Why Pay TV remains prime in the broadcasting universe

While digital streaming is rapidly growing, Pay TV continues to hold its ground in India’s media ecosystem, especially in sports and premium entertainment categories, share industry heads

by

by

Published: Feb 27, 2025 9:10 AM | 8 min read

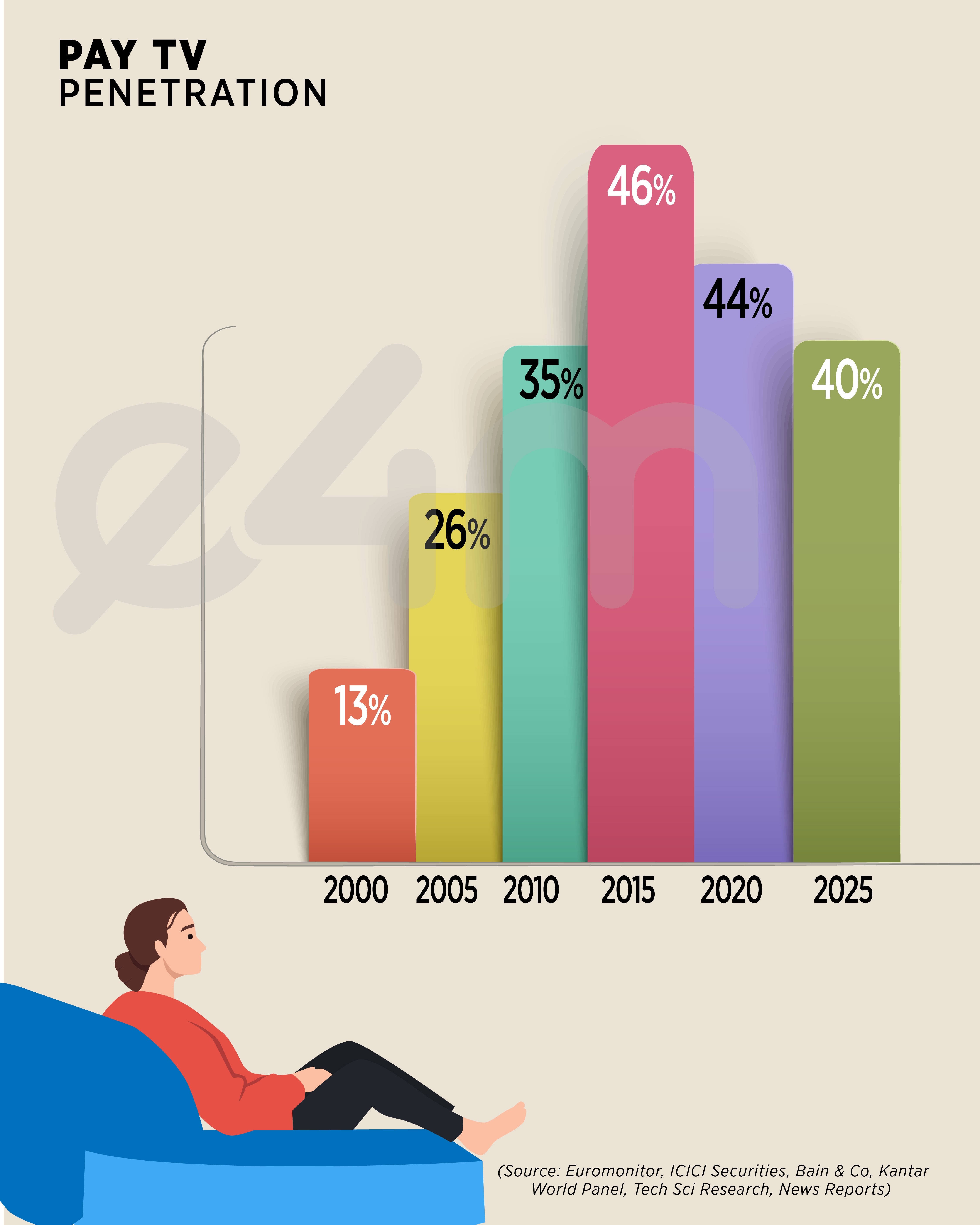

Despite the rise of digital streaming, Pay TV continued to be a significant part of advertiser’s media mix. While its penetration has adjusted from 44% in 2020 to 40% in 2025, Pay TV continues to thrive where it matters most—sports, premium content, and high-engagement programming.

