Consolidation over experimentation: Brands rethink adtech as FY26 closes

Industry observers share test cycles have become much tighter and platforms are now expected to demonstrate incrementality or measurable outcomes quickly, with most rationalising technology stacks

by

by

Published: Apr 7, 2026 8:56 AM | 9 min read

As the financial year draws to a close on March 31, it is that time of the year when marketing teams, finance departments, and agency partners sit down with spreadsheets, dashboards, and campaign reports to tally what worked, what did not, and where next year’s budgets should go.

It is also when technology stacks are reviewed, pilot projects are evaluated, and platform partnerships are renewed or quietly dropped.

This year, across agencies, adtech firms and marketers, one theme appears to be emerging: brands are not necessarily experimenting less with new adtech platforms, but they are experimenting far more selectively.

Rewriting the rules of Programmatic advertising

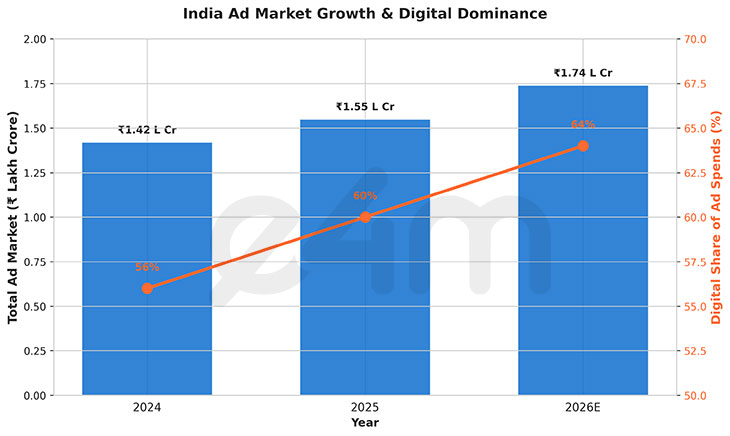

The broader advertising market numbers help explain why. The Pitch Madison Advertising Report 2026 places the market at around ₹1.55 lakh crore in 2025 on an expanded definition that includes quick commerce and MSME digital advertising, and similarly estimates digital’s share at roughly 60%. Perhaps even more pertinently, WPP Media’s This Year Next Year 2025 report estimates that of the incremental ad revenue added in 2025, over ₹10,000 crore came from digital alone, underlining how the growth of the advertising industry is now almost entirely tied to digital media.

Yet even within digital, the growth is not evenly distributed across a wide array of platforms and tools. Much of the incremental digital spending continues to flow into a relatively small set of scaled platforms and ecosystems, including search, social media, marketplaces, retail media networks, and large video and streaming platforms.

WPP Media also notes that digital and television together now account for roughly 85–86% of total advertising spends in India, and within television, streaming and connected TV are steadily increasing their share. In effect, even as the adtech ecosystem continues to expand with new tools and solutions, a large share of actual advertising money is concentrating around platforms that can deliver scale, measurable outcomes, and integrated buying and measurement systems.

This shift is something adtech companies themselves are seeing on the ground. Russhabh Thakkar, Founder and CEO of Frodoh, says brands are not reluctant to try new tools, but their expectations have changed significantly. “Brands aren’t scared of experimenting, they’re just tired of wasting money,” he says, adding that test cycles have become much tighter and platforms are now expected to demonstrate incrementality or measurable outcomes quickly.

He notes that conversations that earlier revolved around interesting new products now quickly move to questions around outcomes, unique reach, or measurable business impact. At the same time, he points out that brands are increasingly working with fewer partners but building deeper relationships, reflecting a broader consolidation trend.

Another major factor behind this shift is the growing role of performance-driven advertisers, particularly MSMEs, in India’s digital advertising growth. The Pitch Madison Advertising Report estimates MSME digital spends at around ₹35,814 crore in 2025, and forecasts that this could rise to nearly ₹42,976 crore in 2026.

In fact, MSMEs already account for roughly 35–38% of India’s digital ad market, much of it flowing into large, established platforms such as Google, Meta, and major marketplaces rather than a long tail of newer vendors.

