FY26 Outlook: Broadcaster OTT revenues to grow 10–15%, but economics still challenging

While digital consumption continues to expand, the revenue trajectory highlights a market that is maturing but still struggling to balance scale with sustainable economics

by

by

Published: Dec 25, 2025 9:04 AM | 4 min read

With over half of the current fiscal already behind it, India’s broadcast industry is beginning to reveal a clearer revenue trajectory, characterised by steady yet restrained growth and persistent profitability challenges for broadcaster-owned OTT platforms.

Industry projections suggest that OTT revenues for Indian broadcasters in FY26 are likely to grow by 10–15% year-on-year, signaling a market that has moved beyond hyper-growth but continues to expand, driven by evolving viewer behaviour and sustained advertiser interest.

While digital consumption continues to expand, the revenue trajectory highlights a market that is maturing but still struggling to balance scale with sustainable economics.

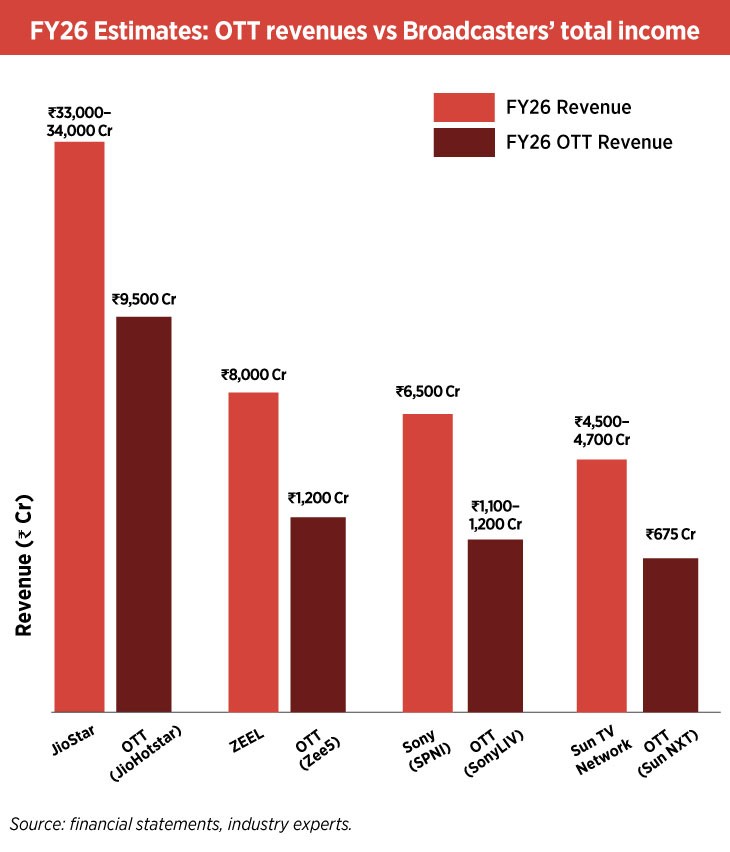

Among broadcasters, JioStar is projected to remain the largest digital and television player by scale. Its total annual revenue for FY26 is estimated at around ₹33,000–34,000 crore, having already generated approximately ₹18,000 crore in the first half of the fiscal. Within this, JioHotstar’s standalone OTT revenue is estimated at around ₹9,500 crore for FY26, which is nearly 30 % of the total revenue.

As per estimates from reliable industry sources, JioHotstar’s revenue from subscription stands at around Rs 4,000 crore, from IPL and ad revenue together another Rs 4,000 crore and around Rs 1500 crore from entertainment sector.

Despite this scale advantage, the platform remains far from profitability, largely due to the outsized cost of sports rights.

According to an industry expert, the annual outflow for IPL alone, across television and digital, is estimated at nearly ₹10,000 crore, while total inflows from the property are believed to be closer to ₹5,000 crore. This structural mismatch has intensified internal and industry-wide questioning around the long-term viability of premium sports as a profit driver for both TV and OTT.

ZEEL is expected to report total revenues of around ₹8,000 crore in FY26, with Zee5 contributing approximately ₹1,200 crore. Zee5’s quarterly performance, including a reported ₹300 crore in one quarter of the current fiscal, points to stable but incremental growth rather than a breakout.

Sony Pictures Networks India (SPNI), meanwhile, is projected to maintain total company revenues of about ₹6,500 crore in FY26, with SonyLIV contributing roughly ₹1,100–1,200 crore.

Unlike several peers, Sony’s broadcast and digital businesses together continue to remain profit-making, though OTT alone is not yet a dominant earnings engine, said an industry observer.

For Sun TV Network, total revenue in H1 FY26 stood at ₹2,737 crore, compared with ₹2,480 crore in the corresponding period of FY25. The company reported full-year revenues of ₹4,543 crore in FY25. According to industry sources, Sun NXT, the group’s digital platform, is estimated to contribute around 15% of total revenues, translating to roughly ₹675 crore on an annualised basis. Industry experts attribute the platform’s relatively modest revenue contribution to a lack of fresh, OTT-first content, its heavy reliance on television catch-up programming, the absence of a dedicated OTT sales strategy, and limited acquisition of non-Tamil film content for the platform.

The FY26 projections underline a broader industry pattern: OTT revenues are rising, but not fast enough to offset the cost structures built over the past few years.

Media buyers and broadcasters broadly agree that while digital advertising is still growing, TV ad sales and distribution revenues have declined by nearly 20%, and digital OTT revenues are either flat or growing slowly. As a result, most broadcaster-owned OTT platforms continue to operate at a loss, with sports content further accelerating cash burn rather than improving margins.

Looking back at FY24–25 provides important context to these expectations.

According to industry estimates, India’s OTT market touched approximately ₹37,940 crore in revenues in FY25, combining advertising and subscription income. A significant portion of this was driven by ad-supported platforms, with YouTube alone accounting for nearly 38% of the total OTT revenue pool, highlighting the dominance of free, ad-led consumption in India. In contrast, subscription-heavy broadcaster platforms accounted for a much smaller share of total digital revenues.

Industry executives increasingly acknowledge that adding sports content deepens losses unless supported by far stronger monetisation levers.

SonyLIV and Zee5 reported FY25 revenues broadly in the ₹1,000–1,200 crore range, reflecting consistency but also limited upside. Despite aggressive investments in originals, sports and regional programming, audience behaviour on OTT platforms remains uneven, with spikes around marquee content but limited stickiness across the year. This inconsistency has made it difficult for platforms to extract long-term value from high upfront investments.

Overall, while OTT revenues in India are undeniably growing, the pace of growth and the structure of monetisation continue to challenge broadcasters.

JioStar remains the best placed strategically due to its unmatched scale and distribution muscle, but it is still far from profitability. Sony stands out as relatively stable due to a diversified and profit-making core business, while Zee continues to push for digital growth amid broader financial restructuring.

As FY26 unfolds, the central question for India’s OTT players is no longer about expansion or reach, but about whether disciplined content strategies and smarter monetisation can finally turn revenue growth into sustainable profits.

Read more news about Television Media, Digital Media, Advertising India, Marketing News, PR and Corporate Communication News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News