ABC H1 2025: Print circulation up 2.77%, but does growth tell the full story?

The headline uplift masks a knotty, uneven picture on the ground: outside a handful of outliers, most major titles did not post individual gains, and several markets saw single-digit declines

by

by

Published: Oct 7, 2025 8:46 AM | 11 min read

Print’s comeback story gained another chapter in the January–June 2025 period, with ABC-certified daily newspaper circulation inching up 2.77% to 29.74 million average qualifying copies, from 28.94 million in July–December 2024. But the headline uplift masks a knotty, uneven picture on the ground: outside a handful of outliers, most major titles did not post individual gains, and several markets saw single-digit declines.

In plain terms, the topline growth isn’t just from more readers. It also reflects mix effects, new or re-counted editions added to the base in some cases, plus short promotions and timing quirks. The comparison (H2 vs H1) isn’t ideal either. It spans election afterglow, school/college breaks, monsoon disruptions, and pricing/pagination changes.

Once all of that is factored in, the broad-based growth looks much softer. Among the outliers, The Economic Times shows a clear mid-teens rise and Dainik Bhaskar stays largely stable across key Hindi markets while most others are flat or down on a like-for-like basis.

Industry leaders say the uptick is real, though the context around comparability matters.

Also read: GST cut: Print players, agencies see renewed sense of optimism

"These two periods H2 CY2024 and H1 CY2025 are not directly comparable. H1 is typically influenced by the institutional/school holiday calendar which leads to temporary reduction in copies. The more accurate comparison is H1 vs. H1, which reflects a like-for-like basis,” Samudra Bhattacharya, CEO- print business, Hindustan times explained.

“For this period, our circulation has grown by +1%, underscoring continued reader loyalty and the enduring relevance of print. The print environment remains stable, and on a like-to-like basis we have achieved a 1% growth in circulation. This is a clear signal that readers continue to value the credibility, depth, and curated experience that print uniquely provides,” Bhattacharya added.

Pivoting into the numbers- down south too, publishers echo the caution on period-to-period readings while flagging a steady rebuild in revenues.

“Print revenues remained stable in 2024. It is slowly reaching the pre-Covid-19 revenues. From the stage of tremendous resilience, the print industry has been successful in not only anticipating but also coping with and adapting to adversities, and now on to the next stage of growth process, from recovery to thriving,” said M V Shreyams Kumar, MD, Mathrubhumi.

Also read: Mixed quarter for print publishers as ads cushion circulation concerns

