Are broadcasters entering a phase where subscriptions will be key in revenue stability?

Industry experts say that while linear TV subscription is shrinking with fewer cable homes and operators reducing payouts, digital subscription is growing but not fast enough

by

by

Published: Nov 20, 2025 9:13 AM | 5 min read

The Indian video market is undergoing a structural shift shaped by cord cutting, digital migration, expensive content acquisition and stagnating linear television viewership. As consumption moves steadily towards streaming, platforms are benefiting from flexible pricing models and premium content that helps add paying subscribers.

Subscription revenues across major broadcasters have begun to rise, yet the gains remain insufficient to meaningfully counter the decline in advertising income.

The financial performance of leading networks shows that while digital adoption is rising, it is not expanding fast enough to offset the deeper, faster erosion in traditional monetisation channels.

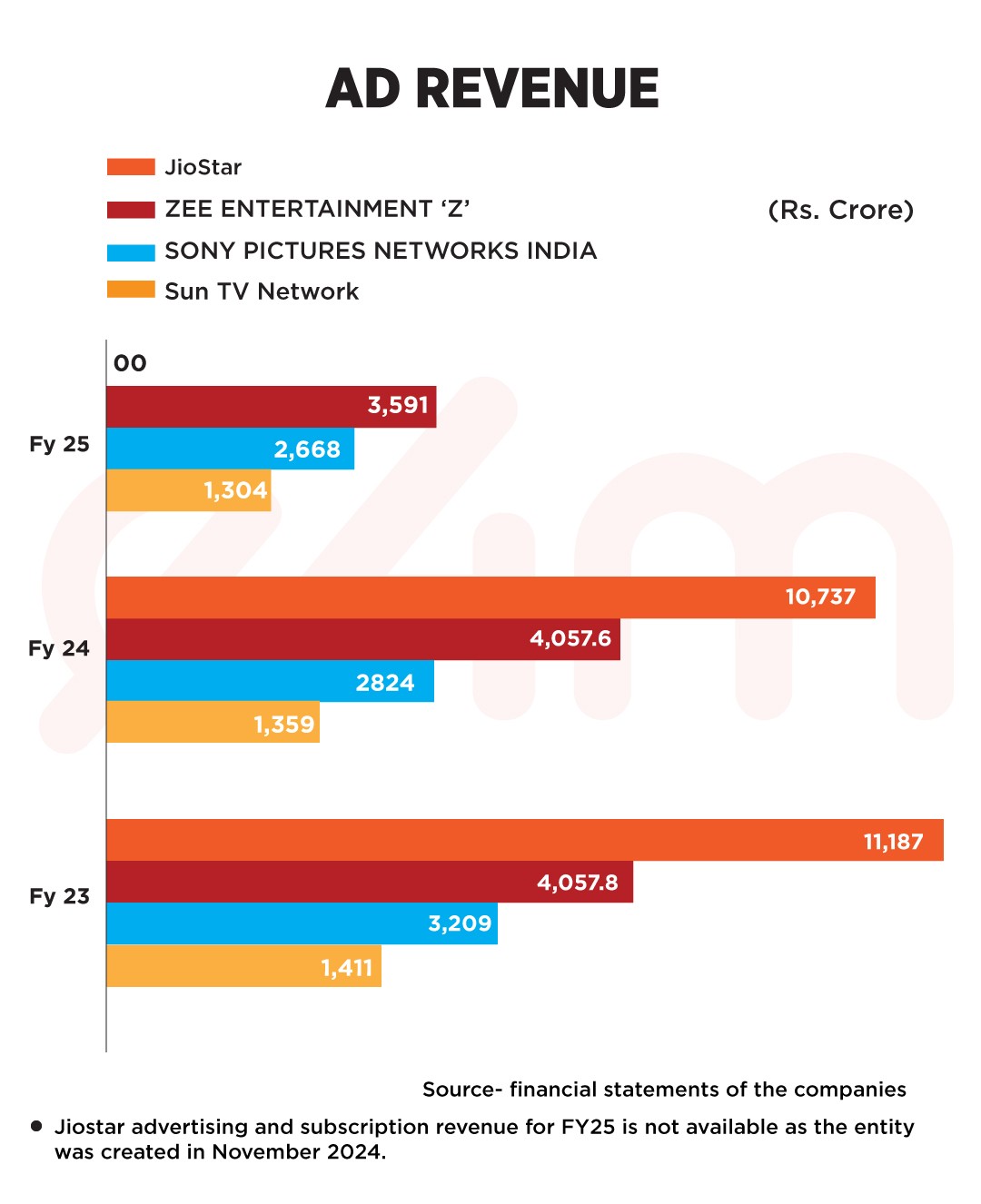

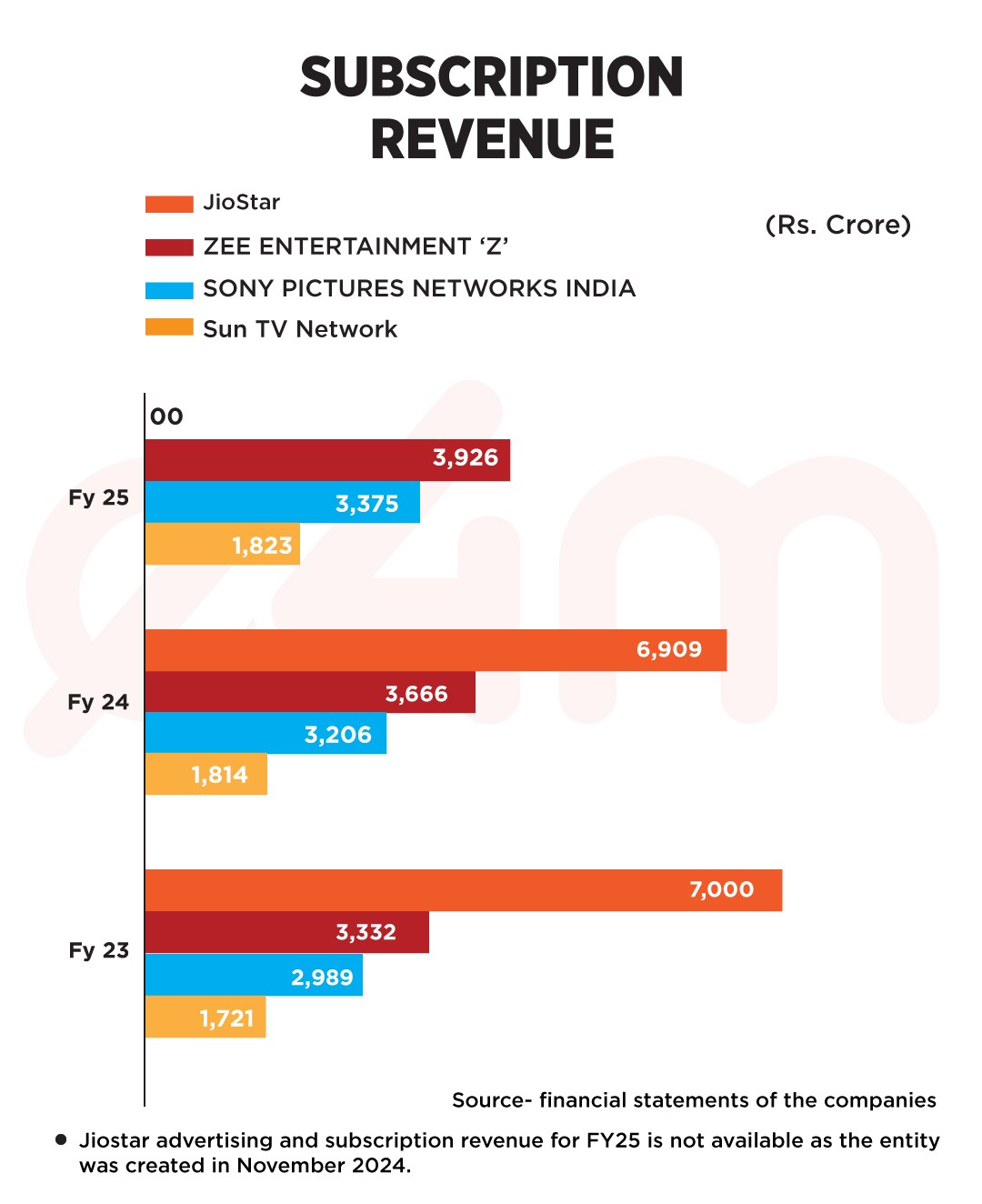

Zee Entertainment’s results underline this widening gap. Its subscription revenue rose to Rs 3926 crore in FY25 from Rs 3666 crore in FY24 and Rs 3332 crore in FY23, driven by OTT pricing adjustments and growing digital usage. But advertising income fell to Rs 3591 crore in FY25 from Rs 4057 crore in both FY24 and FY23.

