From expansion to optimisation: Is Netflix entering a recalibration phase?

After walking away from Warner Bros. Discovery, Netflix sharpens focus on advertising, live programming, content ownership and ARPU; India could be a key testbed for its next growth phase

by

by

Published: Apr 20, 2026 9:10 AM | 10 min read

- Netflix has decided to abandon its bid for Warner Bros. Discovery, marking a strategic shift from expansion to optimization, focusing on efficiency and monetization rather than subscriber growth.

- The company's Q1 2026 results showed an 82% increase in profit to $5.23 billion, indicating that its new monetization strategies, including pricing, advertising, and engagement, are already yielding positive results.

- Netflix's advertising business is rapidly growing, with over 60% of new sign-ups in ad-enabled markets opting for the ad-supported plan, and the company expects to generate nearly $3 billion in ad revenue this year.

- The streaming service is prioritizing content ownership and live programming as key growth areas, aiming to build its own franchises and enhance viewer engagement, particularly in competitive markets like India.

In many ways, Netflix’s decision to walk away from its much-speculated bid for Warner Bros. Discovery marks the end of one chapter—and the beginning of another.

For over a decade, the streaming giant’s playbook was defined by scale: more subscribers, more markets, more content. The Warner deal, had it materialised, would have accelerated that ambition—offering instant access to one of the deepest content libraries in the world.

But in stepping back, Netflix has signalled something far more significant: scale alone is no longer the goal. Efficiency is.

“This is a reset moment,” said a senior global media executive. “Netflix is moving from expansion mode to optimisation mode. The question is no longer how big it can get, but how effectively it can monetise what it already has.”

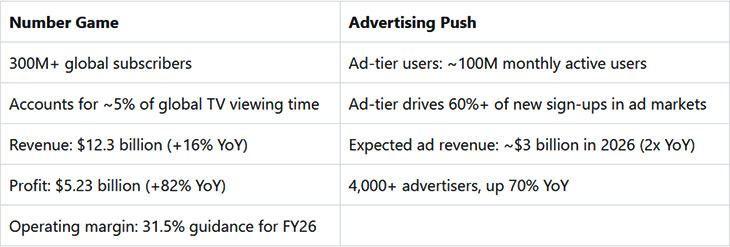

The timing of this strategic pivot is telling. In its Q1 2026 results declared globally on Thursday, Netflix reported an 82% year-on-year surge in profit to $5.23 billion—underscoring that its shift towards monetisation is already beginning to pay off.

The timing of the transition is hard to ignore. Co-founder Reed Hastings will step down from the board in June, shortly after the Warner Bros. Discovery deal fell through—although Netflix has been careful to position the move as independent of the aborted acquisition.

Monetisation playbook: Pricing, ads & engagement

At the heart of Netflix’s strategy lies a three-pronged framework—pricing, advertising and engagement—each designed to maximise revenue per user rather than merely expand the subscriber base.

As of early 2026, Netflix’s global ARPU stands at around $16, led by the U.S. and Canada where it exceeds $17, according to Business of Apps. While periodic price hikes continue to lift ARPU, growth is carefully balanced through lower-priced and ad-supported tiers—particularly in price-sensitive markets such as APAC.

In India, the platform operates across four plans—Mobile (Rs 149), Basic (Rs 199), Standard (Rs 499) and Premium (Rs 649)—catering to a wide spectrum of users, from mobile-first individuals to multi-device households.

A defining aspect of Netflix’s pricing strategy is its discipline. The company has consistently avoided discount-led growth—offering no annual plans, festive deals or special pricing cohorts. In contrast, rivals such as Disney, Paramount, Peacock and WBD have relied heavily on deep discounting, often cutting prices by 50% or more to drive acquisition. While effective in the short term, this approach compresses revenue and hinges on uncertain long-term retention. Netflix, notably, has avoided this trade-off.

