Is quick commerce quietly altering the urban grocery marketing playbook?

Experts say supermarkets are gradually losing marketing clout as 15–50% trade budgets shift to quick commerce

by

by

Published: Feb 23, 2026 9:13 AM | 7 min read

Quick commerce is no longer a novelty in India’s retail story. The clearest proof lies in how the year has begun. According to Redseer, India’s quick commerce Gross Merchandise Value (GMV) reached an estimated ₹11,000 crore in January, nearly doubling year-on-year. Order volumes climbed about 95% YoY to 7.8 million online purchase orders (OPDs). But the deeper structural signal lies beyond this. Quick commerce already accounts for roughly 15% of India’s overall e-commerce market, and in the top eight metros, its share is closer to 30% of total e-commerce spending, according to Nikhil Dalal, Associate Partner, Redseer. Within online grocery specifically, more than 70% of sales are now happening through quick commerce formats, reflecting how rapidly scheduled delivery is being displaced.

India’s grocery ecosystem broadly operates across three formats: kirana stores, large hypermarkets, and mid-sized supermarkets, alongside online scheduled delivery models. According to industry experts, the sharpest shift toward quick commerce is currently being witnessed in mid-sized supermarkets and scheduled e-commerce grocery delivery formats.

The rise of quick commerce is not merely about faster delivery; it reflects a deeper recalibration in how consumers discover, evaluate and purchase everyday products. Shopping patterns are shifting from planned store visits to on-demand, need-based ordering. Increasingly, top-up and impulse purchases are moving away from traditional store formats and into app-based ecosystems where convenience, speed and personalisation drive behaviour.

For decades, supermarkets offered brands physical dominance. Shelf positioning, gondola displays, end-caps and promoter-led activations functioned as powerful discovery engines. The aisle walk was not just a path through a store — it was a curated marketing environment where visibility translated into consideration and, often, conversion. Today, that aisle walk is steadily being replaced by a search bar and algorithm-led recommendations on quick commerce platforms such as Blinkit, Zepto and Swiggy Instamart.

In this new paradigm, experts point out that brands, particularly those in impulse-driven and high-frequency categories, are beginning to reallocate a meaningful share of their trade marketing budgets toward retail media within these platforms.

Shradha Agarwal, Co-founder and CEO of Grapes, told e4m that the shift is already visible in allocation patterns. “Brands are reallocating because they’re seeing substantial traction here. Earlier, online contributed 5–6% for many of our clients. Now that number is moving to 15–20%. Retail still holds close to 80%, but the caution has clearly moved online,” she explained.

Experts have said that this is not merely a shift from offline retail to e-commerce, brands are also redirecting brand-building budgets into digital performance environments. “We’ve seen a jump of almost 30% toward performance marketing and online brand marketing. Clients are increasingly asking whether the money spent on in-store promotions can instead be invested online, where ROAS can be tracked for every penny,” added Agarwal.

Chetan Asher, Founder & CEO, Tonic Worldwide, describes the shift as “a quiet drain rather than a clean pivot.” Brands, he said, are not publicly announcing pullbacks from modern trade. “Budgets in modern trade aren’t being slashed overnight. They’re simply stagnating, while incremental funds are being directed toward quick commerce retail media.”

Physical shelf presence still holds value, but its role has evolved. “If you’re depending on the shelf to do the discovery work the way it used to, that era is largely over in urban markets,” Asher added. The promoter budget that once covered teams across 40 stores in Mumbai, he said, is increasingly being converted into performance allocations on quick commerce platforms “where every rupee is tracked, every impression is logged and every conversion is attributed. That accountability is addictive.”

Adding to this, Rohit sharma, Manager ecommerce, WPP Media, said, “Brands are gradually shifting shopper marketing budgets toward retail media on quick commerce platforms like Blinkit, Swiggy Instamart and Zepto because these platforms offer shelf visibility similar to physical stores, but with sharper targeting and clearer sales measurement. However, this does not mean supermarket activations are stopping. Instead, brands are moving toward a more integrated approach, reallocating a portion of in-store visibility budgets to digital shelf formats such as search, sponsored products and in-app banners, while physical stores themselves are becoming more data-driven.”

