IPL 2026: CTV gains, e-gaming ban impact linear TV

Higher CTV viewership, fewer brands on TV and rising digital traction signal a shift in how India’s biggest media property is being bought and consumed, early data trends suggest

by

by

Published: Apr 29, 2026 8:09 AM | 5 min read

- The 2026 IPL season has seen a significant decline in TV advertiser participation, dropping from over 65 brands in 2025 to around 45, despite stable total ad inventory, indicating a shift towards fewer, more selective advertisers.

- Digital viewership is on the rise, with connected TV (CTV) watch time reaching 32 billion minutes during the opening weekend, and Google emerging as a dominant advertiser, while traditional brands like Parle and Coca-Cola have exited.

- Linear TV metrics show a decline in average ratings and audience engagement, attributed to a shift towards digital platforms, raising concerns about over-commercialization and diminishing returns for advertisers.

- The evolving advertising landscape suggests IPL is transitioning to a more mature phase with concentrated spending, impacting future media rights negotiations set to conclude in 2027.

The Indian Premier League (IPL), India's biggest media property, is showing early signs of a structural shift in its advertising dynamics. The 2026 season witnessed a jump to 32 billion minutes watch time for the opening weekend on CTV, and a contraction in advertiser participation on TV even as overall inventory on TV remained largely unchanged.

According to an early-season industry report based on BARC and TAM Sports data, the number of advertisers on TV has dropped from over 65 in 2025 to around 45 in 2026—a decline of more than 30%. This comes despite total ad inventory (FCT) remaining nearly flat at 4.73–4.78 lakh seconds in the first 16 matches, indicating that fewer brands are now accounting for a similar volume of advertising time.

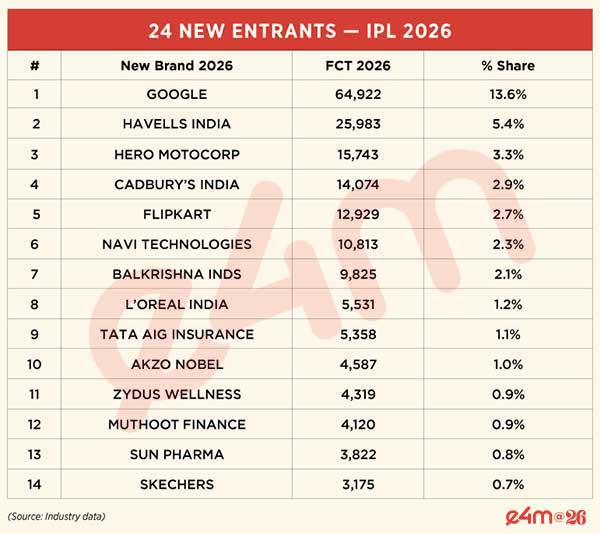

The churn further underscores this shift, with 44 brands exiting the property and 24 new entrants coming in during the first three weeks. For a property long defined by its breadth of brand participation, this narrowing base points to a more concentrated and increasingly selective market and also an impact of ban on e-gaming companies in 2025. For context, just two companies, Dream 11 and Playgames 24*7, took more than 6% of FCT share on TV in the 2025 edition.

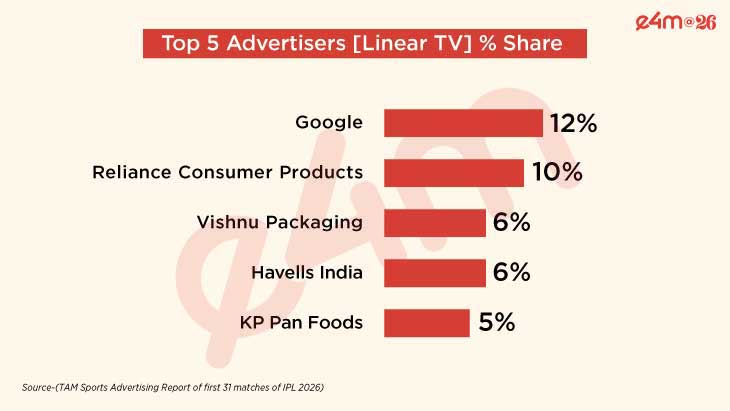

The change is also visible in the advertiser mix. FMCG major Parle, last year’s top spender, along with RBI, Coca-Cola, Maruti Suzuki, Tata Motors, Tata Digital and Emirates Airlines, has exited the league. In contrast, Google has emerged as a dominant player with a 13.6% share of ad volumes. New entrants include Havells, Navi Technologies, Cadbury, Flipkart, L’Oréal, Zydus and Sun Pharma.

