Market cap vs revenue: How investors are repricing India’s media stocks

A tighter gap emerges as TV’s growth cools and print’s cash generation steadies; see the latest company numbers and what could trigger a re-rating

by

by

Published: Sep 22, 2025 9:26 AM | 5 min read

India’s listed media stocks are no longer moving in lockstep. As of market close on Sept 18, 2025 (IST), within the media universe, the market continues to price TV broadcasters richer than print-led peers, but the gap is narrowing as TV faces slower ad momentum and a tougher connected-TV (CTV) battlefield, while print benefits from steadier cash generation.

TV long sat at the top of India’s ad pie, but 2024 marked a turn. As per the latest Pitch Madison Report, TV grew by only about 5% and its share slipped to around 32%, while the number of TV advertisers fell from about 11,100 in 2023 to about 8,700 in 2024. Digital has firmly taken the number one slot with around 42% share, while print, helped by steadier cash generation, held near 19% with roughly 5% growth. Together, these shifts explain why markets have started narrowing the broadcaster–print valuation gap.

And that shift is reflected in valuations. Broadcaster multiples that historically sat above print have tightened this year. Markets are discounting slower TV ad momentum and a more competitive CTV landscape while crediting the steadier cash generation of print, leaving a premium in place but noticeably slimmer than before.

