AI Search after the hype: The quiet repricing of visibility in India

In a series of articles starting today, we will be exploring the impact of AI on search advertising, innovations & disruptions of emerging players, and the role of LLMs in this new marketing matrix

by

by

Published: Feb 20, 2026 8:29 AM | 9 min read

For the better part of three years, Artificial Intelligence in search has been discussed as if it were an incoming storm. Blue links were declared relics. SEO was placed on premature obituary watch. Zero-click behaviour was framed as structural collapse. Every panel had a slide on disruption; every agency deck acquired a new acronym. The tone suggested that Search, that mainstay of digital advertising, was in existential trouble as a commercial system.

And yet, here we are.

Search has not disappeared. Consumers have not stopped looking. Brands have not stopped bidding. What has changed is less dramatic and far more consequential. AI has not replaced search; it has layered itself over it. Instead of ten blue links competing for attention, users increasingly encounter summarised answers, conversational prompts, and recommendation-style responses that compress research into a few sentences.

The act of searching feels shorter, cleaner, more resolved. The commercial machinery underneath continues to operate, but the surface through which users experience it has been reconfigured.

The shift is not about whether search survives. It is about how visibility is allocated inside it. When discovery compresses into summaries and conversational interfaces, attention concentrates. When attention concentrates, leverage moves. The early phase of the AI search story was dominated by speculation about extinction. The current phase is quieter and more structural. It is about redistribution, of exposure, of traffic quality, of pricing power, and ultimately of control.

The question, then, is no longer whether AI will disrupt search. It is who benefits most from the way that disruption has settled.

Market math

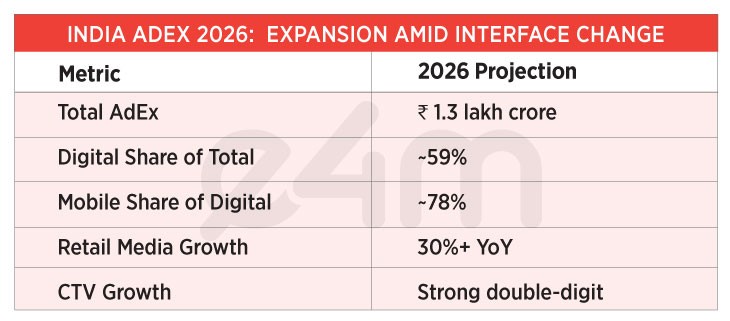

India’s advertising market in 2026 is larger, more digital, and more structurally diversified than at any point in its history. According to the Dentsu-e4m Digital Advertising Report 2026, total ad expenditure is projected to touch and or cross the ₹1.3 lakh crore range.

Digital accounts for approximately 59% of that total, cementing its majority status. Within digital, mobile continues to dominate at nearly 78% of spend. Retail media is expanding at over 30% year-on-year, while connected television is growing in strong double digits.

This context matters, because the conversation around AI in search has often been framed as contraction or disruption. In reality, the overall market is expanding. Search has not disappeared within that growth. But the economics of visibility within search have shifted.

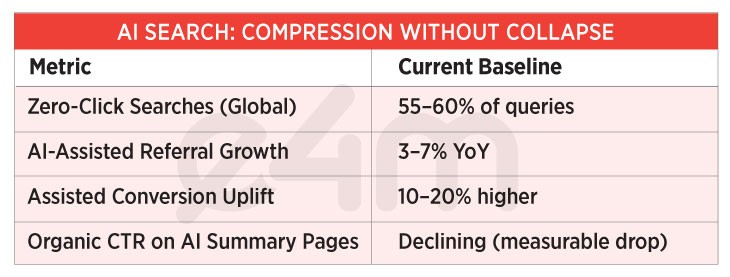

Globally, zero-click searches now account for approximately 55–60% of queries, driven by AI-generated summaries and rich answer formats that resolve informational queries directly on the results page. Simultaneously, AI-assisted discovery contributes modest but accelerating referral growth, at roughly 3–7% year-on-year across large content categories.

These two movements of declining exploratory clicks and rising AI-influenced traffic define the current equilibrium.

The shift

What makes this shift structurally different from previous search evolutions is not simply the presence of summaries. It is the engine generating them. Large Language Models like OpenAI’s ChatGPT, Google’s Gemini, Perplexity, and Anthropic’s Claude, among others, now sit between the user and the index.