Breakdown: Where the gains/drops came from

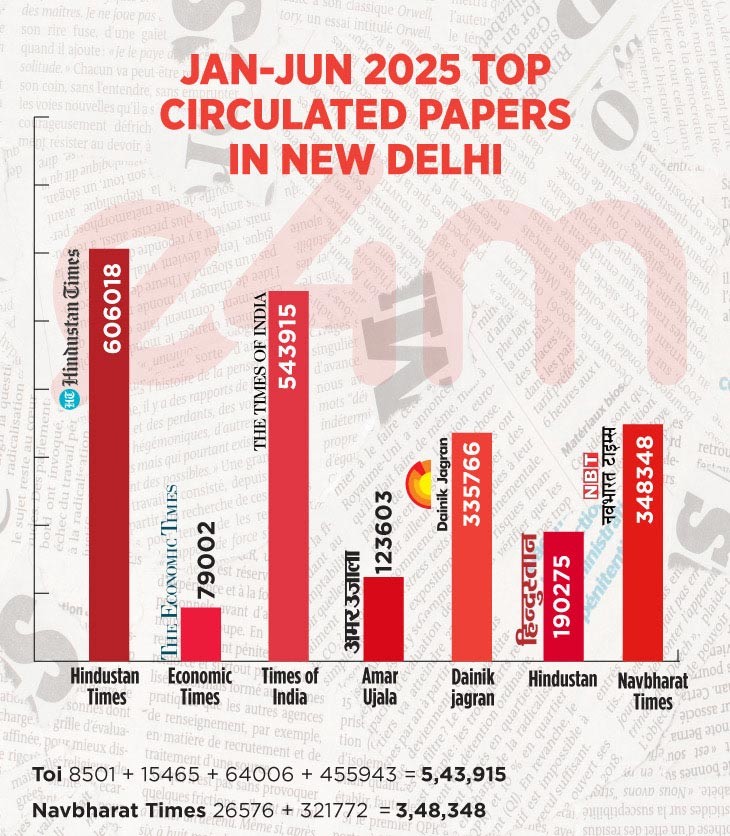

The breakdown across editions reveal a mixed trend. For instance, TOI New Delhi (Sahibabad printing centre) fell to 455,943 (−12.1% vs 518,902), TOI Hyderabad nosedived to 124,554 (−14.1% vs 144,976), TOI Kolkata fell to 153,557 (−7.1% vs 165,321), and TOI Pune fell to 103,789 (−10.8% vs 116,291). Among legacy North titles, The Tribune Chandigarh dropped massively to 87,158 (−23.3% vs 113,677)

Hindi metros were steadier: Navbharat Times (New Delhi) fell to 321,772 (−2.5% vs 329,864) and Punjab Kesari (New Delhi) fell slightly to 350,125 (−0.4% vs 351,488). In the South, Malayala Manorama Kochi dipped to 254,107 (−2.5% vs 260,664). A notable counter-trend was how Hindustan Patna rose to 305,984 (+5.4% vs 290,287), underlining regional divergence and the caution on cross-period.

Similarly, among Dainik Jagran titles, Bhagalpur climbed from 121,477 to 125,838 (+3.6%) and Patna increased from 235,134 to 241,365 (+2.6%). In the South, Sakshi Warangal reported the sharpest improvement, rising from 18,577 to 20,478 (+10.2%), reflecting a more resilient trajectory in these pockets.

In Hindi markets, Amar Ujala Kanpur dropped to 166,819 (−12.1% vs 189,759) and Lucknow touched 162,134 (−9.3% vs 147,081).

On the ground, at least in the south, the circulation picture was shaped as much by local conditions as by demand.

“Traditionally, the first half [ABC Jan–June] has always seen such +/- variations as it is the period of vacations. Further, the construction of NH 66 across Kerala has affected single copy sales in outlets/shops. This year the monsoon set very early during mid-May itself.

Distribution and collections were disrupted in certain districts with continuous red and orange rain alerts. These are purely seasonal and ephemeral local conditions,” said Kumar.

BCCL leads the English pack

Among English dailies, BCCL’s The Economic Times stood out with a near 16% consolidated rise across its audited editions in January–June 2025 versus July–December 2024, per the ABC numbers.

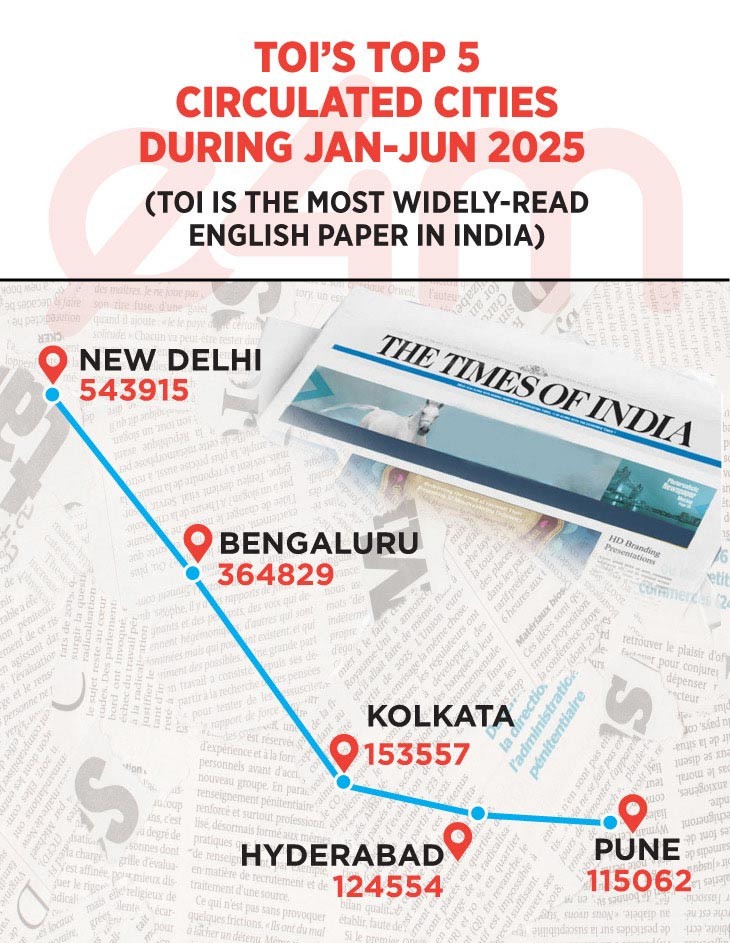

While TOI, which also is a part of BCCL, continues to command the highest English circulation, its audited average qualifying sales slipped by roughly 9.3% over the same comparison window highlighting how ET’s gains came against a softer backdrop for peers.