Compared to Free Dish, Pay TV offers a more refined audience with comparatively less wastage, ensuring better targeting for advertisers. Additionally, the availability of fresh and high-quality content drives deeper viewer engagement, making it a key platform for premium entertainment and live events.

Experts said that even though the Pay TV industry's subscriber base has dropped by 33% from 180 million in 2018 to 120 million in 2024, Pay TV remains a key revenue driver.

A JioStar spokesperson told e4m that Pay TV continues to be a dominant force in the media landscape. “We firmly believe its evolution, driven by consumer preferences and technological advancements, has solidified its influence. With nearly 100 million TV-dark homes, there is massive headroom for growth. At the same time, the shift from free to pay presents another opportunity to expand the Pay TV base. As a committed broadcaster in this space, we are strengthening the Pay TV ecosystem by investing in innovative content and ensuring it remains a preferred destination for viewers.”

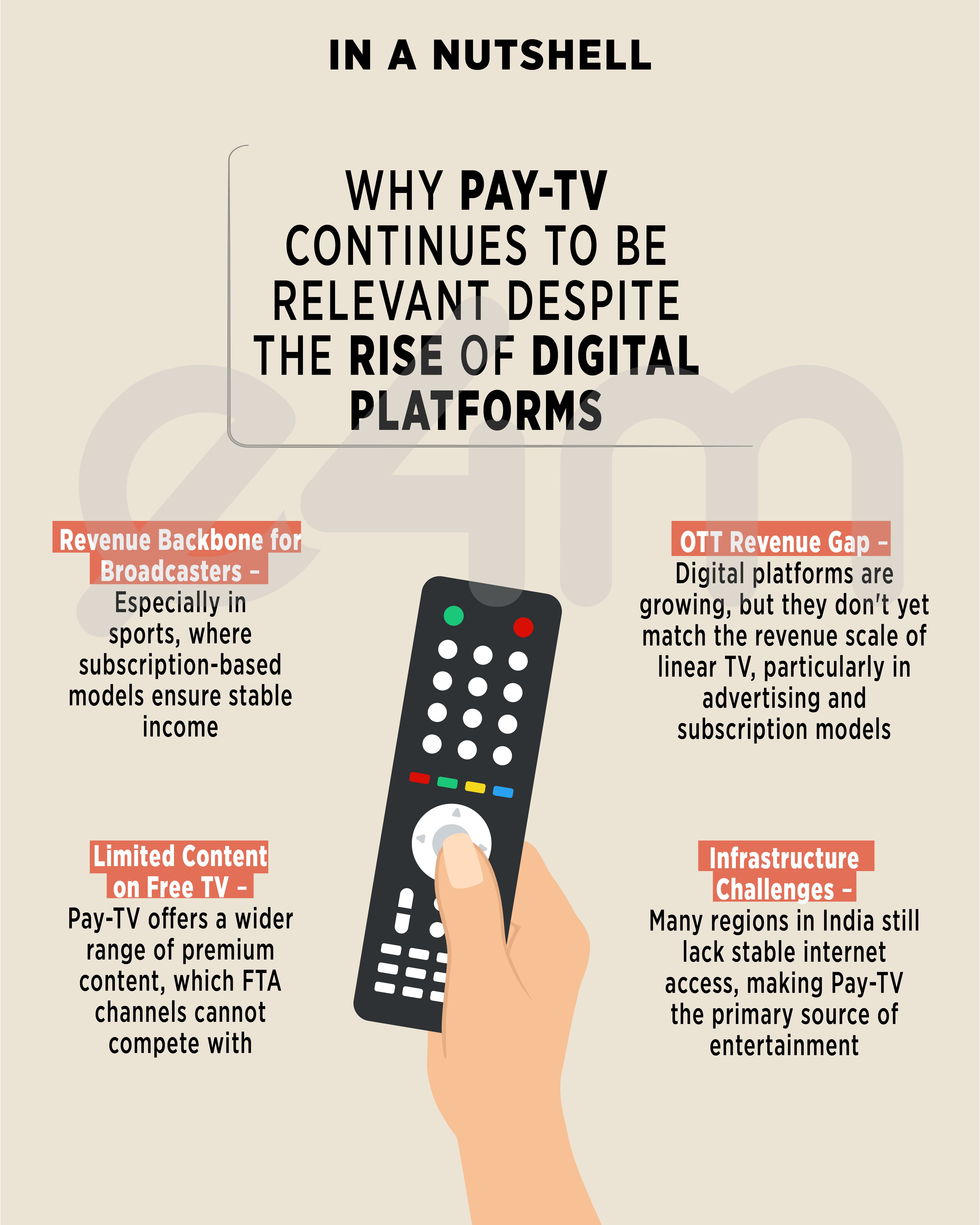

Another industry expert said Pay TV is here to stay, as a significant portion of the population still lacks access to OTT platforms, and the Free-to-Air (FTA) ecosystem has content limitations.