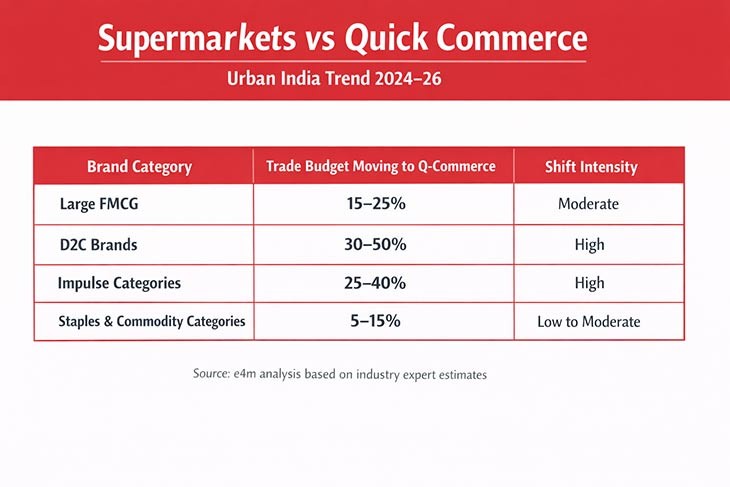

Backing this shift with category-level movement, Mandar Lande, Co-Founder and CEO, WAAYU App, who works closely with several restaurants and consumer brands, noted that in urban India, large FMCG companies are reallocating roughly 15–25% of their trade marketing budgets toward quick commerce retail media. For high-growth D2C brands, the shift is between 30–50%. Impulse-driven categories such as snacks, beverages and ice creams are seeing reallocations in the 25–40% range, while staples and commodity categories remain more measured at 5–15%.

Lande clarified that this is largely incremental reallocation rather than outright cannibalisation of offline trade. “Budgets are being diverted more from mid-sized supermarkets than from large hypermarkets,” he said, suggesting that not all physical retail formats are equally vulnerable.

Dalal’s channel-level analysis reinforces this view. Nearly 90% of India’s grocery retail still flows through kirana stores, and Redseer expects that share to remain above 80–85% over the next three to five years. Large hypermarkets, too, are likely to retain their core user base due to bulk-buy behaviour and price-led positioning.

“The more visible shift is happening from mid-sized supermarkets and scheduled e-commerce delivery,” Dalal explained. Quick commerce, by offering comparable pricing with far superior immediacy, is increasingly taking incremental share from both.

Also Read:What will it take for quick commerce to win Bharat?

Inside FMCG’s digital reset: What’s taking India’s biggest advertisers online

Will retail media reshape media planning, measurement & commerce in 2026?

Industry experts point out that the reasons for the shift are structural. Quick commerce platforms offer measurable ROI, search-led intent capture, geo-targeting by PIN code, sponsored listing control and rapid experimentation cycles, capabilities that traditional supermarkets cannot easily replicate. “Retail media has effectively become the new end-cap,” Lande added.

The most fundamental change is not just where products are being sold, but how visibility itself is being bought. Instead of negotiating for eye-level shelf space or gondola ends, brands are now increasingly bidding for digital prominence — search rankings, sponsored tiles and category banners within quick commerce apps. As Mandar Lande explains, what was once a ₹15,000-a-month promoter deployment in a single outlet can now be redirected toward sponsored search placements across multiple PIN codes, delivering lakhs of impressions along with measurable conversion data.

Industry observers say that within the quick commerce ecosystem, the mechanics of influence are being redefined in ways that closely mirror traditional trade marketing, but in digital form. The top search result effectively functions as eye-level shelving. Sponsored tiles replicate the visibility of gondola ends. Push notifications play a role similar to promoter-led nudges, while flash deal banners operate much like in-store discount displays. The difference, experts note, lies in measurability and targeting precision.

This is where mid-sized supermarkets face mounting pressure. Unlike digital platforms, many regional and neighbourhood chains lack advanced shopper data systems, attribution tools, dynamic pricing dashboards and personalisation capabilities. As one industry executive points out, “their marketing leverage is shrinking faster than their revenue decline.”

Large hypermarkets such as DMart continue to benefit from bulk-buy economics, price-led positioning and destination shopping behaviour, which insulate them to some extent. Kirana stores, anchored in relationships and proximity, also operate on a different logic that is less dependent on formal trade marketing budgets.

The sharper squeeze, industry experts suggest, is being felt in the mid-sized supermarket segment and in scheduled online grocery delivery — the two formats witnessing the most visible migration toward quick commerce. Over the next three to five years, experts say, nearly 80% of scheduled online grocery is expected to shift toward quick commerce formats, particularly across metros and Tier I cities, where density economics favour faster fulfilment models.

Read more news about Marketing News, Advertising News, PR and Corporate Communication News, Digital News, People Movement News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook, YouTube & Google News