The divergence is visible in ARPU trends. Netflix’s ARPU in the U.S. and Canada rose from $13.84 in Q4 2020 to $17.26 in Q4 2024, despite relatively measured price increases. Disney+, on the other hand, saw domestic ARPU move from $6.10 in Q4 2022 to $7.70 in Q4 2024—even after more frequent and steeper hikes.

What makes this trajectory more notable is Netflix’s simultaneous push into advertising. Since launching its ad-supported tier in 2022 at $6.99, over half of new subscribers in ad-enabled markets have opted for the plan. Yet, despite this apparent downtrading, overall ARPU has continued to expand—highlighting the resilience of its pricing architecture and its ability to monetise across tiers without diluting value.

“This is classic yield management,” said an industry analyst. “You segment your audience and maximize value from each layer.”

The financials reinforce this shift. Revenue rose 16% year-on-year to $12.3 billion in Q1 2026, driven by a combination of pricing, subscriber momentum and a rapidly scaling ads business.

Alongside monetisation, Netflix is deepening engagement. Gaming is emerging as a key lever, particularly among younger audiences. The launch of its standalone kids-focused gaming app, coupled with early traction in cloud gaming, signals a broader move towards a multi-format entertainment ecosystem. Nearly 10% of kids’ profiles are already engaging with games, while close to half consume content on mobile devices—underscoring the convergence of video and interactive formats.

India: The next battleground for ads

Advertising, meanwhile, is fast emerging as Netflix’s most decisive growth lever—and India could be its most complex test.

“Building out our ads business has been a major monetisation priority and we continue to make good progress,” Netflix said in its Q1 2026 financials.

Its ad-supported plan already accounts for over 60% of new sign-ups in ad-enabled markets, with the company expecting to clock nearly $3 billion in ad revenue this year—double that of 2025. Netflix now works with over 4,000 advertisers globally, a 70% year-on-year increase—signalling that its ads business is no longer experimental, but foundational.

That signal has firmly put India on the radar.

“Honestly, it’s not if, it’s when,” said Divya Dixit, CEO at Recz, and a long-time veteran of the OTT space. “Netflix already has a global ad tier with over 40 million users and is doubling down with its own ad tech and AI-led formats. In a market like India, which is heavily AVOD-led, the move is logical.”

Yet, the disruption may be more nuanced than immediate.

“This won’t be an overnight shake-up. Platforms like YouTube and JioHotstar operate at massive scale. Netflix will likely win premium ad inventory—not volume. It’s less a mass disruptor and more a high-value advertiser magnet,” she added.

Pep Figueiredo, COO, PTPL India and former SonyLIV executive, offers a more measured timeline.

“Netflix has likely evaluated the ad model extensively for India and may continue piloting it with a curated segment of its user base. But an immediate rollout may not be essential, given Jio’s dominance and the already cluttered AVOD landscape,” he said.

Regionally, Asia-Pacific has emerged as Netflix’s fastest-growing market, with India playing a critical role alongside Korea and Southeast Asia—driven by consistent execution across content, pricing and format innovation.

Content: From acquisition to ownership

If advertising defines Netflix’s present, content ownership will shape its future.

Netflix offers a massive, constantly updated library of over 3,600 movies and 1,800 TV shows, including award-winning originals, documentaries, and anime. Popular content spans diverse genres, featuring hits like Stranger Things, Bridgerton, Squid Game, and The Witcher. Users can watch on multiple devices, with new content added weekly.

It wanted to expand its content slate further by acquiring Warner Bros Discovery and its OTT platform HBO Max. The combined Netflix–WB (after separation of Discovery Global from the group in Q3 2026) entity would have commanded an estimated $70 billion in revenue next year—surpassing Disney and YouTube’s combined ARR.

After acquisition it would have got hold of the marquee HBO originals such as Harry Potter, Friends, Big Bang Theory, Game of Thrones and The Office.

“As the deal is off the table, Netflix is no longer chasing growth at any cost—it is prioritising control, efficiency and long-term value creation,” an industry observer noted.

Importantly, the company’s leadership has framed the decision as a test of discipline rather than a missed opportunity. Co-CEO Ted Sarandos told analysts the process helped “test investment discipline,” adding that the Warner assets were “nice to have, not a need to have.”