These advertisers are typically far more ROI-driven and risk-averse than large brands when it comes to trying new platforms, and their growing share of digital ad spending is reinforcing a broader industry trend toward performance channels and established ecosystems rather than experimental tools.

From a marketer’s perspective, this does not mean experimentation has disappeared, but the way experimentation happens has changed.

Megha Agarwal, CMO at Table Space, says the experimentation mindset is still very much alive, but the tolerance for vague pilots has declined significantly. She notes that today, “Most technology tests are expected to begin with a clear hypothesis, defined budgets, and specific KPIs before the tool even goes live.”

For many marketers, the key question is no longer what a platform can do technically, but what commercial outcome it can demonstrate, whether that is improved pipeline quality, better account engagement, or faster deal velocity.

Agarwal also points out that many organisations are actively rationalising their technology stacks, as a leaner, well-integrated stack often performs better than a sprawling collection of disconnected tools.

This rationalisation is happening at a time when the number of adtech and martech tools available to marketers has exploded. Over the past few years, brands have been approached with tools for retail media optimisation, clean rooms, identity solutions, attention metrics, AI-driven creative optimisation, CTV measurement, attribution modelling, and customer data platforms, among many others.

A broader look at the market also helps explain why brands are becoming more selective about adding new platforms. India’s digital advertising market is expected to grow at roughly 10% annually and is projected to touch around USD 14–15 billion by 2026, according to industry estimates from WPP Media, Dentsu and Madison.

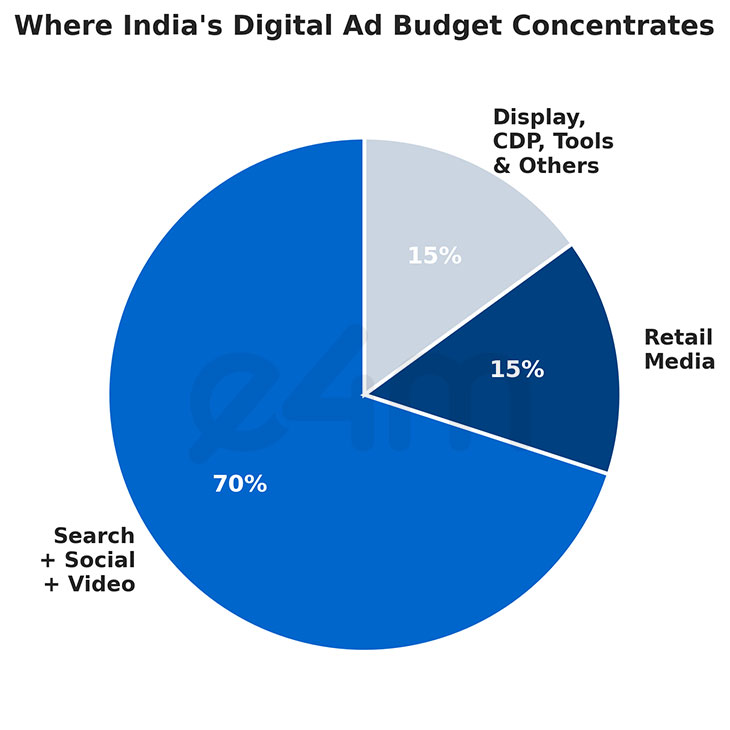

Within digital, search, social and video together account for nearly 70% of total digital ad spends, meaning a large share of advertising money is already concentrated in a handful of large platforms.

Retail media, meanwhile, is emerging as one of the fastest-growing segments in the digital ecosystem, with industry estimates suggesting it is growing at 25–30% annually as FMCG, e-commerce and quick commerce brands increasingly shift budgets toward commerce-linked advertising that can be tied directly to sales outcomes.

“We get pitched new platforms almost every week, whether it’s retail media, measurement tools or AI optimisation platforms. The reality is we don’t have the budgets or bandwidth to test everything anymore. So now every new platform has to answer a simple question: will this help us sell more or reach consumers more efficiently? If that isn’t clear quickly, we usually don’t move forward,” said a senior marketer at an FMCG company, requesting anonymity.

