Why auto brands cut back on ads even as sales hold up

Exclusive TAM AdEx data accessed by e4m shows a visible moderation in auto advertising between January and April 2026, across television, print and digital

by

by

Published: Jun 11, 2026 9:04 AM | 6 min read

- India's automobile sector is experiencing rising vehicle sales alongside a cautious approach to advertising, particularly in television, where ad volumes dropped significantly from January to April 2026.

- Despite the decline in ad spending, retail sales of vehicles, including two-wheelers and passenger cars, have shown strong growth, with notable increases reported by the Federation of Automobile Dealers Associations in February, March, and April.

- The advertising landscape is shifting, with brands becoming more selective in their media spends, focusing on efficiency and ROI, and increasingly utilizing digital platforms for consumer education, especially regarding electric vehicles (EVs).

- Industry experts indicate that the auto sector's media strategy is evolving from broad-based advertising to a more integrated approach, aligning media choices with the consumer journey rather than traditional channel-specific tactics.

India’s automobile sector has started 2026 with an advertising paradox: sales are rising, but media spends appear to be turning cautious.

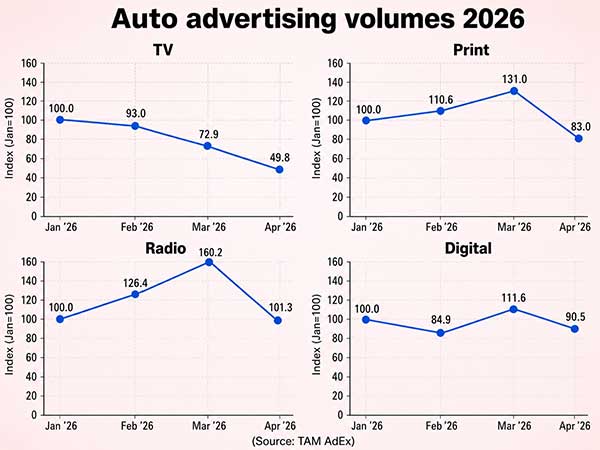

Exclusive TAM AdEx data accessed by e4m shows auto advertising volumes softened across key media between January and April, with television seeing the sharpest pullback. TV ad volumes for auto brands fell from an index of 100 in January to 50 in April, declining steadily through February at 93 and March at 73. The drop is significant because television remains a key medium for auto brands during launches, sports-led campaigns and mass awareness pushes.

Other media showed less linear trends. Print rose from 100 in January to 131 in March before falling to 83 in April. Digital slipped to 85 in February, recovered to 111.6 in March and settled at 90 in April. Radio was relatively resilient, rising to 160 in March before easing to 101 in April. The data suggests the pullback was not uniform, but April clearly reflected a more cautious advertising stance after the March push.

The moderation comes even as vehicle sales have continued to grow. According to the Federation of Automobile Dealers Associations, retail sales across key categories, including two-wheelers, passenger vehicles and commercial vehicles, have been rising in recent months. FADA described February as the best-ever month with 25% year-on-year growth, March as historic with another 25% jump, and April again as the best-ever April with 13% year-on-year growth.

Notably, auto was one of the few large categories that held up strongly in 2025, even as several other sectors saw pressure. According to the Pitch Madison Annual Report 2026, auto is the country’s third-largest advertising category after FMCG and e-commerce. Across TV, print and radio, auto spends grew from ₹5,266 crore in 2024 to ₹5,548 crore in 2025, a 5% increase that added ₹281 crore to the ad market.

Print led that growth, rising 8% from ₹2,803 crore to ₹3,036 crore. Radio grew 13% from ₹266 crore to ₹299 crore, while TV remained broadly flat at ₹2,212 crore. The resilience reflected auto’s position as a high-involvement category where print offers detail and credibility, radio supports dealer-led local pushes, and television builds visibility around major launches.

Industry observers say the early-2026 slowdown should be read against a high base, tax-led demand support and a changing media mix. Auto advertising is increasingly being split across brand campaigns, variant launches, dealer activation, EV education, festive pushes, digital lead generation and retail conversion. As a result, brands are becoming more selective about where and when they spend.

According to Veteran adman Dr Sandeep Goyal, MD of Rediffusion, “Sales are up due to price, not persuasion.”