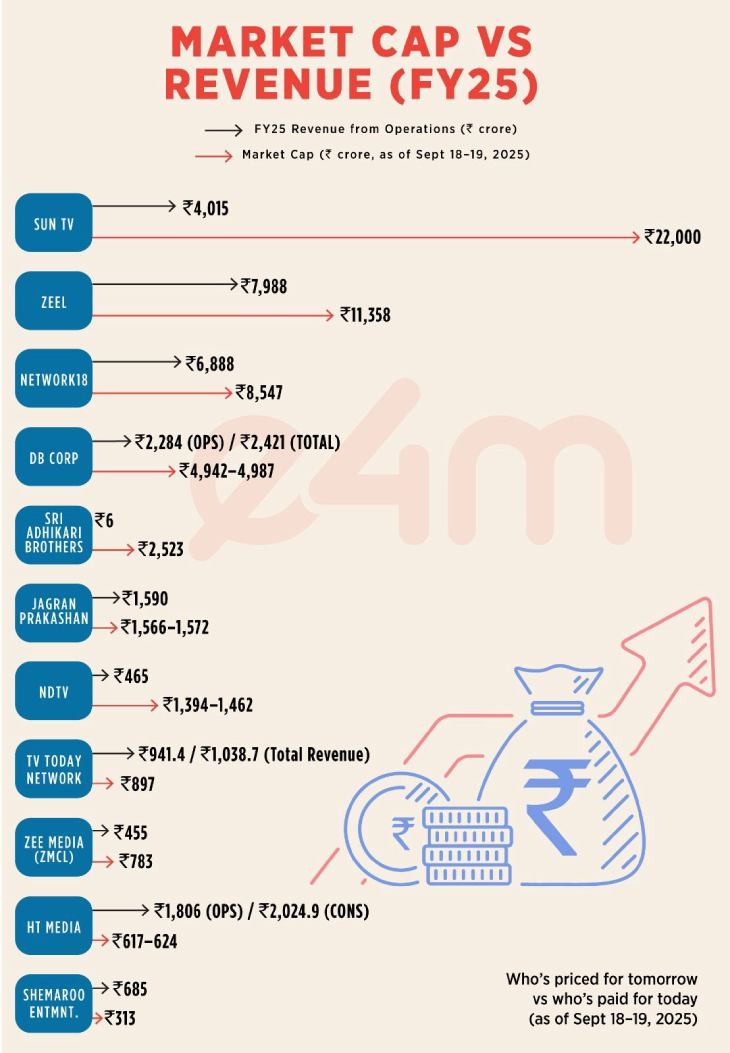

For context, here’s how the big listed names stack up right now- Sun TV Network (market capitalization approximately Rs 22,000 crore as of Sept 19, 2025; FY25 revenue from operations Rs 4,015 crore); Zee Entertainment (ZEEL) (market capitalization approximately Rs 11,358 crore; full-year revenue approximately Rs 7,988 crore); Zee Media (ZMCL) (market capitalization approximately Rs 783 crore; FY25 revenue from operations Rs 455 crore); Network18 (market capitalization approximately Rs 8,547 crore; FY25 consolidated revenue about Rs 6,888 crore); NDTV (market capitalization approximately Rs 1,394–1,462 crore; FY25 revenue from operations Rs 465 crore); HT Media (market capitalization approximately Rs 617–624 crore; FY25 consolidated revenue Rs 2,024.9 crore, revenue from operations Rs 1,806 crore); Jagran Prakashan (Dainik Jagran) (market capitalization approximately Rs 1,566–1,572 crore; FY25 total operating revenue Rs 1,590 crore); DB Corp (Dainik Bhaskar) (market capitalization approximately Rs 4,942–4,987 crore; FY25 revenue from operations Rs 2,284 crore; total revenue Rs 2,421 crore). TV Today Network (market capitalization approximately Rs 897 crore as of Sept 19, 2025; FY25 revenue from operations Rs 941.4 crore; total revenue Rs 1,038.7 crore).

Also read:

Sun TV Network sees decline in profits

'ZEEL designing omni-channel business model for future growth'

Network18 posts nearly Rs 149 crore profit in Q1 FY26

Against that backdrop, Karan Taurani, Executive Vice President at Elara Capital, explained how the historical premium for TV over print rested on two planks, scale in the advertising pie and the potential to extend that scale into digital via OTT and CTV while print’s digital monetisation remained small.

“But if you look at the last six months, broadcaster valuations have largely come on par or even at a discount to print in some cases,” he said, pointing to TV’s share loss in the ad pie, the inability to fully offset that via digital, and selective margin pressure from higher digital investments.

In his base case, he does not see TV reclaiming a large premium over print unless digital truly scales.

“You don’t get premium multiples until digital is 25–30% of revenue with 20–25% steady-state margins. Otherwise, the sector settles around similar bands. Print steady at roughly 10–12x forward P/E, and TV moving up from about 8–10x only if digital execution lands,” he added.

On the ground, CTV is both the opportunity and the constraint.

Taurani argued that linear TV cannot easily reinvent content for younger cohorts, measurement remains patchy, and competitive intensity on connected screens is far higher than in linear.

“On CTV, broadcaster apps are not the default; you’re up against YouTube, Netflix, Amazon and a long tail of OTT. To scale, broadcasters must differentiate on content, UX and exclusivity,” he said, adding that micro-dramas and YouTube’s massive base complicate share gains for broadcaster OTTs.

A similar read comes from the investor side.

Commenting on CTV economics, Kabir Kochhar, Founder and Managing Partner at Audacity Venture Capital said, “The value in CTV sits with OEM-controlled surfaces and O&O/FAST, so that’s where I model the mix is shifting. I’m only giving a modest CPM uplift for now because supply is heavy and YouTube still dominates. ACR (Automatic Content Recognition) is the unlock for targeting/measurement, but IDs and cross-device attribution are messy, so I assume OEMs partner with specialists. In India, search monetization is small but growing,” he said.

“I shall re-rate when platform/O&O/FAST show up as as real revenue, ACR is scaled with clean de-duped reach, unified IDs lift mid-funnel, shoppable + TV search become material, and we see early wins on gaming ACR,” Kochhar added.

Simply put, according to Kochhar, the real CTV money will flow to device home screens (run by TV OEMs) and to owned-and-operated/FAST channels, not automatically to every broadcaster app.

So, expecting big CPM jumps is not yet on the cards because ad supply is abundant and YouTube still dominates the segment. Better targeting and trustworthy reach numbers will only come when ACR is widely scaled and IDs work cleanly across devices (likely via specialist partners).

Ultimately, any sector re-rating will hinge on tangible delivery. CTV revenues that show up in results, ACR-based measurement that advertisers trust, and durable digital margins.

Until those pieces align, the market cap versus revenue snapshot remains the clearest barometer of how investors weigh broadcasters’ growth optionality against print’s cash-flow certainty and why the valuation gap has narrowed but not disappeared.

Read more news about Television Media, Digital Media, Advertising India, Marketing News, PR and Corporate Communication News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News