The momentum for ET was broad-based in the previous period. Kolkata fell to 20,645 (−14.8% vs 24,216), Chennai fell to 22,152 (−6.3% vs 23,635), Bengaluru fell to 43,003 (−3.8% vs 44,697), and Ahmedabad fell to 16,723 (−3.2% vs 17,271), while Kochi held steady at 5,049. Overall, the declines were moderate, reflecting ET’s ability to maintain relatively stable circulation in English print despite city-level variations and seasonal influences.

Bhaskar bucks the swings: Stability across markets

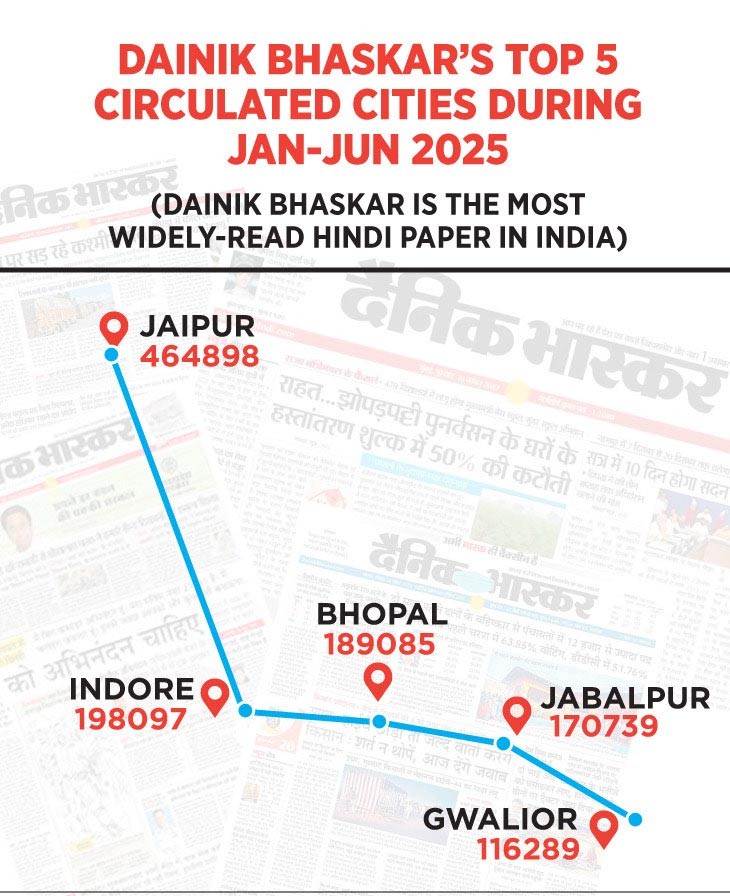

One publisher that distinctly stood out for stability across both periods is Dainik Bhaskar. Across key Hindi markets, several flagship editions sat in a tight ±1–2% band, Jaipur at 464,898 vs 462,332 (+0.6%), Nagpur 90,166 vs 90,194 (flat), Kota 90,318 vs 91,204 (−1.0%), Chandigarh (Sirhind) 86,527 vs 86,484 (flat), Gwalior 116,289 vs 114,347 (+1.7%), and Raipur 191,855 vs 191,241 (+0.3%), signalling steadier print demand even as many peers saw sharper swings.

Reflecting on the approach behind that stability, Rakesh Goswami, Chief Operating Officer, Dainik Bhaskar Group, said the group has “not only sustained its circulation numbers but also achieved growth in key focus markets.”

He pointed to an industry-first phygital reader program “Jeeto 14 Cr.” with daily/fortnightly touchpoints, the summer “Jeeto Sona Chandi” activity driving page-by-page engagement (averaging 1.5 lakh daily participants and 9.7 lakh unique so far), a market-specific on-ground acquisition and win-back engine (including a 1,000+ member door-to-door team, performance marketing and CRM-led retention), and a channel-first “Trade Delight Program” to motivate partners through earnings add-ons, milestone celebrations and automation-led joint field work.

