India nears US & China in digital ad share, but structural gaps remain

Digital ad share in India is set to hit approx 70% by 2027, closing in on major economies, but lower ad pricing, platform dominance and ROI-led spends limit value parity, experts point out

by

by

Published: Feb 16, 2026 9:05 AM | 7 min read

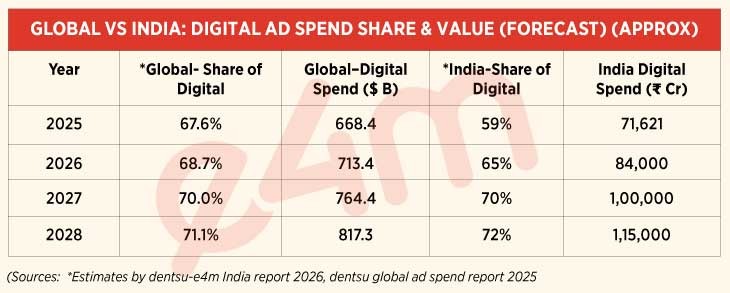

India’s digital advertising market is no longer merely catching up with global peers—it is structurally converging with them in the media mix. Digital is estimated to have grown nearly 19% in 2025 to ₹71,621 crore, accounting for about 59% of India’s total ad expenditure of over ₹1.2 lakh crore, according to the dentsu–e4m Digital Advertising Report 2026.

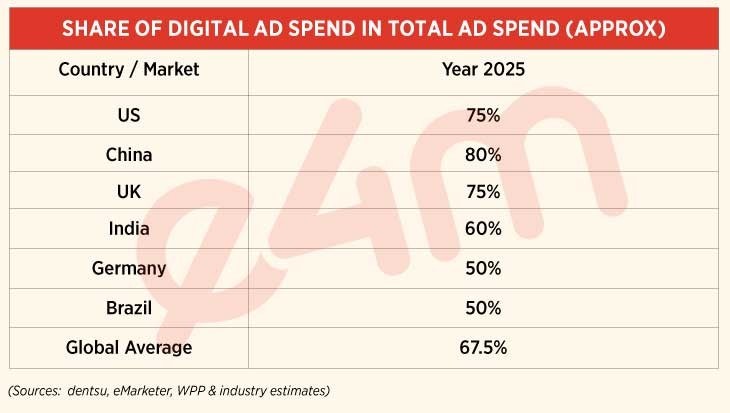

At this pace, digital is projected to command around 65% of total ad spend by end-2026 and approach 70% by 2027—bringing India closer to mature markets such as the US, where digital accounts for about 75% of ad spend, and China, where it exceeds 80%, various industry estimates suggests.

The shift marks a decisive reordering of India’s media economy. In less than a decade, digital’s share of total ad spend has climbed from around 12% in 2016 to nearly 60% today, making it not just the fastest-growing medium but the primary destination for incremental advertising investments.

Read On: Digital format allocation by verticals: How India’s ad money has shifted

Industry executives said digital is now shaping overall ad market expansion, rather than merely benefiting from it.

What makes India’s trajectory particularly striking, experts said, is the speed at which this transition is unfolding despite lower per-capita income and overall advertising intensity compared with developed markets.

Smartphone penetration, ultra-low mobile data costs, and platform-led consumption have accelerated the shift, compressing into a few years a transition that took over a decade in Western economies.

As a result, India is approaching global benchmarks in digital share far earlier in its economic cycle. However, executives cautioned that headline convergence in share does not yet translate into parity in value, as differences in pricing, advertiser mix, and platform economics continue to shape the market differently.

Digital’s rise has also reshaped the structure of advertising growth itself. The medium is no longer just absorbing budgets from traditional channels but is expanding the advertiser base, drawing in startups, direct-to-consumer brands, and small businesses that rely on measurable, performance-driven formats to scale customer acquisition, industry leaders point out.

Yet, beneath the headline convergence in digital share lies a more complex reality—one shaped by very different CPM economics, platform structures and maturity of the digital value chain.

Growth is rapid—but structurally different from global markets

India’s digital ad growth is being powered primarily by video, commerce-linked advertising and creator-led formats—reflecting a markedly different expansion pattern from mature markets. Social media and online video together account for over half of digital ad spends, with social media contributing 29% (₹21,057 crore) and online video 28% (₹20,004 crore). Online video is projected to overtake social by 2027, driven by mobile-first consumption and OTT expansion.

Read On: Digital projected to command 70% of total ad spends by 2027: dentsu-e4m report

Industry executives said retail media on e-commerce and quick-commerce platforms has emerged as one of the most structurally incremental segments—unlike in mature markets where digital growth is increasingly driven by premium streaming and brand-led video.

