India flags slower growth amid Iran tensions; AdEx outlook faces downside risks

GDP growth projections of 7–7.4% for FY27 face considerable downside risks, GoI has said; inflation, falling rupee & sensex volatility may soften consumption and impact advertising, experts warn

by

by

Published: Apr 3, 2026 8:59 AM | 5 min read

India has flagged rising risks to its economic outlook amid escalating tensions in Iran, signalling a potential slowdown in growth alongside widening fiscal and external pressures in the new fiscal beginning April 1.

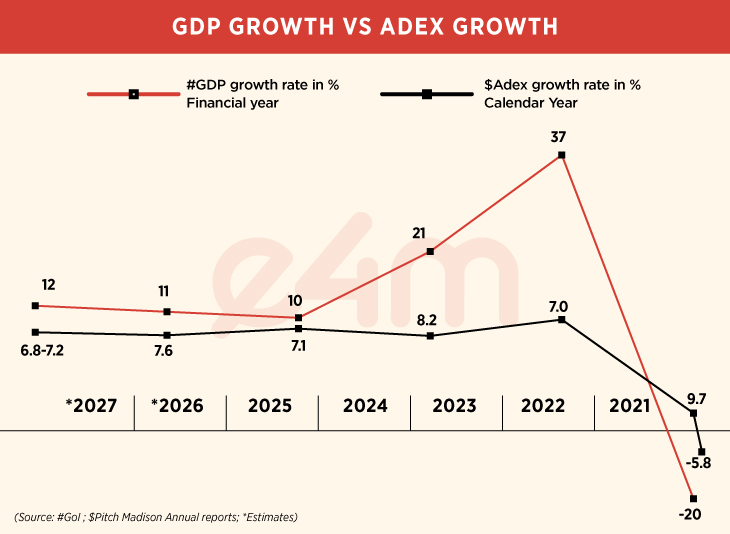

In its March 2026 economic review, Chief Economic Adviser V. Anantha Nageswaran said GDP growth of 7.0–7.4% for FY27 faces “considerable downside risks,” driven by elevated crude prices and geopolitical uncertainty. For an energy-import dependent economy like India, the transmission is immediate—higher input costs, rising inflation and pressure on the rupee, which recently crossed 95 against the dollar.

Early signals suggest stress is already feeding into corporate behaviour. Business activity has moderated, inflation—particularly in energy and food—has intensified, and consumption sentiment is softening.

“Most advertisers—primarily in FMCG, fashion, Auto, Aviation and Real Estate—paused campaigns soon after the US-Israel attacks on Iran began on 1 March,” agency leaders told e4m, indicating an immediate freeze in brand activity. The first quarter of the new fiscal year is likely to impact advertising further, marketers say.

Such reactions are typical. Advertising is among the most flexible levers in corporate budgets and tends to respond quickly to uncertainty. Even marginal changes in growth expectations can trigger disproportionate adjustments in AdEx.

A&P budgets cut proactively, not reactively

India’s advertising market stood at ₹1.55 lakh crore in 2025, growing 12% year-on-year, with digital accounting for nearly 60% of spends. Growth for 2026 was projected at 10-13% — a trajectory now under pressure.

“The 10-13% projection assumes a stable macro environment,” said senior industry leader Shubhransu Singh. “Oil shocks impact confidence first. Corporate earnings come under pressure before GDP numbers move, and advertising budgets respond to earnings guidance, not projections.”

Singh expects AdEx growth to moderate to 8–10%, with a sharper correction in the second half. “Advertising and promotion budgets are cut proactively. FMCG companies will protect margins before media plans,” he said.

At the ground level, this shift is already visible. “Two D2C brands we are working with paused brand campaigns this quarter and doubled down on performance—same budgets, different allocation,” said Sahil Gandhi, co-founder of Blushush and Ohh My Brand.

“When GDP softens, brands don’t announce cuts—they start asking for ROAS on everything,” he added, highlighting a growing bias towards measurable outcomes.

Anshika Dhawan, Chief Marketing Officer, Amara Raja Energy & Mobility Ltd, says, “A moderation in GDP growth typically leads to more cautious spending across sectors, and advertising is often one of the first areas where budgets are optimised.”

She advises, “However, having spent a significant part of my career in categories where consumers are not actively engaged all the time changes how you think about it. You focus less on noise, more on trust and reliability You build mental availability over time, not just campaigns And you ensure that when the consumer enters the category, your brand is the obvious choice It’s a more disciplined, long-term way of building brands—but also far more defensible.”

Sectoral stress and widening media divergence

The impact is uneven. FMCG, auto, real estate and MSMEs—sectors sensitive to input costs and demand—are expected to see sharper pullbacks.

“When input costs rise, campaign horizons shrink. A six-month plan becomes a three-month test,” Gandhi noted, adding that delayed auto launches and tighter FMCG spends are already visible.

This is accelerating divergence within media. Digital continues to gain share due to flexibility and measurability, while traditional media—especially television—faces greater vulnerability due to fixed commitments.

Currency pressures add another layer. “A weaker rupee increases the cost of dollar-denominated digital inventory,” Singh said. “Advertisers pay more in rupee terms for the same reach.”

At the same time, MSMEs—a key base for digital advertising—face working capital pressures, which could dampen overall AdEx growth, including on digital platforms.

Cyclical slowdown or structural reset?

While near-term headwinds are evident, industry observers see this as part of a broader structural shift. “Recent years are better viewed as a consolidation phase,” said an industry strategist. “Growth is becoming more selective, driven by sharper allocation and clearer returns.”

This shift is visible in media mix trends. Digital continues to capture incremental spends, while traditional media shows increased volatility. In a constrained environment, performance-led channels are likely to command a greater share of budgets.

The pattern is not new. During the pandemic-induced contraction in FY21, AdEx fell nearly 20% when GDP declined 5.8%. Recovery phases, in contrast, have seen advertising outpace GDP growth, amplifying both downturns and rebounds.

Prolonged uncertainty could also weigh on deal activity in media and entertainment, where valuations depend on growth visibility.

Yet, India’s long-term fundamentals—rising consumption, digital adoption and a young demographic base—remain intact.

“The easy expansion cycle is behind us,” the strategist added. “What lies ahead is more calibrated growth, where efficiency and outcomes matter as much as scale.”

Read more news about Internet Advertising India, Marketing News, PR and Corporate Communication News, Digital Media News, Television Media News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News