“This ensures that Pay TV remains relevant and cannot be easily replaced,” the expert said, adding that content remains king, and the programming available on Pay TV is not accessible on Free TV, making it a valuable offering for viewers.

According to broadcast expert Rajiv Khattar, despite the digital shift and the abundance of free content, pay TV remains a crucial revenue source for broadcasters, especially in the sports genre.

“Digital platforms have not yet reached a stage where they can fully compensate for the revenue generated by linear broadcasts. Meanwhile, programming costs continue to rise, and advertising revenue is unlikely to see significant growth due to economic constraints. As a result, broadcasters will continue to rely on Pay TV for a steady share of their earnings,” Khattar said.

He, however, added that this year, subscription revenue will dominate, though growth may be limited to just 5%.

Experts also believe that availability of free content on platforms like YouTube, along with many OTT platforms offering free access, is accelerating the digital shift and Free-to-Air (FTA) channels further impact pay TV, as many households opt to save on monthly fees while still accessing staple content such as music, news, movies, and religious programming.

According to a cable industry expert, Pay TV is indeed facing significant challenges with rising channel prices, forced bundling, reduced customer choice, and increasing competition from video OTT platforms. All this has led to a declining subscriber base.

However, he said, if the necessary regulatory reforms are implemented, there is a clear path to revitalize pay TV.

“Industry stakeholders have consistently emphasized the need for rationalizing channel pricing, granting DPOs greater flexibility in bundling, and addressing the widening regulatory disparity between video OTT and traditional broadcasting. The issue of Linear TV on streaming platforms also remains a key concern that requires urgent attention.

“With the right regulatory interventions, Pay TV can continue to be a vital part of India’s broadcasting ecosystem, offering diverse and high-quality content to millions of households while remaining economically viable for all stakeholders,” the expert said, adding that the lack of a level playing field between traditional Pay TV and OTT platforms has further contributed to the sector's distress.

According to data shared by a senior industry leader, TV is a highly penetrated durable but its penetration is relatively low in India compared to other countries. In 2010 the penetration was 47% and in 2020, it reached 62%. Top five countries with highest TV penetration are China (99%), followed by the US (98%), the UK (97%), Malaysia (94%) and Singapore (91%).

Pay TV penetration stood at 13% in 2000, 26% in 2005, 35% in 2010, 46% in 2015, 44% in 2020 and 40% in 2025.