Traditional search engines ranked and retrieved links. LLM-powered systems synthesise, summarise and recommend. They interpret multi-sentence prompts, infer intent, and generate consolidated responses that blend information from multiple sources into a single narrative output.

That difference is subtle but economically significant.

When discovery is mediated by an LLM, visibility is no longer determined solely by rank position. It is influenced by whether a brand, publisher or data source is considered authoritative enough to be incorporated into a generated answer. Inclusion becomes probabilistic rather than positional.

This changes optimisation logic. The competitive question shifts from “How high do I rank?” to “Am I structurally legible to the model?”

In a digital advertising market that now commands nearly 60% of total adex in India, this layer of mediation matters. The LLM does not eliminate search demand. It restructures the pathway through which demand encounters supply. And that restructuring is where leverage moves.

Fewer clicks, higher intent

The immediate reaction to zero-click behaviour is to interpret it as loss. However, the data suggests a more nuanced outcome. Abhinay Bhasin, Senior Vice President – Product & Technology at dentsu India, notes that while overall organic clicks are under pressure as AI summaries proliferate, traffic influenced by AI interfaces tends to demonstrate stronger engagement and assisted conversion metrics, often 10–20% higher than conventional pathways.

The result is filtration rather than collapse. Informational curiosity is increasingly resolved within summary modules. When users do click through, they tend to be closer to decision. The funnel narrows, but it narrows toward intent.

From a commercial standpoint, this explains why transactional search has proven resilient. High-consideration categories (banking, travel, real estate, automotive, retail) continue to rely heavily on search advertising for performance outcomes. Paid search budgets in India remain structurally embedded in performance marketing frameworks.

Gopa Menon, COO and co-founder of Theblurr, cautions against overstating the disruption. “Traditional search hasn’t collapsed; it’s evolving into a mix of classic SERPs, AI overviews, and conversational interfaces, and in India Google still anchors the ecosystem for both discovery and performance,” he says.

Search is not dead. It is layered.

Industry snapshot

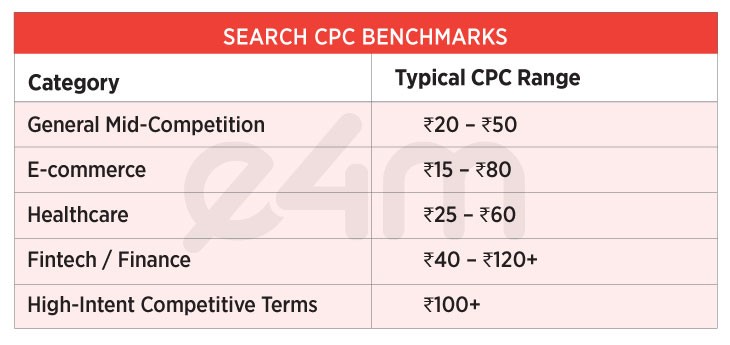

As of early 2026, search advertising in India continues to be predominantly auction-driven and priced on a cost-per-click basis, with benchmarks reflecting both rising competition and category variance.

Industry estimates suggest that average search CPCs in India typically range between ₹20 and ₹50 for mid-competition keywords, with higher-intent verticals such as finance, insurance, fintech and certain enterprise B2B categories frequently exceeding ₹100 per click in competitive auctions.

E-commerce keywords often fall in the ₹15–₹80 range, healthcare in the ₹25–₹60 band, and fintech or high-value financial products can extend from ₹40 to ₹120 or more, depending on query competitiveness and audience targeting. These ranges underline a key dynamic: while India’s search CPCs remain lower than mature Western markets, premium commercial terms have steadily climbed as digital competition intensifies.

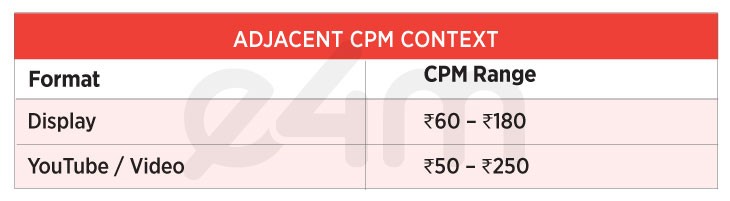

Unlike display or video formats, search inventory itself is rarely sold on a CPM basis, since it is fundamentally performance-oriented and auction-priced per click.

