What will it take for quick commerce to win Bharat?

As Q-comm players eye Tier-2 and Tier-3 cities, marketers say the real challenge may not be demand — but how brands communicate, build trust and measure impact in these markets

by

by

Published: Oct 13, 2025 8:54 AM | 10 min read

What began 7–8 years ago as a few experiments to deliver last-minute groceries has today moved past its “emergency orders” phase. Quick commerce has evolved to serve a larger audience, with bigger baskets and a wider variety of products than ever before. And the numbers back this transformation. According to CareEdge Ratings, Indians ordered goods worth Rs 64,000 crore from quick-commerce platforms like Blinkit and Instamart in FY25 — more than double the Rs 30,000 crore recorded in FY24.

Interestingly, the report also noted that the gross order value (GOV) is expected to grow more than threefold, reaching Rs 2,00,000 crore by FY28. Along with this expansion, Q-comm platform revenues have also surged, reaching Rs 10,500 crore in FY25, up from Rs 450 crore in FY22. And leading the race has been Blinkit, Zepto and Swiggy Instamart, whose growth trajectory has been clearly reflected in their last two years top line. Redseer notes that the sector grew at 150% YoY during the first five months of 2025, driven by dark store expansion, category diversification, and wider selection.

Also read: How quick commerce brands bet on humour to win the season

Now, it looks like the sector is preparing for its next phase of growth, expanding into tier-2, tier-3, and smaller cities. Blinkit, for instance, signalled its intent to test and adapt its model for these markets with a recent front-page ad in Times of India, Indore. The company confirmed its presence in Indore but declined to share an official comment.

Flipkart, too, is transforming last-mile logistics in smaller cities. A few months back, it shared via LinkedIn that with 13% YoY growth from these regions and a delivery network spanning over 13,500 pincodes through its Kirana Partner network. “This isn’t just expansion; it’s strategic infrastructure designed to scale access, speed, and reliability across India’s heartland,” the post said.

Swiggy Instamart has also seen strong traction beyond metros. During its recent Quick India Movement Sales, the platform demonstrated its nationwide reach, with tier-2 cities showing standout growth compared to regular days. It had shared that Bathinda saw an 18-fold increase, Ludhiana 15-fold, and Kota, Meerut, and Amritsar each recorded a 12-fold rise. Udaipur led in fastest 10-minute deliveries, followed by Panipat, Goa, Thrissur, Madurai, Meerut, Palakkad, and Kanchipuram.

Also read: Q-comm ad rates climb 50% in a year

As quick commerce platforms eye Tier-2 and Tier-3 cities, marketers say the real challenge may not be demand — but how brands communicate, build trust, and measure impact in these fragmented, vernacular-heavy markets.

“The appetite is evident, though it is at a different scale compared to metros,” said Uday Mohan, COO, Havas Media India & Havas Play. “Consumers in Tier-2 and Tier-3 cities are increasingly aspirational and seeking the same convenience their metro counterparts enjoy. While order volumes may be smaller today, repeat usage is steadily growing, especially among younger households and nuclear families who value time and ease of access.”

Media execution becomes the real test

As quick commerce expands beyond metros, the real test lies in how effectively brands can localise and sharpen their media execution. There’s clear demand brewing in smaller cities, even if it’s at a different scale.

However, converting that appetite into consistent usage would require localised, and sharper media execution. According to experts, delivery infrastructure and logistics can be inconsistent, and payment preferences vary significantly between markets. Digital literacy levels also differ, which impacts how communication is received and acted upon. “For brands, this makes it important to design campaigns that are localised, relevant, and measured with a sharper lens than in metros,” Mohan added.

Adding perspective to this, Rashi Bhushan, AVP - Digital Planning & Buying, Mudramax, explained that media strategies in smaller cities need a complete reset. “The first hurdle is infrastructural unevenness, connectivity gaps, inconsistent delivery networks, and fragmented data ecosystems make it even harder to deploy and measure campaigns effectively.”

