹10,000 crore over the next three years, underscoring the scale of infrastructure spending underway.

DPDP is no longer a legal sidebar. It is becoming a structural cost of entry into India’s fastest-growing advertising market.

This is not just a privacy story. It is a power story.

Shradha Agarwal, Co-founder and Global CEO of Grapes Worldwide, says the DPDP is forcing marketing and technology teams to align much earlier in the planning cycle. “Choices around data structure and user consent now directly affect how campaigns are designed and measured. Privacy systems are no longer background support; they influence media selection, partner decisions and attribution models,” she notes.

While large enterprises may have a scale advantage, she adds that disciplined data organisation will determine long-term competitiveness. “Ultimately, responsible data management, not just size, will define advantage.”

At a surface level, the compliance anatomy appears procedural. Enterprises are conducting full data-mapping exercises across departments, rebuilding consent management layers, deploying encryption and access controls, integrating data clean rooms, and hiring Data Protection Officers and compliance teams.

Technology stacks are being audited and, in many cases, re-engineered. Legacy third-party integrations are being renegotiated. Internal workflows for deletion requests, breach notifications and audit trails are being codified.

Over an 18–24-month window, these interventions can accumulate into a multi-crore transformation cycle. For conglomerates spending hundreds or thousands of crores annually on marketing, this is absorbable. For mid-market brands operating on tighter margins, it is transformational.

The context is critical. Digital is no longer experimental spend. At ₹71,621 crore in 2025 (as per the Dentsu-e4m Digital Advertising Report 2026) and climbing toward ₹98,000 crore by 2027, it is the centre of gravity for Indian advertising. As budgets consolidate into digital formats, the compliance burden consolidates there too.

The first power shift is from open experimentation to governed growth. When digital commands 60% of the ad pie and is heading toward 70%, governance becomes part of growth infrastructure rather than a bureaucratic hurdle.

Marketing decisions now pass through compliance architecture. Campaign design is shaped not only by audience insight but by consent provenance and data lineage. The internal balance of influence shifts. CMOs increasingly operate alongside CIOs, CISOs and legal heads as co-architects of data strategy.

Veteran marketer, Shubhranshu Singh says he sees DPDP less as a compliance burden and more as a structural reset. “As consent, first-party data and purpose limitation tighten, control will shift from platforms to brands that build direct consumer relationships. It fundamentally reshapes performance economics — and in my view, that’s an important shift.”

The second shift strengthens walled gardens. Online video and social, each holding roughly 29% of digital spend, are deeply tied to logged-in identity environments. As consent management and data-sharing obligations tighten under DPDP, brands gravitate toward ecosystems where identity is already structured, consent is platform-managed and data remains within controlled environments.

Bhushan Kadam, Senior Vice President – Creative & Strategic Initiatives at White Rivers Media, says brands can no longer collect data “just in case.”

“Every data point now requires purpose-specific consent, which shifts budgets toward channels with verifiable consent trails,” he explains. “MarTech stacks are consolidating around platforms with integrated consent dashboards to reduce vendor risk and simplify compliance.”

The operational friction of compliance makes closed systems comparatively attractive. The open web, long dependent on loosely stitched third-party signals, faces higher scrutiny and heavier governance overhead.

The third shift is from data arbitrage to data fortressing. FMCG, the largest digital spending category at over ₹23,000 crore (as per Dentsu-e4m), depends heavily on targeting precision and measurement efficiency. Under DPDP, free-flowing exchanges of user-level data between brands, agencies and third-party vendors become riskier and more auditable. Data clean rooms move from pilot projects to structural infrastructure. Instead of sharing raw datasets, parties reconcile insights within secure, permissioned environments.

A senior marketing leader at a large FMCG company, who did not wish to be named, says the shift is already visible in planning cycles. “The focus has moved from data accumulation to data discipline. Consent documentation and internal data flows now require the same rigour as financial controls. It slows things initially, but cleaner permissioning ultimately improves retail data reliability and attribution confidence.”

Other marketers contacted by this reporter declined to comment at present because brands' DPDP playbooks are still being developed.

Cloud providers and clean-room vendors gain leverage as gatekeepers of compliant collaboration. Data brokers operating in regulatory grey zones face structural pressure.

The fourth shift creates a compliance moat. A ₹15–20 crore compliance cycle is manageable for a conglomerate allocating hundreds of crores annually across media. It is not trivial for a mid-sized advertiser. As digital approaches ₹98,000 crore and beyond, the barrier to compliant participation rises.

Enterprises that can invest in robust first-party data systems, clean rooms and governance frameworks consolidate advantage. Smaller brands become more dependent on platform-native tools and packaged audience solutions. Vendor consolidation accelerates. DPDP becomes a filtering mechanism within the ecosystem.

The fifth shift is from media-heavy marketing to infrastructure-heavy marketing. For years, the dominant narrative around digital growth revolved around creative velocity, influencer scale and performance optimisation. DPDP introduces a parallel cost centre.

Consent orchestration systems, audit trails, encryption layers, deletion workflows and breach response protocols now sit beneath campaign execution. In some organisations, privacy infrastructure spend over a two-year period may rival major campaign production outlays. Marketing begins to resemble regulated industries in its process discipline.

It is tempting to frame this transformation through the lens of statutory penalties, which can run into hundreds of crores for significant breaches. But fines are only the boundary condition. The deeper driver is systemic risk. Investors, boards and global partners increasingly expect demonstrable data governance. Campaign stoppages, vendor suspensions and reputational damage carry commercial consequences that are harder to quantify but no less material.

The macro numbers from the dentsu-e4m report sharpen the stakes. When digital is adding double-digit growth and pulling away from traditional media, any structural shift in how digital operates has outsized consequences.

Online video and social are not peripheral formats; they are nearly three-fifths of digital’s core.

FMCG and e-commerce are not niche advertisers; they are foundational pillars of the ecosystem. If DPDP alters targeting pools, measurement fidelity or data-sharing norms in these segments, the ripple effects extend across agencies, adtech vendors and publishers.

There is also a quieter reallocation underway. As compliance budgets grow, total marketing envelopes do not necessarily expand proportionally. In many enterprises, the same overall budget must now accommodate both media outlay and infrastructure investment.

Some portion of what might have flowed into incremental performance campaigns is redirected toward governance layers and consent architecture. Over time, this could compress experimentation budgets, particularly for mid-tier brands.

Who benefits from this recalibration is becoming clearer. Large platforms with logged-in identity graphs stand to gain as advertisers prioritise controlled environments. Retail media networks operating within first-party data ecosystems become more strategically valuable. Cloud providers and clean-room vendors evolve from optional partners to structural enablers. Consultancies and system integrators with compliance implementation expertise find new demand.

Who faces pressure is less frequently acknowledged. Mid-market brands with limited technology budgets encounter higher relative entry costs. Lightweight performance agencies built on aggressive third-party targeting tactics must adapt. Independent data intermediaries operating in loosely governed corridors see their room to manoeuvre narrow.

India’s digital advertising market is expanding rapidly toward the ₹1 lakh crore mark. Growth remains robust. Innovation continues. But the cost of participation is changing.

DPDP is not shrinking the market. It is reorganising who controls it.

The multi-crore compliance cycle is not merely a regulatory adjustment. It is the new toll gate at the entrance to India’s digital growth story. Those who can invest in the infrastructure reshape the road ahead. Those who cannot must operate within the systems others design.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News