Who’s spending and why it matters

That circulation steadiness has been mirrored on the demand side, with auto, real estate, education, jewellery and retail forming the core of print monetisation this cycle; government advertising (central, state and local) scaled up with multi-page ‘impact’ features around project launches and citizen outreach; BFSI added both statutory notices and brand/public-awareness campaigns; and tactical sales-push bursts at the dealer level lifted auto pages, while local FMCG players leaned in even as some national FMCG majors stayed tepid.

Even so, print’s buyer profile has stayed premium, sustaining high-value categories.

“The silver lining is that print remains the preferred medium for reaching the affluent audiences in India and is being used by premium brands and categories like real estate, automobiles, phones etc., particularly in brand and product launches. Credibility and Trust of Print make it a powerful medium for both news consumption and advertising engagement,” said Shreyams Kumar.

Adding further to this, Manoj Singh, former VP at Madison Media, highlighted that the sentiment towards print remains strong and positive at 65% trust levels from the consumers view, which is reflected in various studies.

“Publishers countering with hybrid models (digital + print) could tilt the balance further towards demand resilience,” he added.

Echoing this sentiment, Deepak Hiremath, Chairman & Managing Director, Vermillion Communication, mentioned, “Reader sentiment is positive, driven by credibility and habit in Tier-2 and 3 markets however digital convenience has drawn away casual urban readers with softening in subscriptions specially newsstand copies.”

The circulation trajectory reflects both genuine demand shifts as per Hiremath, especially urban fatigue, and technical factors such as ABC’s stricter audit coverage and rationalized reporting. But, it is not a collapse of print readership.

What the data and decision-makers say

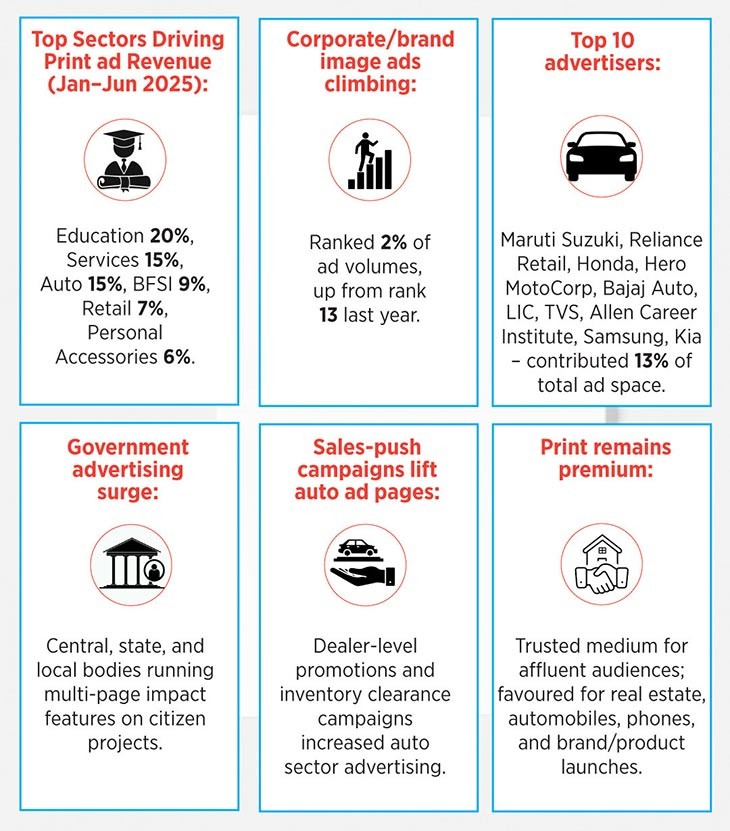

As per TAM AdEx print ad-volumes for January–June 2025, education led the sectoral mix at 20% contribution to overall ad volumes, with services (15%) and auto (15%) close behind; banking/finance/investment contributed 9%, retail 7%, personal accessories 6%, food & beverages 4%, while durables and personal healthcare were at 3% each. Corporate/brand image advertising accounted for 2%, notably climbing from rank 13 a year ago, while others made up the remaining 15%.