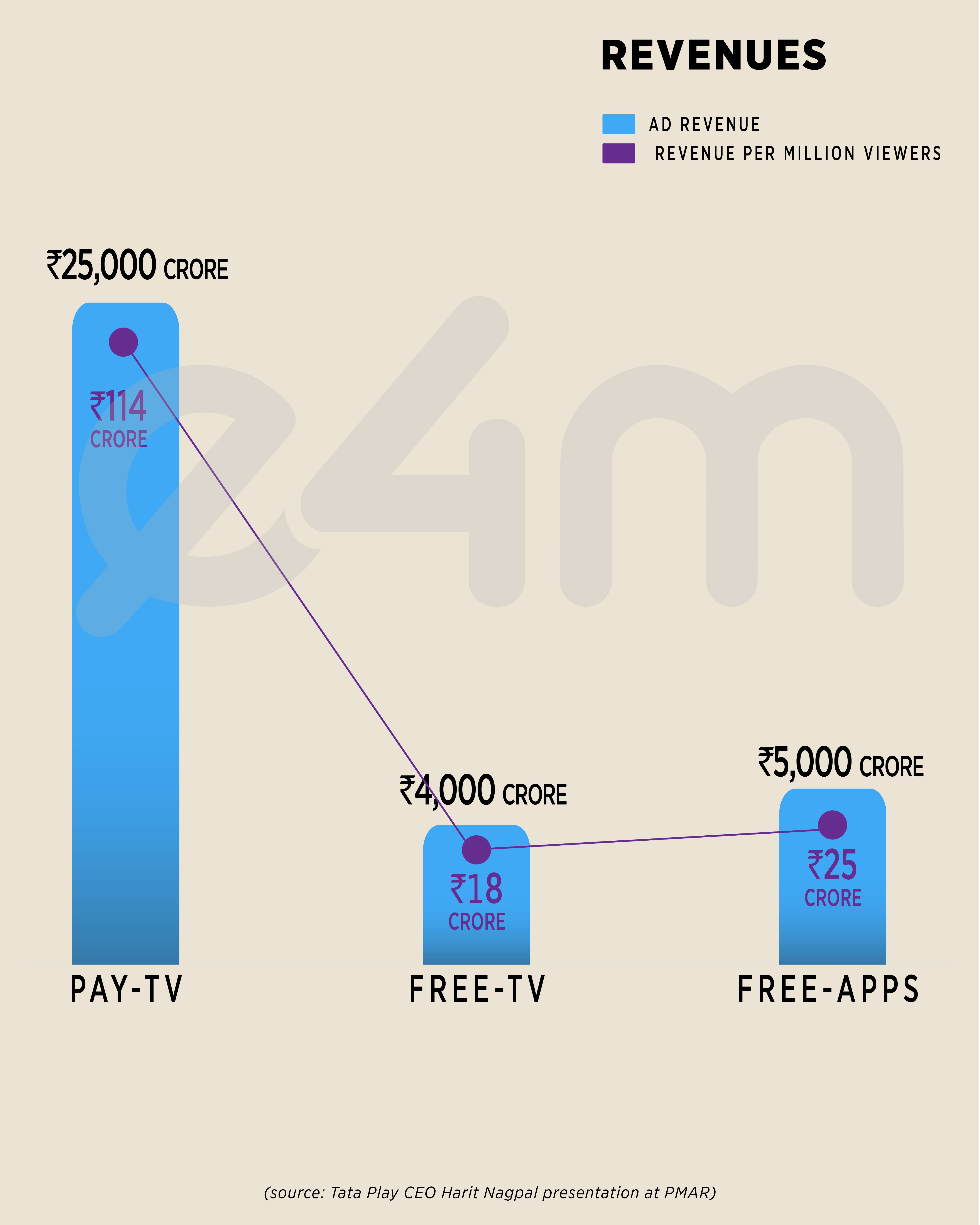

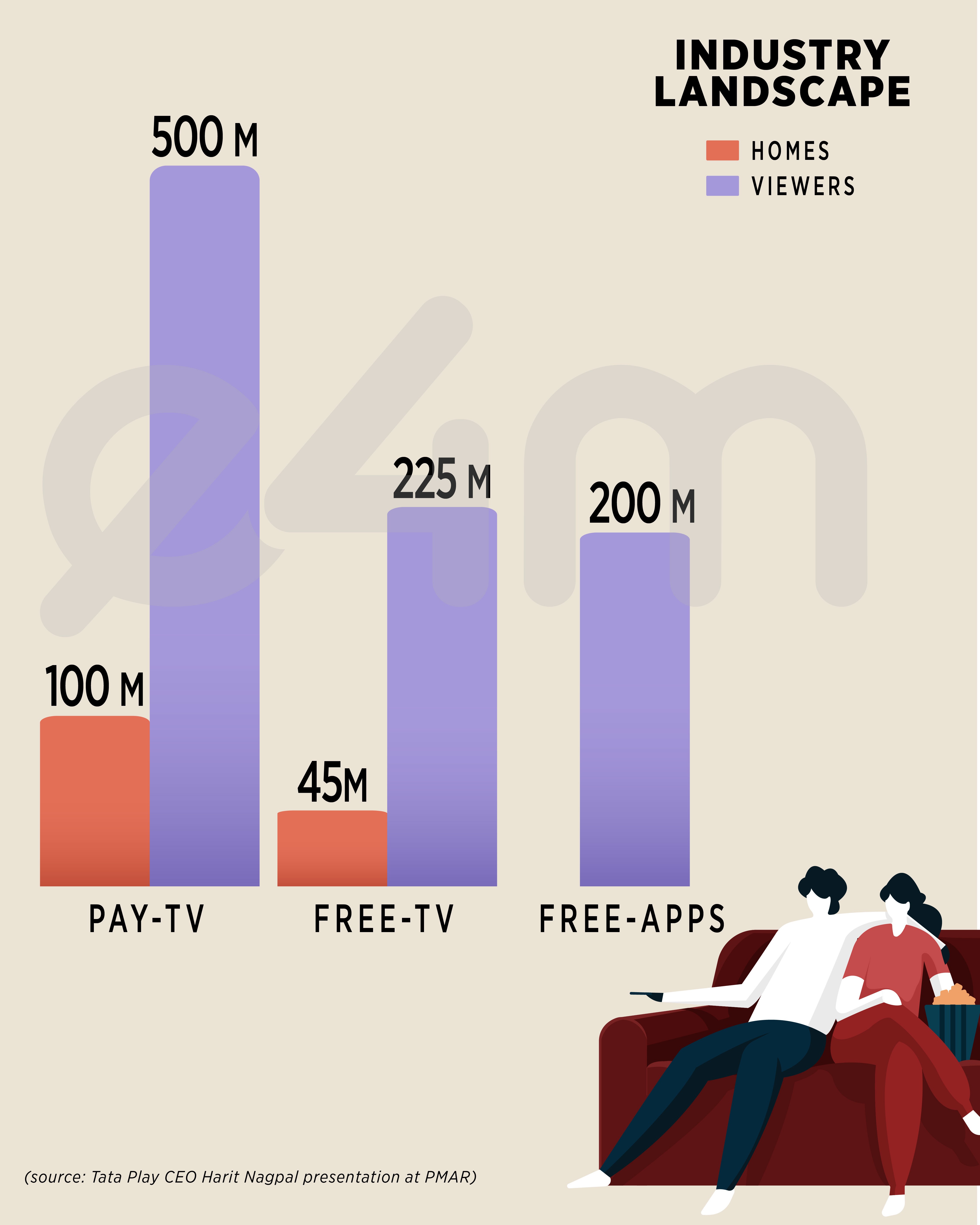

India’s Pay TV segment comprises 100 million homes, reaching 500 million viewers. The sector generates substantial revenue, with ₹32,000 crore coming from subscriptions and ₹25,000 crore from advertising, contributing to a total revenue of ₹114 crore per million.

In contrast, the Free-TV category, which includes DD Free Dish, covers 45 million homes and reaches 225 million viewers. This segment earns ₹4,000 crore in annual advertising revenue, amounting to ₹18 crore per million.

Additionally, the Free Apps segment, catering to 200 million eyeballs, earns around ₹5,000 crore annually through ad revenue, generating ₹25 crore per million.

India's pay DTH sector has witnessed a decline in its active subscriber base, dropping from 62.17 million in June 2024 to 59.91 million by September 2024, according to Telecom Regulatory Authority of India (TRAI).

With lower prices of data, consumers are shifting towards cheaper online streaming options.

According to the recently released Pitch Madison Advertising Report, despite the underwhelming performance in 2024, industry analysts predict a revival for television industry AdEx in 2025.

According to the report, India’s total ad expenditure is expected to reach Rs 1.2 lakh crore, reflecting an 11% year-on-year increase from Rs 1.08 lakh crore. This surge will be primarily fueled by major sporting events, including the IPL, ICC Champions Trophy, Asia Cup, and India’s bilateral cricket series, all of which are expected to drive both TV and digital advertising revenues. Specifically, TV advertising is projected to grow by 6% in 2025, reaching Rs 36,500 crore.

While this growth is still moderate, the industry remains hopeful that large-scale events and a strong push from sports and entertainment content will sustain TV’s relevance amid the rising dominance of digital platforms.