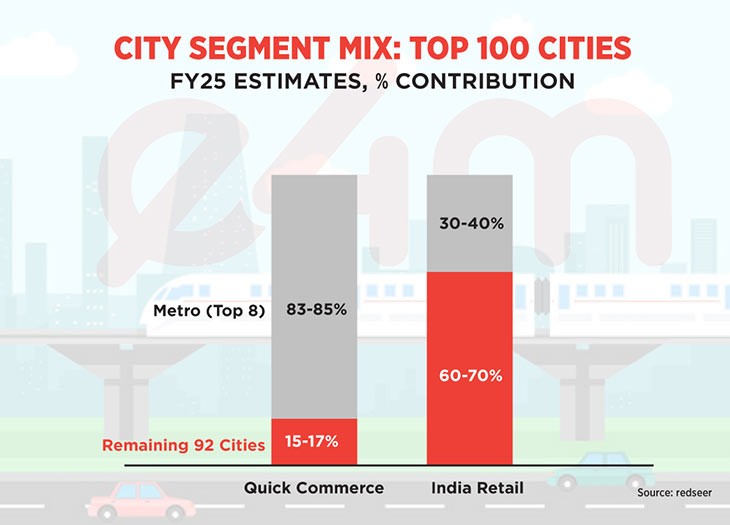

A report by Redseer has pointed out that orders per day per dark store drop sharply below 1,000 beyond the top 10–15 cities and below 700 in the next 20 cities, reflecting the operational challenge of scalling the model outside metros.

According to Bhushan, many users in Tier-2 and Tier-3 towns are still new to online ecosystems — they engage through short-form video, vernacular content, and micro-influencer communities rather than mainstream digital channels. So, communication needs to be more local, visual, and trust-oriented, rather than overly transactional.

Payment behaviour also shapes how campaigns are planned and measured. While UPI usage is rising, cash-on-delivery remains the preferred mode in several micro-markets. “This affects how conversion and attribution are tracked, and it means campaigns must play a dual role — driving awareness as well as building confidence in digital payments. Most measurement frameworks are still metro biased. In smaller towns, reach and impact are best understood through a blend of digital metrics and local insights — integrating online engagement data with on-ground feedback from retailers or delivery partners,” Bhushan said.

But what’s actually driving early growth in these towns, as per media buyers, is that groceries and FMCG categories are leading adoption, followed by personal care. “Groceries and FMCG are leading adoption, given their high frequency and immediate need states,” said Mohan. “Personal care is also gaining traction, particularly among younger cohorts who are aspirational and more open to experimenting with new products.”

Bhushan added that for consumers in smaller towns, quick commerce isn’t just a convenience; it’s an access revolution. “In cities like Indore, Lucknow, and Bhubaneswar, consumers are seeing 10–20-minute delivery as a way to bridge availability gaps rather than as a lifestyle perk. Groceries and staples lead the pack — driven by predictable demand and freshness assurance. Branded FMCG goods are seeing sharper growth curves due to price competitiveness and promotions. Personal care and beauty products have emerged as a dark horse category, driven by aspirational consumption,” she said.

How viable will this model be?

In the recent past, many reports have pointed out the viability of these towns. Bernstein report has estimated that the industry will grow 75% YoY, far outpacing traditional retail, which is projected to grow in the low teens. The report also mentioned that new categories and tier-2+ cities will drive this next phase of growth. Another report by brokerage Emkay has stated that non-metro towns are increasingly economically viable due to favorable unit economics. With nearly 8,000 SKUs on offer (compared to around 1,000 at a typical local kirana) quick commerce platforms are catering to growing demand for variety and convenience outside metros.

Even brands like ITC have seen strong growth in quick commerce accounts across Tier 2 and Tier 3 towns, with their footprint now expanded to over 240 locations. “Quick commerce is a critical growth driver for us, and we are actively partnering with leading platforms to leverage this opportunity. We are strengthening our presence through the right assortment, agile supply chains, enhanced discoverability, and close collaboration with platform partners for seamless integration and on-app investments. As consumers in smaller towns become more digitally connected and aspirational, they are up-trading across premium SKUs and seeking better packaging and innovative products,” Sandeep Sule, Divisional Chief Executive, Trade Marketing and Distribution, ITC Ltd told e4m.