The top 10 advertisers contributed 13% of total print ad space out of 87K+ active advertisers. Maruti Suzuki India held the top spot, Reliance Retail took the second spot, while Honda Motorcycle & Scooter and Hero MotoCorp, Bajaj Auto, LIC, TVS Motor, Allen Career Institute, Samsung India Electronics and Kia Motors Corporation followed next.

Advertisers say circulation is a starting point, not the finish line. Dabur India's VP in Marketing, Rajiv Dubey said, “Circulation is a gating input for us as FMCG advertisers, but never the only criterion. While the latest ABC numbers show strong variations, what really matters is how these readers align with our core markets and product categories. Hindi and regional dailies remain critical for mass reach in heartland India, while English titles help us connect with urban, premium consumers. Ultimately, circulation trends guide our choices, but cost per reach, geography and consumer relevance determine where the advertising rupee goes."

Publishers echo that lens from the supply side, pointing to government and BFSI-led demand shaping the current print ad mix.

“We are also seeing a trend among governments, be it central, state or local bodies, to promote what they are doing for the benefit of the citizens. Hence, we are witnessing vigorous advertising from governments around ground-breaking and launch of various projects,” said Sumit Modi, Chief Operating Officer, Madhya Pradesh, Rajasthan & Chhattisgarh, Dainik Bhaskar Group.

“Moreover, there is an emerging trend of impact features by various governments, sometimes running into multiple pages, on what and how they are transforming the lives of their citizens. This is contributing immensely to our revenue kitty. BFSI, apart from their obligatory statutory requirements, like notices, are also publishing their branding and public awareness campaign, which is adding to our revenue. Sales Push Tactical Advertising with various schemes for inventory clearance at the dealers-end did push auto companies to take up advertising in a big way in this year,” Modi added.

According to Modi, while the national level FMCG players have been tepid in their print advertising, many local FMCG players continued, and even increased their ad spends in the year, to gain share from their bigger counterparts.

Reading the city lines carefully

In several cases, titles are clustered under a metro family rather than a single edition name. For instance, The Times of India – New Delhi spans multiple satellite print centres: Bareilly (8,501), Dehradun (15,465), Manesar (64,006) and Shahibabad (455,943) in H1’25. That makes “Delhi” a broader footprint and complicates like-for-like city comparisons. It also begs a question for buyers and analysts alike: Should such clusters be evaluated as metro footprints instead of standalone city editions? “The over-emphasis on the number of copies sold and paid for does not always provide a comprehensive understanding of the actual audiences that see an advertisement. Paid copy is the parameter for ABC audits. Pass-along readership and online readership are not fully captured. This is not an indication of the overall health and reach of a publication,” Shreyams Kumar.

The Mumbai puzzle

Notably, Mumbai daily editions are missing or not certified for several blue-chip brands this cycle. The Economic Times has no Mumbai (daily) line item in the preliminary list (though its weekly ET Wealth shows Mumbai 40,467), and The Hindu, Mumbai appears as “Not Submitted.” Even TOI’s daily roster in this list shows multiple cities but no Mumbai line, highlighting how non-submission can skew metro-to-metro comparisons in H1’25.

New/changed editions can lift the totals

Overall tallies can also move when new editions enter, old ones pause, or membership status changes between periods. Lokmat is a useful case. Their brand-level growth appears close to 80% in H1 CY2025 largely because editions that weren’t counted in H2 CY2024 are now included. For instance, Lokmat Nagpur is certified at 202,677 (vs 207,877 earlier), while several Sambhaji Nagar–area editions that were previously absent/“not a member” are now in the frame, so the step-up is base-driven and mechanically pushes the overall circulation total, independent of underlying demand.

Taken together, ABC’s January–June 2025 print uptick is real, but best read through a like-for-like lens and with an eye on audit coverage and city-edition submissions.

The stand-outs and the steadies show there’s durable demand where credibility and local depth are strongest, while TAM AdEx signals that premium, launch-heavy categories continue to value print’s high-attention environment. Equally, metro gaps and base effects from newly counted editions inflate aggregates and complicate comparisons.

The more telling test now is H2, typically a stronger, festival-led half when advertiser momentum, cover-price discipline, and bundled print-plus propositions will determine whether this bounce consolidates into sustained growth.

Read more news about Print Media, TV Media, Advertising India, Digital Media, Marketing

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News