India’s ad spend to cross Rs 1.8 lakh crore this year; retail media growing fastest: TYNY

Retail media may cross Rs 30,000 Cr in 2026, capturing 15.0% of total ad revenue, linear TV viewership likely to fall at a mid-single-digit rate, says report

by

by

Published: Dec 8, 2025 8:20 AM | 5 min read

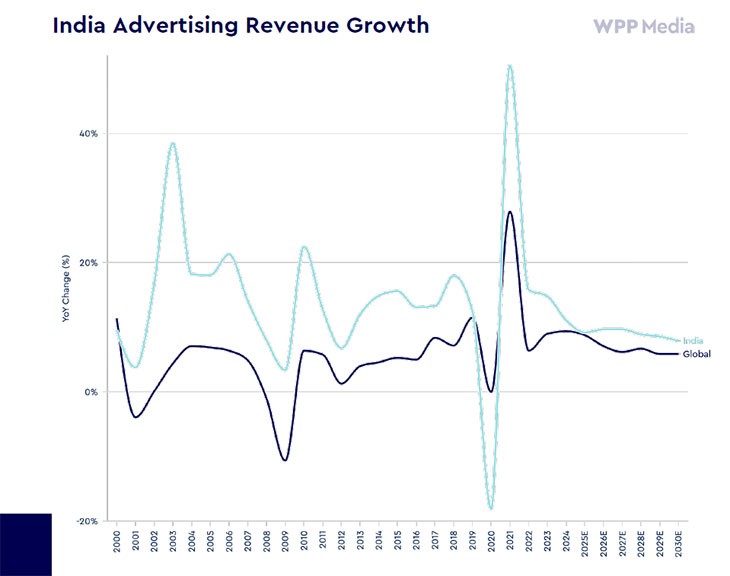

India’s advertising market continues to show resilience amid global macroeconomic uncertainty. According to WPP’s This Year, Next Year (TYNY) report, total advertising revenue is expected to reach Rs 185,000 crore (USD 20.7 billion) in 2025, reflecting 9.2% growth over 2024.

The group’s forecast early this year projected 7% growth in advertising expenditure in 2025, with the market expected to reach Rs 1,64,137 crore.

As per the year end statement, ad growth in India is projected to accelerate to 9.7% in 2026, taking the market to Rs 200,000 Cr. The IMF’s latest nominal GDP growth projection for 2026 remains at 10.2%.

In India, GDP and AdEx have usually demonstrated a dynamic interplay over the past decade. The average growth of the AdEx is expected to be around 1.5 times of the GDP growth. However, the softened consumption and decreased household savings seem to have impacted the AdEx growth.

As per the report, Indian household savings weakened between 2020 and 2024, with the share of bank deposits declining from 43% to 35% over the nine years preceding FY22–23, according to the Ministry of Statistics and Programme Implementation’s National Accounts data. Yet consumer spending has held firm in select categories, noted the report.

While the 2025 festive season (September–October) delivered exceptionally strong results, with retail sales crossing Rs 6 lakh crore supported by deep discounting across both online and offline channels, as per the Confederation of All India Traders.

“Beneath the headline numbers, however, bargain-led spending has intensified, and usage of BNPL apps continues to expand,” the report noted.

Content

Television continues to face structural headwinds. Total TV advertising is projected to decline 1.5% in 2025 to Rs 47,740 crore, before returning to growth in 2026. Linear TV viewership is expected to fall at a mid-single-digit rate as audiences spend more time online.

Streaming remains a bright spot, expanding rapidly off a smaller base. The November 2024 Reliance Jio–Disney Star merger has reshaped the competitive landscape, creating a market-leading digital-led entity. Amazon Prime Video’s ad-supported tier, launched in 2025, adds further competitive intensity.

Looking ahead, the 2027 IPL rights auction for the 2028 cycle will be a critical turning point. The BCCI is likely to steeply increase bid prices, setting up a high-stakes contest between legacy broadcasters and digital platforms and potentially accelerating the linear-to-digital shift.