While experts and many reports have pointed out that there is huge demand for online orders and quick deliveries in small cities, to really make this model work, brands and quick commerce platforms will have to step into the shoes of retail stores.

According to Sameer Gandotra, founder of Frendy, an Ahmedabad-based grocery chain, “Blinkit, Zepto, and similar players mostly operate in richer, urban, high-density areas. In smaller cities, they are available, but the demand for urgent delivery is lower due to more domestic help and larger families. Cost is also a factor, so people tend to optimise their basket.”

He added, “Marketing and community engagement are key. Targetting housing societies—through billboards, kiosks, or sponsoring events—works best, as these areas offer high density. Quick commerce is critical, but ultimately it’s an optionality people can choose to use.”

Beyond the metro mindset

In many small towns, the demand for quick deliveries and online orders has largely been fulfilled by local kirana stores, where customers place orders over the phone or via WhatsApp, or rely on their friendly shopkeeper to deliver promptly. These stores have long been the backbone of immediate convenience, often catering to the community’s needs at no extra cost. To succeed, quick commerce platforms must deliver quickly and earn the deep-rooted trust that consumers have long placed in local retailers

Alok Chawla, Serial Entrepreneur and Founder of Kiko Live, a platform that has digitised small-town kirana stores to provide quick commerce-like service pointed out that for these models to work profitably beyond metros, a typical dark store needs a population density that can support at least 1,000 orders a day. In smaller towns, the population is often more spread out, reducing density per square kilometre, which makes a high-SKU, dark-store-led model difficult to sustain. “What could work is a hybrid model, where quick commerce players keep a few hundred extremely fast-moving SKUs in dark stores while leveraging neighborhood kirana inventory for the long-tail products,” he explained.

Similarly, Gautam Kapoor, COO of Shiprocket, highlighted that profitability beyond metros requires high local order density (around 1,000+ daily orders within a 2–3 km radius), compact dark stores in high-demand zones, and efficient fleet utilisation with 4–6 deliveries per rider per hour. Success also depends on optimising last-mile routes, leveraging shared infrastructure, and using data to match inventory with demand in real time.

Expanding into smaller towns, however, comes with a distinct set of operational and market challenges. These include logistical complexities from dispersed demand, higher warehousing and last-mile delivery costs, and the price-sensitive nature of consumers, which requires balancing affordability with speed and service quality. Building consumer trust also takes time, as many shoppers continue to rely on familiar local sellers. Infrastructure constraints, such as limited connectivity and availability of delivery hubs, further impact scalability. Achieving sustainable growth in these markets requires continuous investment in technology, smarter resource planning, and deeper collaboration with local partners to ensure consistent and reliable service, shared Kapoor, whose company powers last-mile delivery logistics across smaller towns.

The next phase of quick commerce

Early adoption in these markets is being driven primarily by groceries and FMCG, with personal care and beauty products emerging as aspirational categories. According to experts, platforms must contend with low population density, dispersed demand, infrastructure gaps, and cash-dominated payment preferences, all of which affect profitability.

Redseer in its report has emphasised that creating a profitable play in smaller cities is a steep ask: lower demand maturity leads to smaller average order values, larger delivery radii, and higher delivery payouts — increasing the breakeven dark store throughput by 1.5–2x versus metros.

The next wave of growth will depend on how effectively platforms integrate with small-town realities — from localised media execution and vernacular campaigns to hybrid fulfilment models leveraging kiranas. Marketers will need to focus on trust-building, aspirational product offerings, and measurable campaigns, while platforms work on unit economics, dark store optimisation, and community engagement.

As consumers in Tier-2 and Tier-3 towns become more digitally connected and aspirational, the opportunity for quick commerce to expand is clear — but success will hinge as much on execution, local insights, and strategic prioritisation as it does on technology or speed.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News