Why video advertising in India no longer has formats, only platforms

Video, optimised primarily for mobile screens, now sits at the centre of most digital strategies, regardless of whether brands label those budgets as awareness, performance, or commerce

by

by

Published: Feb 11, 2026 9:16 AM | 12 min read

For most of the last decade, video advertising in India was organised around formats. Television was where brands went for reach and legitimacy. Digital video promised targeting and measurability. Short-form was discovery-led. Long-form was reserved for storytelling and “serious” attention. Media plans were built by stacking these formats, each with a defined role in the funnel.

That organising logic has now quietly broken.

By 2026, video in India no longer behaves like a set of discrete formats that can be neatly slotted into a plan. It has become the default interface through which consumers discover products, evaluate trust, and increasingly, transact.

As a result, the question advertisers are grappling with is no longer which video format to invest in, but which platforms can do the most work with the least friction.

This is not a future trend. It is a planning reality that many marketers are already navigating, even if they continue to describe it using the language of an earlier era.

Format-end?

Formats once served as useful mental shortcuts. They helped simplify complexity and made internal decision-making easier. Television meant scale. Digital video meant precision. Mobile video meant performance. These distinctions held when consumption habits were segmented and platforms were specialised.

They hold far less in 2026.

Video now moves fluidly across screens and contexts. A single consumer might watch a long-form explainer on a phone in the morning, scroll through short clips during the day, and watch creator-led content on a connected television at night. From an advertiser’s perspective, these are no longer separate “video moments”. They are variations of the same attention stream.

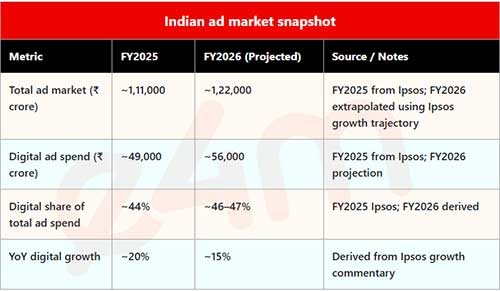

This shift is visible in where the money is going. India’s total advertising spends in FY2025 stood at roughly ₹1.11 lakh crore (with some estimates putting it as high as ₹1.8 lakh crore), growing at high double digits year-on-year.

Digital already accounts for about 44 per cent of this total, with projections taking it closer to half the market in FY2026.

Within digital, mobile dominates decisively, capturing nearly 78 per cent of all digital ad spends. Video, optimised primarily for mobile screens, now sits at the centre of most digital strategies, regardless of whether brands label those budgets as awareness, performance, or commerce.

What is striking is not just the growth of video, but the blurring of where video “belongs”. Television still commands a large share of total video budgets, but digital video is growing faster.

Mobile video attracts the bulk of incremental digital spends, while Connected TV is emerging as a creamy layer rather than a premium replacement.

Retail media is quietly absorbing video budgets that once sat in brand or social line items. Video is no longer being planned as a category; it is being distributed across surfaces.

As platforms collapsed distribution, measurement, and monetisation into single environments, formats began to lose their practical relevance. What was once a question of duration, placement, or screen increasingly became a question of surface ownership.

Indian mobility

India experiences this shift more sharply than many other markets because the transition is uneven.

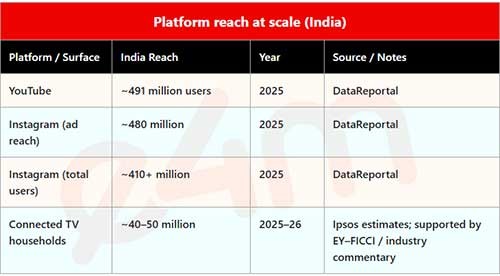

Mobile video continues to dominate reach, particularly outside the top metros. At the same time, connected TV usage is rising rapidly, driven by falling smart-TV prices and bundled OTT subscriptions. By the end of 2025, India had an estimated 40 million connected-TV users, with projections crossing 50 million in 2026. Advertising has followed, with the Indian CTV ad market crossing ₹1,300 crore in calendar 2025 and nearing ₹1,500 crore on a fiscal-year basis.

Short-form video is deeply saturated, while long-form consumption has quietly resurged in categories such as podcasts, education, news explainers, and vernacular content. Linear television continues to command mass reach, while retail media platforms are beginning to integrate video deeper into commerce environments.

The result is a compressed media ecosystem where multiple stages of video evolution coexist simultaneously. Indian advertisers are not choosing between old and new video. They are dealing with all of it at once.

In such a landscape, formats are less helpful as planning tools. Platforms, by contrast, offer a way to simplify complexity.

Platform Matrix

This is where convergence across platforms becomes impossible to ignore.

YouTube remains the clearest signal of this shift in India, not because it is the most experimental platform, but because it already sits at the intersection of search intent, habitual viewing, and creator trust. As of early 2026, YouTube reaches roughly 490 million users in India, making it the country’s largest video destination by a wide margin. Indian adults now spend well over an hour a day on the platform on average, across mobile screens and, increasingly, television screens.

Globally, YouTube’s scale continues to expand, with over 2.8 billion monthly users and Shorts generating more than 200 billion daily views. But what matters more in India is not the scale itself, but the behaviour it reflects. YouTube does not need to teach Indian users how to consume long-form video, how-to content, or creator-led programming. It simply formalises habits that already exist.

Other platforms are moving toward the same end state, even if they approach it from different directions. Social platforms such as Instagram have become discovery engines first and foremost, with Reels now dominating time spent and ad inventory. India alone accounts for over 480 million Instagram users reachable via ads, making it one of Meta’s most critical markets globally. While social video still leans heavily toward upper-funnel discovery, commerce integrations and performance overlays have steadily blurred that distinction.

