e4m Report Card 2025: Big Tech’s big year in earnings and courtrooms

This was not the year Big Tech escaped scrutiny. It was the year scrutiny finally began to harden institutionally, even as the businesses themselves continued to compound

by

by

Published: Dec 23, 2025 9:14 AM | 6 min read

Through most of 2025, Big Tech demonstrated once again that it can grow through almost anything. Lawsuits, regulatory pressure, parliamentary scrutiny, fines, investigations and fresh compliance regimes all intensified through the year. Revenues, at least through the first three quarters, did not flinch. Markets barely blinked. If anything, the gap between legal accountability and commercial performance became clearer.

This was not the year Big Tech escaped scrutiny. It was the year scrutiny finally began to harden institutionally, even as the businesses themselves continued to compound.

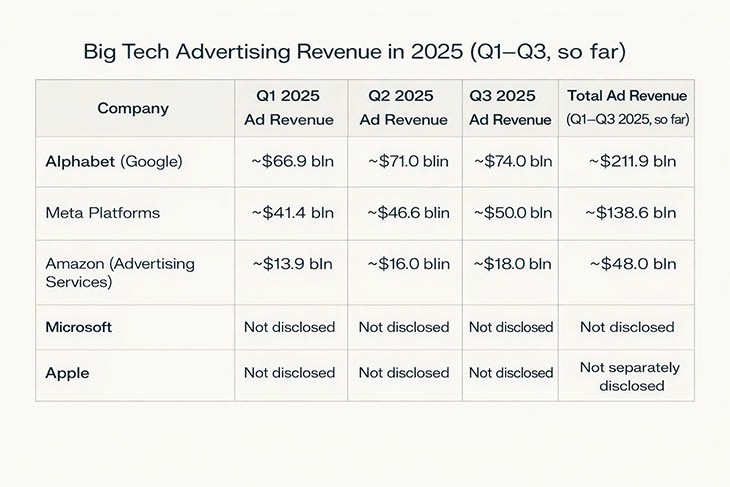

So far in 2025, the earnings picture has remained robust. Alphabet reported double-digit revenue growth through Q3, driven by a recovery in advertising and continued expansion in Google Cloud. Meta delivered one of its strongest profit performances in recent years through the same period, with advertising revenues growing sharply and margins expanding, even as Reality Labs continued to post losses. Amazon’s advertising business continued to grow faster than its core retail operations, while AWS stabilised as a cash engine after a volatile prior year. Apple saw moderation in hardware growth, but services revenues continued to provide ballast. Microsoft leaned heavily into cloud and enterprise AI, reinforcing its position as one of the quiet beneficiaries of Big Tech’s infrastructure moment.

This matters because 2025 was widely expected to be the year regulation finally showed up on income statements. Through Q3, it largely had not.

Advertising, in particular, remained stubbornly resilient. Despite years of predictions about fragmentation, decentralisation and the erosion of platform dominance, Google and Meta continued to anchor global and Indian digital ad spends. Search and social remained the default demand-capture layers for most advertisers, even as retail media rose sharply alongside them. Budgets shifted at the margins, formats evolved, but the centre of gravity held.

In India, this resilience was especially visible. Digital advertising continued to grow at a healthy clip through 2025, and Big Tech platforms retained their centrality to reach, performance and discovery. Retail media expanded rapidly, but it did not displace search or social. It supplemented them. The result was not disruption, but reinforcement.

While earnings stayed strong through most of the year, the legal and regulatory calendar grew increasingly crowded.

For Google, 2025 was marked by sustained anti-trust pressure across jurisdictions. In the United States, scrutiny of its search and adtech practices continued to intensify, with courts and regulators moving beyond abstract dominance arguments towards discussions around remedies. In the European Union, enforcement under the Digital Markets Act began to translate into operational changes, particularly around self-preferencing, interoperability and default settings. None of these actions concluded decisively in 2025, but the regulatory direction became harder to ignore.