With the evolving media landscape, advertisers are expected to adopt integrated TV and digital strategies, leveraging high-impact events to maximize audience engagement. As the competition between digital and television intensifies, 2025 will be a crucial year for the Indian advertising industry.

According to PMAR, the year 2024 was one of the toughest years for almost all TV Broadcasters in terms of ad revenue, and many industry experts point to a flat TV revenue. We began the year with a forecast of 8% growth, but ended the year with growth of a mere 5% taking TV Adex to a revenue of Rs. 34,450 crores. TV Adex further lost 1% point in terms of share and is now at 32%. The growth rate of 5%, is the slowest in 7 years, baring the Covid year of 2020.

In terms of quarter wise volume, the figures declined as the year progressed. Q1 registered a growth of 6%, but Q2 slowed down to a 1% growth. Q3 registered a -4% growth, whereas Q4 registered a -8% growth. Cumulating to a -1% growth overall.

From the Dentsu e4m Digital Advertising Report 2025, television continues to be a significant player in the Indian advertising market, although its share has seen a decline. In 2024, television accounted for 28% (₹28,062 crore) of India's total advertising spend. However, this represents a drop from 31% in 2023, and it's projected to fall further to 24% by 2025, with continued competition from digital media, especially social media and online video.

It said that traditional media like television and print still hold substantial shares of the advertising pie.

Read more news about Television Media, Digital Media, Advertising India, Marketing News, PR and Corporate Communication News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News