According to Goyal, GST cuts announced in September 2025 changed the economics of the category. Taxes on SUVs above 1500cc dropped from 50% to 40%, while GST on small cars came down from 28% to 18%, leading to price cuts of nearly ₹1 lakh across categories. “You needed to advertise the price drop, not the car,” he said.

He added that dealer dispatches and registrations also reflected a strong price-led push. “When the government hands you a ₹1 lakh discount, you don’t need 30-second TVCs to convince people. You need to educate them that the discount exists. That’s fewer GRPs, more tactical spend,” Goyal said.

TAM data shows Maruti Suzuki, the largest advertiser in the category, continued to dominate print, digital and radio advertising, while TVS Motor Company led television during January-April. Tata Motors remained among the top advertisers across television, print and digital, reflecting its strong presence across passenger vehicles and EVs.

e4m reached out to all leading car and two-wheeler companies for comment. Their responses were awaited at the time of publishing.

TV important, but not at the cost of other media

The decline in auto advertising appears largely tactical, not structural. After a launch-heavy 2025 driven by SUVs, EVs and premium vehicles, brands are normalising spends, says Vinay Hegde, CEO Investments (Media), Madison World.

“Advertising growth is decoupling from sales growth with marketers becoming more ROI-focused amid margin pressures, inventory considerations and a more cautious consumer environment,” Hegde noted.

He emphasises, “TV remains important but investments are becoming more concentrated. Brands are prioritising high-attention content rather than maintaining broad-based, always-on TV presence and hence volume shows a decline. Digital and CTV are gaining share for consideration and conversion. The future media model is integrated rather than channel-specific.”

Echoing the sentiments, Tarun Nigam, media consultant and ex-WPP and ex-Publicis, says, “The auto sector is moving from ‘growth mode’ to ‘efficiency mode’ or ‘efficacy mode’. While 2025 was fuelled by launches, premiumisation, SUVs and EV-led excitement, 2026 is seeing CFOs enter the media room.”

Nigam explains, “The bigger story is not lower spends but smarter spends. Brands are questioning whether every GRP, every burst and every festive spike is delivering incremental sales. That naturally hurts TV first because it is the largest line item. There is also a deeper behavioural shift. Consumers today are researching more, postponing purchases longer and expecting financing comfort before decision-making. In such a market, marketers become cautious even when topline demand looks healthy.”

Auto media planning is going through its biggest rewiring in years. Earlier, awareness itself was the funnel. Today, awareness is just the entry ticket, according to Nigam. “TV is becoming more event-led and impact-led rather than always-on. Print is surviving because auto remains a trust category — consumers still want details, offers, specs and local dealer reassurance. Radio remains tactical and hyperlocal.”

EV growth complicates the media playbook

The moderation comes at a time when the auto market itself is becoming more complex. India’s passenger vehicle market, estimated at around ₹4.5 lakh crore by industry observers, is seeing sharper competition across SUVs, premium vehicles, hybrids and electric cars. EV adoption is also expanding, with total EV sales touching 2.3 million units in 2025 and accounting for nearly 8% of new vehicle registrations, according to Vahan Portal data cited by industry trackers.

This is changing how auto brands use media. EVs and hybrids require more explanation than conventional vehicles, with buyers seeking clarity on range, charging, battery life, total cost of ownership, resale value and incentives.

“The biggest shift is digital becoming the education layer. EVs, hybrids, connected cars and premium vehicles cannot be sold only through glamour shots and celebrity films. Consumers want battery economics, charging reassurance, ownership costs, technology explainers and comparison content,” said Tarun Nigam.

Industry experts estimate that digital now accounts for roughly 35% of auto advertising expenditure, followed by print at 33% and television at 27%. This means any reduction in auto budgets is likely to be felt most sharply by digital and print, though television also remains exposed because of its higher campaign ticket sizes.

The emerging media mix is therefore less about mass versus targeted advertising, and more about matching media to the consumer journey. TV and CTV help build aspiration and trust, print supports detail-rich explanation, digital drives research and lead generation, while radio and OOH continue to support dealer-level activation and test-drive campaigns.

“The future auto mix is not mass versus targeted. It is mass for aspiration and digital for reassurance. The winners will be brands that stop planning media channel-wise and start planning consumer-journey wise,” Nigam said.

Read more news about Marketing News, Advertising News, PR and Corporate Communication News, Digital News, People Movement News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News