This shift toward performance and measurable media leaves relatively smaller experimental budgets for newer adtech tools unless they can clearly demonstrate incremental value.

At the same time, the number of marketing and advertising technology tools available to brands has exploded over the past decade.

Global martech landscape studies show that the number of marketing technology solutions worldwide has crossed 11,000 tools, spanning data platforms, attribution tools, clean rooms, identity solutions, retail media platforms, customer engagement platforms and AI-driven optimisation tools.

“The biggest challenge today is not lack of tools, it’s too many tools. Every platform has its own dashboard, attribution logic and reporting format, and that becomes very difficult to manage. We are actually trying to reduce the number of platforms we work with and go deeper with a few partners rather than spreading budgets too thin,” said a senior marketer from a beauty brand, who asked not to be named.

Large enterprises today often use dozens of marketing and data platforms across media, analytics, CRM and automation, which has led to growing complexity, overlapping capabilities and rising integration costs. As a result, many organisations are now focusing on tech stack rationalisation, integration and interoperability rather than continuously adding new standalone tools, reinforcing the broader industry shift from experimentation toward consolidation and efficiency.

Vivek Bhargava, Co-Founder of Consumr.ai, believes the industry is moving from a phase of testing more tools to testing smarter tools. He says the explosion of platforms has made prioritisation the real challenge for marketers, especially as budgets come under greater scrutiny.

According to him, brands are increasingly consolidating around platforms that bring clarity and deeper consumer understanding rather than just execution capabilities. He describes this shift as a move from managing tool stacks to building intelligence stacks, where the focus is on platforms that improve decision-making rather than simply adding another layer of execution.

At the same time, agencies say that financial scrutiny and business pressure are also shaping platform decisions. With CEOs and CFOs increasingly asking for clearer returns on marketing investments, budgets are often being directed toward channels with proven performance, such as search, retail media, and large video platforms.

From a beauty and wellness brand’s perspective, Anurag Mehrotra - Chairman at Fixderma, says retail media planning has to become more agile and localised.

"For us at Fixderma, quick commerce is also becoming an interesting discovery channel. Consumers are increasingly comfortable ordering skincare products instantly whether it’s sunscreen before stepping out or an acne solution when they need it quickly. That behaviour shift is pushing brands to think more dynamically about both visibility and availability."

Why video advertising no longer has formats

Sector-wise data cited in industry reports shows digital spends climbing across categories such as FMCG and e-commerce, with smaller categories also increasing digital spends significantly year-on-year, much of it flowing into performance-driven channels rather than experimental media formats.

Privacy regulations, data compliance requirements, and integration challenges are also making marketers more cautious about adopting standalone tools that do not fit into existing technology ecosystems.

Tejas Maha, Associate Director – Media at White Rivers Media, says agencies and brands are increasingly evaluating new tools based on how well they integrate with existing systems such as CRM platforms and DSPs, and whether they can demonstrate measurable business impact.

He notes that many organisations are now conducting tech stack audits to remove duplicate tools, reduce technical debt, and move toward fewer dashboards and more integrated platforms. According to him, new tools are still being tested, but usually through structured pilots tied to specific KPIs and business outcomes rather than broad exploratory budgets.

Taken together, these shifts suggest that the adtech ecosystem in India may be entering a new phase. Over the past few years, the industry was in an experimentation phase, with brands testing multiple tools across data, measurement, retail media, CTV, and AI-driven optimisation.

As digital advertising matures and budgets come under closer scrutiny, the industry now appears to be moving into a consolidation and efficiency phase, where marketers are focusing on fewer platforms that can integrate into existing stacks and demonstrate clear business outcomes.

Experimentation, industry executives say, is unlikely to disappear. But random experimentation without clear outcomes is increasingly difficult to justify in an environment where digital advertising budgets are growing, but so are expectations around performance, measurement, and accountability. In that sense, the question is no longer whether brands will experiment with new adtech platforms, but which platforms can prove they are worth being part of a much smaller, more accountable technology stack.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News