Apple spent much of 2025 navigating continued pressure around its App Store economics. In the EU, DMA enforcement pushed the company towards changes in payment flows, steering rules and platform controls. In the US, scrutiny remained more fragmented, but the cumulative effect was a narrowing of Apple’s room to manoeuvre. The impact during 2025 remained procedural rather than financial, but the guardrails tightened.

Meta’s exposure was similarly layered. In the EU, enforcement under the DMA and the Digital Services Act forced operational adjustments related to advertising transparency, data usage and platform obligations. Elsewhere, privacy and competition scrutiny continued to shadow the company. Yet through Q3 2025, Meta’s advertising engine remained largely insulated from these pressures.

Across Big Tech, the pattern repeated. Legal pressure rose. Revenues, so far, held.

It would be inaccurate to say that regulators were no longer satisfied with fines alone in 2025. The year featured both substantial financial penalties and a deepening emphasis on structural oversight. What changed was not the presence of fines, but the growing recognition that penalties by themselves were insufficient to alter platform behaviour. Regulators increasingly paired fines with monitoring regimes, compliance obligations and early-stage remedy discussions.

The reason earnings and courtrooms did not meaningfully collide in 2025 is not difficult to explain. Litigation timelines are long. Revenue cycles are short. Even large fines remain financially absorbable for companies operating at this scale. More importantly, most regulatory actions in 2025 were still focused on process rather than product. They signalled intent, not transformation.

The real threat to Big Tech lies less in penalties than in remedies. Changes to defaults, auction mechanics, self-preferencing rules, distribution advantages and data flows are far more consequential than one-time fines. In 2025, most of these remedies were still under consultation, phased rollout or early enforcement. The commercial impact remains largely prospective.

India offers a useful case study in this regulatory lag.

From a policy standpoint, 2025 was significant because it marked the transition of India’s Digital Personal Data Protection framework from legislation to implementation. The DPDP Act itself was passed in 2023. What 2025 delivered were the Rules, the operational contours of compliance, and the gradual set-up of the Data Protection Board.

In practical terms, DPDP’s impact in 2025 functioned as a compliance reset rather than a business disruption. Platforms updated consent mechanisms, revised disclosures, and began aligning internal processes with localisation and data-handling requirements. Enforcement, however, remains staggered, with substantive oversight and penalties expected to roll out progressively into 2026 and 2027.

As with GDPR in its early years, DPDP’s long-term force will depend less on the statute itself and more on how assertively it is interpreted and enforced. For Big Tech, DPDP in 2025 joined a growing list of regulatory obligations treated as operating conditions rather than existential threats.

Compliance costs rose. Legal and policy teams expanded. Product adjustments occurred at the margins. Advertising models and platform economics, through Q3 2025, remained largely intact.

Markets responded accordingly.

Investor behaviour through most of the year suggested that regulatory risk had already been priced in. Share prices tracked earnings performance and growth prospects far more closely than legal headlines. Capital expenditure on AI infrastructure, cloud capacity and platform expansion continued. Advertisers did not meaningfully retreat. Developers did not decamp. Dependence remained.

This is not because regulation failed in 2025. It is because regulation and commerce continue to operate on different clocks.

The uncomfortable conclusion of Big Tech’s 2025 report card is that scrutiny has become systemic, but impact remains deferred. Courts and regulators are laying foundations. Companies are adapting without retreating. The collision between legal accountability and business models has been scheduled, not cancelled.

What changes after 2025 is not the presence of regulation, but its character. The next phase will be less about fines and filings, and more about product-level constraints. Distribution defaults, auction design, platform fees and data flows will become the real battlegrounds. These are slower, more complex interventions, and far harder for platforms to absorb quietly.

For now, 2025 stands as proof of concept. Big Tech showed that, through most of the year, it could absorb lawsuits, comply with new rules such as DPDP, navigate EU DMA and DSA enforcement, and still deliver strong earnings.

Regulation is getting sharper. But until it materially alters how these companies make money, it remains pressure, not gravity.

That, more than any verdict or quarterly result, was Big Tech’s real achievement in 2025.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News