Read e4m report on Zee's Q2 FY26 performance

Quarterly numbers show an accelerating downturn. ZEEL’s ad revenue for Q2 FY26 fell to Rs 806 crore from Rs 901 crore a year earlier, and Q1 FY26 declined to Rs 758 crore from Rs 911 crore in Q1 FY25. For the first half of FY26, ad income dropped to Rs 1564 crore from Rs 1813 crore in the same period last year.

Subscription trends moved the other way. ZEEL’s subscription income rose to Rs 1023 crore in Q2 FY26 from Rs 970 crore a year earlier, and H1 FY26 subscription revenue reached Rs 2004 crore compared with Rs 1957 crore in H1 FY25. Yet this increase is not enough to compensate for the sharper fall in advertising.

ZEEL’s total revenue for FY25 slipped to Rs 8417 crore, down from Rs 8766 crore in FY23, a reminder that subscription growth alone cannot lift overall revenue. Even cost rationalisation, including reductions in media content and telecast expenses from Rs 5039 crore in FY24 to Rs 4517 crore in FY25, only partly cushions the underlying weakness.

Sony Pictures Networks India shows a similar pattern. Subscription revenue rose from Rs 2989 crore in FY23 to Rs 3206 crore in FY24 and Rs 3375 crore in FY25, while advertising revenue continued to weaken, falling to Rs 2668 crore in FY25. The company’s total revenue still declined in FY25 despite rising subscription income, weighed down by soft advertising, higher production costs and lower licensing income.

Read e4m report on SPNI's net profit down to nearly half

Sun TV Network mirrors the industry trend. Its ad revenue for Q2 FY26 fell to Rs 292 crore from Rs 335 crore in Q2 FY25, and Q1 FY26 was similarly weaker at Rs 290 crore compared to Rs 323 crore the previous year. For H1 FY26, ad revenue fell to Rs 582 crore from Rs 658 crore in H1 FY25.

Sun TV posts 30% growth in Q2 revenue

Subscription income, however, continued to rise steadily. It reached Rs 476 crore in Q2 FY26 up from Rs 437 crore in Q2 FY25, and H1 FY26 subscription revenue totaled Rs 946 crore compared with Rs 862 crore a year earlier. The annual trend reinforces the same story with subscription revenue rising from Rs 1721 crore in FY23 to Rs 1814 crore in FY24 and Rs 1823 crore in FY25 while advertising continued to contract.

According to industry experts, the situation is even more complex for JioStar, which now houses the former Star India operations.

After the reorganisation into JioStar the company reported Rs 11035 crore in revenue for the period from November 14 2024 to March 31 2025. In FY26 it posted Rs 11222 crore in Q1 and Rs 7232 crore in Q2 taking first half revenue to Rs 18454 crore. Analysts believe digital subscription is likely growing for JioStar driven by Hotstar and JioCinema but the pace remains measured.

Although FY25 advertising figures are undisclosed, past numbers show a slowdown was already in play with ad revenue at Rs 10737 crore in FY24 and Rs 11187 crore in FY23.

Subscription revenue was relatively stable at Rs 6909 crore in FY24 and Rs 7000 crore in FY23 without strong expansion.

Industry experts point out that subscription now exists in two distinct buckets. Linear TV subscription, which is shrinking as cable homes disconnect and operators reduce payouts, and digital subscription that is growing but not fast enough to outpace the losses on the linear side.

Even spikes driven by premium events contribute only temporarily and often fail to cover the soaring cost of acquiring such properties. Rights for marquee sports, especially the IPL, are cited as examples where revenue grows on paper but profitability erodes because the investment required has reached unsustainable levels.

The revenue equation for broadcasters is increasingly defined by a three-way squeeze, said experts.

Content costs are rising as the battle for premium programming intensifies. Linear subscription revenue is shrinking due to cord cutting and operator discounts. Traditional TV advertising is declining because advertisers are reallocating budgets toward digital channels and shifting brand strategies in favour of targeted digital formats.

Only one stream - digital subscription - is growing, and even that growth is steady rather than explosive, they said, adding that as a result the subscription uptick is not translating into meaningful profit gains.

Broadcasters find themselves in a phase of loss minimisation using digital gains to slow the pace of decline while absorbing structural shocks in linear television.

The industry consensus is that subscription revenue alone cannot compensate for the advertising slump and advertising on television cannot recover unless viewership stabilises.

The near-term challenge for broadcasters is to navigate a landscape where digital grows gradually, cable shrinks steadily, ad budgets migrate to digital, and content inflation remains unchecked. The longer-term shift points to a more digital centric ecosystem but the transition period will continue to place significant pressure on revenue stability and profitability.

Read more news about Television Media, Digital Media, Advertising India, Marketing News, PR and Corporate Communication News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News