However, adjacent digital formats provide useful context for broader pricing pressure. Impression-based campaigns in display and YouTube environments typically operate within CPM ranges of roughly ₹60–₹180 per 1,000 impressions, with premium video formats extending into the ₹50–₹250 CPM bracket depending on targeting and inventory quality.

Taken together, these benchmarks suggest that while AI-mediated discovery may compress informational clicks, high-intent search traffic in India remains commercially valuable (and increasingly competitive) within a performance ecosystem that continues to price intent rather than impressions.

Informational traffic and mid-funnel compression

The more significant shift is occurring in informational discovery. AI-generated summaries increasingly resolve comparison-heavy, research-oriented queries before users scroll. Organic click-through rates on pages featuring AI summaries have declined measurably.

Jacob Joseph, VP – Data Science at CleverTap, captures this asymmetry: “The rhetoric about SEO and paid search being obsolete is a bit overstated… while informational traffic is taking a hit, transactional and branded intents remain remarkably stable.”

Informational queries historically supplied mid-funnel oxygen. They supported publisher traffic models, fed remarketing pools, and created surplus inventory across display ecosystems. AI compression reduces that surplus. Research collapses into synthesis. Fewer downstream impressions are generated organically.

In a market where digital accounts for nearly 60% of total ad expenditure, even marginal reductions in exploratory traffic alter the supply-demand balance of attention.

Scarcity emerges not in consumer demand, but in available surface area.

Intent expression, not intent erosion

From a brand perspective, the behavioural shift is less about disappearing demand and more about how users articulate it.

Prasun Kumar, CMO at Magicbricks, observes that “what’s genuinely changing is how intent is expressed, not the intent itself.” Users increasingly ask longer, conversational, outcome-oriented questions. They expect aggregation, comparison, and summarised recommendations. AI interfaces provide these directly.

For brands, this alters competitive dynamics. Ranking for fragmented keywords is less consequential if inclusion inside summarised answers determines first exposure. Structured data, authoritative signals, and credible domain expertise become prerequisites for representation.

Inclusion becomes a visibility currency.

Brands that have invested in first-party data, consistent entity signals, and authoritative content frameworks benefit disproportionately from AI synthesis. Those dependent on thin content or keyword arbitrage face greater volatility.

The competitive variable shifts from “position on page” to “presence within answer.”

The broader redistribution of digital spend

The Dentsu-e4m report’s spend composition reinforces this recalibration. Retail media’s 30%+ growth trajectory indicates aggressive reallocation of performance budgets toward environments with structured purchase signals. CTV’s double-digit expansion signals diversification in upper-funnel reach strategies.

Search continues to function as a performance backbone, but it is no longer the singular axis of digital strategy. As digital consolidates 59% of total adex and mobile commands 78% of digital budgets, the interface layer increasingly governs exposure economics.

AI summaries, generated by LLMs, sit precisely at that interface.

Search ad spend does not evaporate under AI pressure. It competes within a broader ecosystem of structured signal environments. Performance remains measurable, but discovery compresses.

Winners & vulnerabilities

The beneficiaries of this compression are clear. Platforms that control summarisation layers gain leverage over first exposure. Brands with authoritative signals gain defensibility. High-intent traffic becomes more concentrated and, in many cases, more efficient.

The vulnerabilities are equally visible. Generic informational publishers face declining surface-level traffic. Thin affiliate ecosystems struggle when comparison content is replaced by synthesised summaries. Mid-funnel arbitrage becomes structurally fragile in a compressed discovery environment.

Even challenger brands encounter higher entry thresholds. Representation inside AI-generated summaries increasingly requires structured entities, credible references, and consistent cross-channel signals. Visibility becomes capital-intensive rather than optimisation-driven.

Repricing, not rupture

The industry spent 2024 asking whether AI would kill search advertising. By 2026, the data suggests a calmer interpretation. India’s advertising market is expanding. Digital dominates. Search remains integral to performance strategies. Transactional intent persists.

What has shifted is leverage.

AI search has compressed informational discovery, filtered traffic toward higher intent, and reduced surplus visibility at the top of the funnel. In a ₹1.3 lakh crore advertising economy, that reduction in surface area carries consequences.

Visibility was once abundant through rank optimisation. It is now scarcer through summarised inclusion. In markets, scarcity rarely redistributes evenly.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News