OTT and streaming platforms, meanwhile, are circling back to advertising after years of subscription-led positioning. Ad-supported tiers, dynamic ad insertion, and experimentation with shoppable formats have made these platforms feel increasingly television-like in both consumption and monetisation. For advertisers, OTT is less a replacement for television than a premium extension of it, offering addressability layered onto familiar viewing behaviour.

Retail media platforms represent the next leg of convergence. E-commerce players in India generated over ₹15,500 crore in advertising revenues in FY2025, growing at over 25 per cent year-on-year.

Video has become an increasingly important part of these budgets, not as a storytelling device, but as a way to collapse discovery and purchase into a single interaction.

The result is not differentiation, but convergence. Platforms increasingly offer similar building blocks: scale, targeting, creator inventory, commerce hooks, and measurement. What differs is not the format they sell, but how seamlessly they connect attention to action.

Build-a-layer

What makes this convergence possible is not just distribution, but infrastructure.

Platforms now control the entire loop: creative inputs, delivery logic, optimisation signals, and success metrics. AI-assisted creative tools allow brands and creators to generate, localise, and iterate video at scale. Algorithmic distribution determines which videos surface, where, and for whom. Measurement frameworks increasingly sit within platform dashboards, not external systems.

This matters because formats once acted as constraints. A 30-second TV spot had a defined role and expectation. A six-second digital video had another. When platforms absorb those constraints into software, formats lose their policing function. What replaces them is optimisation logic (what performs, what scales, what converts) defined by the platform itself.

In India, where marketing teams are lean and scrutiny is high, this is not necessarily resisted. It is often welcomed.

Digital Feedback

For Indian advertisers, convergence has translated less into experimentation and more into consolidation.

Marketing teams are under pressure to deliver outcomes with fewer partners, fewer line items, and tighter accountability. Complexity, while attractive in theory, is difficult to defend in quarterly reviews. As a result, advertisers are quietly favouring platforms that can collapse multiple objectives into fewer decisions.

Instead of asking which video format drives awareness or which placement converts best, marketers are increasingly asking which platforms reduce friction across the entire journey. Platforms that promise reach, relevance, and measurable outcomes within a single ecosystem are easier to justify internally, even if that comes at the cost of diversity.

This shift is visible in budget behaviour. While television still commands a significant share of video ad spend, digital video continues to grow faster year-on-year. Mobile-led video attracts the bulk of incremental digital budgets, while connected TV is emerging as a premium layer rather than a replacement. Retail media, meanwhile, is absorbing video dollars that might once have been earmarked for standalone brand campaigns.

The common thread is not format preference, but platform confidence.

Caveat reader

There are trade-offs to this new normal.

As formats fade into the background, advertisers become more dependent on platform-defined measurement, optimisation, and creative norms. When platforms act as planners, distributors, and evaluators simultaneously, choice narrows. The ability to test alternative approaches, build independent audiences, or challenge platform logic becomes more constrained.

This does not mean the old model was better. It means the new model carries different risks.

Formats did not disappear because they failed. They disappeared because platforms absorbed their utility. What formats once offered as differentiation, platforms now offer as bundled capability.

TL; DR

In 2026, video advertising in India no longer lives in tidy silos. The funnel has flattened. Screens have blurred. Formats have lost their explanatory power.

What remains is a smaller set of powerful platforms competing to control the surface between attention and action. For advertisers, the strategic question is no longer how to optimise individual video formats, but how much dependence they are willing to place on the platforms that now define what video advertising even means.

That reality may be uncomfortable. But it is already here.

Platform scale vs format logic

The reason video formats have lost their usefulness as planning tools becomes clearest when advertisers compare platforms that were once seen as representing distinct video “types.”

For years, the industry treated platforms like Netflix and YouTube as proxies for fundamentally different formats. Netflix stood for premium, long-form, appointment viewing. YouTube was framed as everything else: short-form, creator-led, utility-driven. That distinction no longer explains how video is actually consumed or monetised, particularly in India.

YouTube now reaches roughly 470–490 million users in India, spanning income groups, geographies, and languages. Netflix’s Indian subscriber base, estimated at 16–20 million paying users, remains significant but structurally narrower by design. This gap is not simply about popularity. It reflects the limits of format-based thinking in a market where scale, frequency, and cross-screen continuity matter more than categorical purity.

The revenue data underscores this divergence. In 2025, YouTube crossed $60 billion in annual revenue globally, driven primarily by advertising, while Netflix’s global revenues stood in the mid-$40 billion range, overwhelmingly subscription-led. The gap reflects not just scale, but monetisation philosophy. YouTube is built to monetise attention at every layer; Netflix monetises commitment.

Usage data reinforces this shift. Indian adults spend over 72 minutes a day on YouTube on average, a level of engagement that rivals or exceeds traditional television for a majority of users. Crucially, this time is not confined to a single format. Long-form video, Shorts, podcasts, explainers, sports clips, and news content coexist within the same platform and often within the same viewing session.

The living room tells the same story. YouTube has become one of the most watched applications on connected TVs in India, with tens of millions of viewers consuming YouTube content on television screens. What would once have been classified as “mobile video” now comfortably occupies the same screen as premium OTT content, without requiring a change in buying logic or creative approach.

For advertisers, this erodes the usefulness of format distinctions. Planning for “long-form versus short-form” or “TV versus digital video” becomes less meaningful when the same platform delivers all of them, measured through a single system. Netflix, even with its growing ad-supported tier, remains tied to a specific viewing mode. YouTube is not. It absorbs multiple video behaviours and offers them back as a unified advertising surface.

This is the underlying reason video planning in India has shifted from format-led decisions to platform-led ones. Formats have not disappeared. They have simply stopped being the most relevant unit of organisation.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News