Meher Patel, Founder, Hector (Wondrlab Network platform), said brands are reallocating trade marketing and offline visibility budgets into marketplace advertising, effectively bringing net new money into digital.

Sharing more, Nitin Sabharwal, Founding Partner and COO, Indixital, said platforms such as Amazon, Blinkit and Zepto are evolving into full-funnel media environments, particularly for FMCG and D2C brands. At the same time, OTT and connected TV are beginning to attract brand budgets from linear television, while influencer-led commerce—especially in Tier 2 and Tier 3 markets—is unlocking new advertiser segments.

However, unlike the US and China, where digital expansion is increasingly driven by brand and premium video spends, a significant portion of India’s growth remains performance-led. Executives said spending continues to shift between large platforms such as Google, Meta and marketplaces, with genuinely new money concentrated in commerce-linked and attribution-driven environments.

Same share, different depth of monetisation

In the US and China, digital maturity is supported by diversified retail media networks, large-scale connected TV, premium video ecosystems and strong brand-led investments. India, by contrast, remains heavily skewed toward performance-led formats such as search, social and marketplace advertising.

Sayak Mukherjee, Founder and Director, Brandwizz and Creatorcult Media, said India’s digital budgets remain largely conversion-driven, keeping pricing competitive and agency margins tighter. However, he noted that India’s cost efficiencies and expanding creator ecosystem allow platforms and advertisers to scale rapidly, even if monetisation per user remains significantly lower than in mature markets.

A senior executive at a rival global media agency said India’s digital transition has followed a structurally different path from Western markets. “India isn’t just catching up on digital share—we’ve leapfrogged parts of the traditional evolution cycle. The ecosystem is far more mobile-first, video-heavy and commerce-linked. That accelerates scale, but also means growth is concentrated in performance environments rather than premium brand-led media,” the executive said.

The divergence becomes clearer when advertising is viewed relative to economic size. Advertising accounts for around 1–1.5% of GDP in markets such as the US and UK, compared with about 0.4% in India, projected to rise to around 0.5% by 2029. Executives said this suggests India is converging rapidly in media mix, but not yet in underlying value creation.

Low CPMs accelerate adoption—but limit value parity

India’s digital expansion has been enabled in part by structurally lower advertising costs. Rahul Vengalil, CEO, Tgthr, noted, “CPMs in India remain a fraction of those in developed markets, accelerating adoption among performance-driven advertisers but reinforcing India’s position as a volume-led market.”

CPMs are gradually rising across platforms over the past few years, but platform concentration remains high, with Google, Meta, Amazon and Flipkart capturing a disproportionate share of measurable spend. This has enabled rapid scale but limited value capture compared with more diversified ecosystems in mature markets, Mehr Patel explains.

Read On: Digital AdEx to grow 7.41%, but CPMs likely to face pressure

Scale brings efficiency—but also maturity pressures

Industry leaders said India’s market is entering a phase of optimisation rather than pure expansion, as rising CPMs, signal fragmentation and increased competition begin to compress performance efficiency. This mirrors patterns seen earlier in mature markets such as the US and China, where digital continued to grow but required more sophisticated, full-funnel strategies to sustain returns.

Mukherjee said the shift reflects strategic evolution rather than slowdown. As digital penetration deepens, he noted, brands are moving beyond pure performance marketing toward more balanced allocation models that combine conversion-led spending with brand-building, creator engagement and commerce integration. This transition is driving hybrid media strategies that are digital-first but increasingly outcome-agnostic across channels.

Other industry executives said rising auction density and signal loss—driven by privacy changes and platform concentration—are making incremental efficiency harder to achieve through performance channels alone. As a result, advertisers are expanding into retail media, OTT, connected TV and influencer-led ecosystems to access new audiences and sustain growth.

Sabharwal echoes the sentiments. “The connected TV and premium video environments are becoming particularly important as brands look to build incremental reach beyond saturated performance channels. These formats, he said, offer a combination of measurable outcomes and upper-funnel brand visibility, helping advertisers balance immediate conversion with longer-term demand creation,” he noted.

Executives added that this phase marks the natural maturation of India’s digital ecosystem. While digital will continue to attract incremental budgets, the next phase of growth is expected to be driven less by migration from traditional media and more by improved monetisation, deeper advertiser participation and more sophisticated use of data and creative strategy.

“This mirrors the trajectory seen in the US around 2016–2019 and in China shortly thereafter, when digital crossed majority share and efficiency gains gave way to more complex, full-funnel strategies”, a senior executive points out.

Read more news about Internet Advertising India, Marketing News, PR and Corporate Communication News, Digital Media News, Television Media News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News