Audio advertising will grow modestly, rising 1.5% in 2026 to Rs 29.0 billion (≈ Rs 2,610 crore), with digital audio formats—particularly podcasts—driving gains. Terrestrial radio is expected to decline 1–2% annually through 2030.

Print continues to defy broader global trends. Newspaper advertising is forecast to grow 3.5% in 2025 and 4.5% in 2026, reaching Rs 170.9 billion (≈ Rs 17,090 crore). Growth is being driven by government, political and retail advertising, much of it outside large agency networks. TV news consumption has risen sharply amid geopolitical and economic volatility, while readership measurement for print remains limited until third-party surveys potentially resume in 2026.

Magazine advertising, however, continues to decline structurally, falling 13.6% in 2025 to Rs 1.7 billion (≈ Rs 170 crore), although premium brands continue to invest selectively in luxury titles.

Other digital—including social platforms—remains the biggest absolute growth engine. It is projected to reach Rs 717.1 billion (≈ Rs 71,710 crore) in 2026, up 11.1% over 2025. Short-form video, particularly micro-dramas, continues to gain traction though audiences remain modest in scale. By 2026, other digital will account for 35.5% of India’s ad revenue.

Retail Media

Retail media remains India’s fastest-growing advertising channel. The sector is projected to rise 26.4% in 2025 to Rs 24,280 crore, followed by 25.0% growth in 2026 to Rs 30,360 crore. By 2026, retail media is expected to capture 15.0% of the country’s total advertising revenue.

Amazon and Walmart-owned Flipkart dominate the retail advertising ecosystem. Meanwhile, quick-commerce players—Blinkit, Zepto and Instamart—are scaling ad revenue at 100%+ growth rates, albeit from smaller bases, as competition for user attention and order frequency intensifies.

Search advertising will grow at a more moderate 8.9% in 2025, reaching over Rs 21,550 crore and accounting for 11.7% of total ad revenue. Growth decelerates to 8.0% in 2026, with mid- to high-single-digit gains through 2030. Google launched its AI Overviews feature in India in 2025, though its impact on search usage and commerce remains unclear. The market is maturing as advertisers reallocate more spend toward retail media.

Location

Out-of-home (OOH) continues to show strong momentum. The category is set to grow 8.6% in 2025 to approx Rs 3,790 crore, with a similar rate expected in 2026. Key drivers include:

- The return of IT and service-sector employees to office commutes

- Metro rail expansion into new cities and additional routes in existing networks

- Continued uptake of digital OOH, which will represent 4.1% of OOH revenue in 2026

- Heavy public investment in road and transport infrastructure over the past 3–5 years

OOH spending remains 40% national and 60% local, driven largely by smaller businesses and retail advertising. Key categories include automotive, mobile phones, e-commerce, fintech, and media & entertainment.

Cinema advertising is recovering steadily, rising 8.0% in 2025 to Rs 9.3 billion — approximately Rs 840 crore. Box office collections remain under pressure as more filmmakers release content directly on streaming platforms in exchange for guaranteed minimums. Cinema is expected to surpass pre-pandemic advertising levels in 2026.

Growth Drivers

Growth drivers for 2025–2026 include automotive, retail, BFSI, food & beverage and mobile handsets. Durables, commerce, retail and services are expected to remain stable.

The largest structural shift continues to be the migration of linear TV budgets to digital platforms—particularly commerce ecosystems. This reallocation shows no sign of slowing, though the report cautions advertisers against over-indexing on short-term performance at the expense of brand-building during the priming stage of consumer decision-making. Connected TV (CTV) is expected to record strong double-digit gains as advertisers follow audiences to streaming environments.

By 2030, India’s advertising market is projected to reach (Rs 280,000 crore). Content-driven advertising will account for 60.7% of total revenue, down from 71.6% in 2025, with commerce emerging as the dominant growth contributor. Traditional formats will continue to lose consumption and revenue share to digital, underscoring the ongoing structural transformation of India’s advertising ecosystem.

Read more news about Internet Advertising India, Marketing News, PR and Corporate Communication News, Digital Media News, Television Media News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News