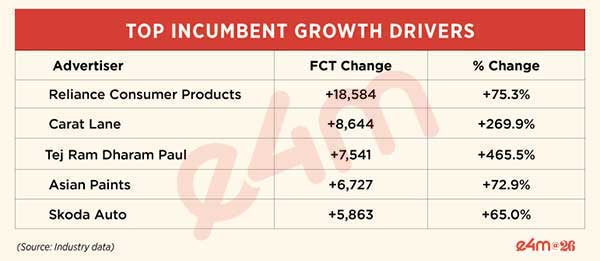

Among continuing advertisers, spends have become more concentrated. Reliance Consumer Products (+75%), Asian Paints (+73%) and Skoda Auto (+65%) have ramped up investments, while others such as Apple (-43%) and Star India (-52.8%) have scaled back. The result is a market increasingly driven by a smaller set of deep-pocketed players.

Linear Signals Show Softening

Alongside these shifts in advertiser behaviour, linear television metrics indicate a softening trend. Average TV ratings for the first 15 matches landed at 3.71 in 2026 vs 4.57 in 2025, the data indicates.

Meanwhile, reach (for AA 15+) on TV which was at 123.96K is down to 113.61K in the opening phase, while Average Minute Audience (AMA) has gone from 10,600K to 7,842K, pointing to weaker engagement.

The change is across gender, with male TVR dropping from 5.06 to 4.13 and female TVR from 4.06 to 3.28.

Industry executives attribute this largely to continued migration toward digital platforms, reinforcing the shift in consumption patterns.

e4m reported earlier this month that ad rates on linear television have remained largely unchanged from last season, with 10-second spots during live matches priced at ₹18 lakh for combined SD+HD feeds, ₹15 lakh for SD-only, and ₹7.2 lakh for HD-only.

Also read: IPL 2026: Fewer brands but stronger shift in advertiser mix?

IPL: CTV surges with digital ads, FMCG holds ground on linear TV

In a first, Google tops IPL ad charts

Digital Gains Momentum

Digital, meanwhile, has started the season on a strong note. Data put out by JioStar claims impressive jump on CTV viewership. Opening weekend data shows combined reach rising to 515 million across two matches (up 26% per match), with total watch time at 32.6 billion minutes. Peak concurrency on connected TV is estimated to be 61% higher by the time this season ends, highlighting growing adoption of large-screen streaming.

Monetisation on digital—particularly CTV—is increasingly driven by CPM-based buying and audience targeting. As per rate cards accessed by e4m, JioStar’s live mid-roll inventory starts at ₹600 CPM, rising to ₹800 for targeted segments, while match-select pre-roll inventory is priced between ₹1,200 and ₹1,600 CPM.

By the time this season ends, the full season digital reach is estimated to end up at around 750 Mn + (vs 652 mn LY) as per JioStar MPA 2025 report.

CTL 2 placements on CTV are pegged at ₹21.35 lakh for 10-second spots, while pre- and post-show inventory is priced at ₹4 lakh. Non-live inventory, including VOD and highlights, starts at ₹450 CPM, offering cost-efficient scale.

Digital is also being sold through bundled packages, with handheld (HH) deals ranging from ₹25 crore to ₹100 crore, and CTV packages priced between ₹60 crore and ₹150 crore.

Risk of Over-Commercialisation?

Engagement trends point to a more nuanced challenge. The drop in TV AMA compared to reach suggests viewers are spending less time per match pn TV, signalling shift towards digital viewership.

With ad inventory on TV remaining largely unchanged despite softer engagement, concerns around over-commercialisation are emerging. “For advertisers, this could translate into diminishing returns, particularly in a market that is becoming increasingly ROI-driven,” an ad executive said.

From Scale to Selectivity

Taken together, the trends suggest that IPL, valued at ₹76,100 crore (D&P Advisory IPL Valuation Report 2025), is entering a more mature phase. The property continues to deliver scale, but the nature of participation is shifting—from broad-based advertiser presence to more concentrated, performance-led spending.

However, the full-season picture is still evolving, with the final scheduled for May 31. While digital reach is expected to peak during the playoffs, it remains to be seen whether it can consistently offset the scale and stability historically delivered by linear television.

This year’s advertising performance will also have a bearing on the next media rights cycle, with the current deal set to end in 2027.

“The next rights cycle will be crucial in determining the trajectory of value creation for the league,” said a senior executive at a global ad network. “If media valuations continue to grow, it strengthens franchise economics. If they stabilise, the model still holds—but growth expectations will need recalibration.”

e4m reached out to JioStar, the official broadcast and streaming partner of IPL, for comments. The copy will be updated once they respond.

Read more news about (internet advertising India, internet advertising, advertising India, digital advertising India, media advertising India)

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Whatsapp