With over 300 million subscribers globally, the focus is now on building franchises that can travel across markets and sustain engagement over time.

For India, however, execution will be critical.

“India runs on regional and culturally rooted content,” said Dixit. “Netflix is moving towards ‘ownable moments’ and local storytelling rather than just buying large libraries. It’s a shift from breadth to depth.”

Figueiredo adds that the company’s strengthened financial position—supported by the $2.8 billion break-up fee—gives it the flexibility to sharpen both owned and licensed content strategies, with global recalibrations likely cascading into India.

But consistency remains the real test.

“Netflix’s strength is premium storytelling that drives cultural conversation,” Dixit noted. “But in India, one big hit isn’t enough—you need a steady pipeline across languages. Ads and pricing can bring users in, but retention depends on relevance and frequency.”

Without Warner’s IP, Netflix must now build its own franchises organically—a slower, more capital-intensive path, but one that ensures long-term control.

“Buying IP is always faster than building it,” said an industry executive. “But building gives you ownership, longevity and flexibility.”

Netflix continues to emphasise that strong content drives retention, repeat viewing and word-of-mouth growth, with its internal quality metrics hitting an all-time high in Q1.

Live content: The new growth engine

If advertising is the revenue engine, live programming is increasingly the fuel powering it. Netflix’s push into live events—from sports to global cultural programming—is closely aligned with its ad ambitions. Live content delivers what on-demand cannot: urgency, scale and real-time engagement.

The World Baseball Classic in Japan, which drew 31.4 million viewers and drove the country’s biggest sign-up day, underscores this potential—creating not just subscriber spikes, but high-impact advertising moments.

“Live is where the next phase of monetisation lies,” said a streaming executive. “It brings appointment viewing back into streaming—and advertisers love that.”

Competition and pursuit of supremacy

Netflix has maintained its full-year guidance of $50.7–$51.7 billion in revenue and an operating margin of 31.5%—a signal that its pivot towards advertising and monetisation is not cyclical, but structural.

Its transformation reflects a broader shift in the streaming industry. The first phase of the streaming wars was about acquiring users at scale. The second is about extracting value—monetising those users efficiently.

“The real battle now is not for subscribers—it’s for time, attention and revenue per user,” said a senior industry executive. The competitive dynamics in streaming are increasingly defined by what each platform optimises for—and on that count, Netflix continues to hold a distinct edge on monetisation.

With over 300 million global subscribers (as last disclosed) and ARPU in mature markets such as the US and Canada crossing the $17 mark, Netflix generates significantly higher value per user than most of its rivals. By comparison, platforms such as Disney+ operate at a much lower global ARPU—often in the $4–$7 range—driven by price-sensitive markets like India.

This divergence highlights a deeper structural split in strategy. Platforms like JioHotstar are built on scale—leveraging mass-market pricing, sports-led spikes and advertising reach to drive volumes. Meanwhile, Amazon Prime Video operates within a bundled ecosystem, where video consumption is only one part of a broader value proposition tied to e-commerce and memberships, making direct comparisons on subscriber value or ARPU less straightforward.

Engagement adds another layer to this competitive equation. Netflix claims that it accounts for roughly 5% of total global TV viewing time—an important signal of depth and habit, not just reach. While Amazon has recently pushed its ad-supported inventory to reach over 200 million users globally, and Netflix’s own ad tier is now approaching nearly 100 million monthly active users, the nature of engagement varies widely.

“Netflix’s decision to stop reporting subscriber numbers and ARPU on a quarterly basis marks a strategic shift in how it wants to be evaluated. The focus is no longer on scale alone, but on revenue growth, profitability and long-term monetisation efficiency,” said an ad executive.

Netflix seeks to rewrite its own playbook—not by getting bigger, but by getting smarter.

e4m reached out to Netflix for participation in the story; however, the platform did not provide an official comment.

Read more news about Digital Media, Internet Advertising, Marketing News, Television Media, Radio Media

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News