6 million subscribers lost in a year: Time for DTH to press the reinvention button?

Next few years are likely to determine whether traditional satellite television can remain relevant as part of India’s media ecosystem, or whether it will be steadily sidelined by digital platforms

by

by

Published: Sep 10, 2025 8:50 AM | 6 min read

The Direct-to-Home (DTH) sector in India has been under growing strain as the shift of viewers to digital and on-demand content has triggered a sharp contraction in its subscriber base over the past year.

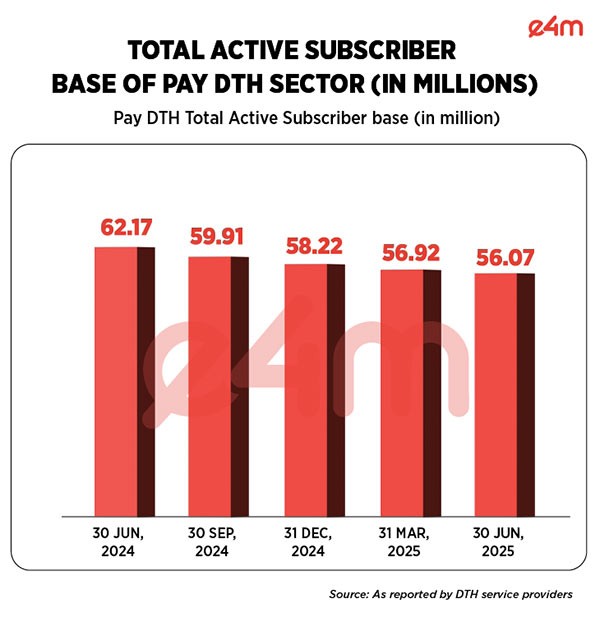

According to TRAI, the number of active DTH subscribers of the only four DTH players fell from 62.17 million on June 30, 2024, to 56.07 million by June 30, 2025, representing a loss of more than six million users in just 12 months.

The steady erosion reflects not only the rise of over-the-top (OTT) and connected TV platforms but also the increasing competition from free-to-air options like DD Free Dish, which continue to attract cost-sensitive households.

The fall in subscribers was not sudden but consistent throughout the year, highlighting the depth of the structural shift underway in Indian television consumption. At the end of June 2024, the active subscriber base stood at 62.17 million. By September 2024, it had dropped to 59.91 million. The downward trend continued through December 2024, when the base shrank further to 58.22 million. By March 2025, it had fallen to 56.92 million, before reaching 56.07 million at the close of the June 2025 quarter, the lowest point in the 12-month period.

This pattern underscores a gradual but persistent migration of audiences away from satellite television toward broadband-enabled, on-demand viewing, particularly in urban markets where internet penetration has deepened.

Despite this contraction, the relative positioning of four DTH operators – Tata Play, Airtel Digital TV, Dish TV and Sun Direct - has remained largely unchanged, suggesting that the challenge is industry-wide rather than confined to any single player.

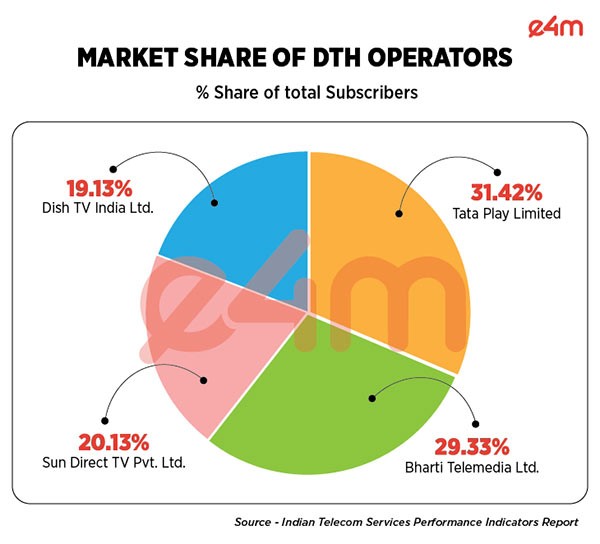

As of June 30, 2025, Tata Play retained leadership with a 31.42 percent share of the total subscriber base. Bharti Telemedia Ltd. (Airtel Digital TV) followed closely with 29.33 percent, while Sun Direct TV Pvt. Ltd. held 20.13 percent and Dish TV India Ltd. accounted for 19.13 percent.

Market share figures for the quarter ending March 31, 2025, tell a similar story, with Tata Play steady at 31.42 percent, Airtel Digital TV at 30.20 percent, Sun Direct at 19.32 percent, and Dish TV at 19.06 percent. These numbers indicate that while the overall pie has shrunk, the competitive balance among players has not shifted dramatically, though the race between Tata Play and Airtel Digital TV remains especially close.

The financial results of operators during this period mirror the subscriber decline. Dish TV, one of the oldest players in the sector, reported a sharp revenue fall in the first quarter of fiscal 2026. Its total income declined 27.7 percent to Rs 329.4 crore from Rs 455.3 crore in the same quarter last year. Subscription revenue fell 10.8 percent to Rs 273 crore from Rs 306.2 crore, while advertising income dropped by more than half to Rs 4.4 crore from Rs 9.7 crore. Losses deepened sharply, widening from Rs 1.6 crore in Q1 FY25 to Rs 94.5 crore in Q1 FY26. These figures underline the dual challenge of falling subscriber numbers and declining ad revenues, both of which weigh heavily on profitability.

Airtel Digital TV, by contrast, reported a more modest dip. In the first quarter of FY26, the company posted revenue of Rs 763 crore, down 1.8 percent year-on-year, with a customer base of 15.7 million. For the entire fiscal year 2024–25, its revenue stood at Rs 3,060 crore, nearly flat compared to the previous fiscal. Bharti Airtel Vice Chairman and Managing Director Gopal Vittal noted that despite headwinds, Airtel Digital TV had achieved a record high market share. He emphasized that the company is implementing structural changes by eliminating subsidies in its DTH business, a move expected to strengthen cash flows even as competition intensifies.

Tata Play, the sector leader, has not been immune to pressure. In FY24-25, the company’s loss widened to Rs 529.43 crore from Rs 354 crore in FY23-24. Revenue declined 5.46 percent to Rs 4,082 crore from Rs 4,305 crore in the previous fiscal. The company’s subscriber base shrank sharply to 18 million in FY25, down from a peak of 23 million. Analysts at Crisil Ratings observed that Tata Play is unlikely to see revenue growth in FY26 as it continues to face headwinds in its core DTH business. Much of the erosion is attributed to the popularity of DD Free Dish in smaller towns and rural areas, combined with the accelerating shift of urban audiences toward digital platforms where flexible, on-demand content dominates consumption.

The financial strain is not limited to individual operators but is evident at the sector level as well. According to the Ministry of Information and Broadcasting (MIB), non-tax revenue from DTH services fell to Rs 648.73 crore in FY24-25. This represents a 6.2 percent decline from Rs 692 crore in FY23-24 and a sharper 24.6 percent fall when compared with Rs 859.96 crore in FY22-23. The downward trajectory of revenue highlights the structural challenges the sector faces in monetization.

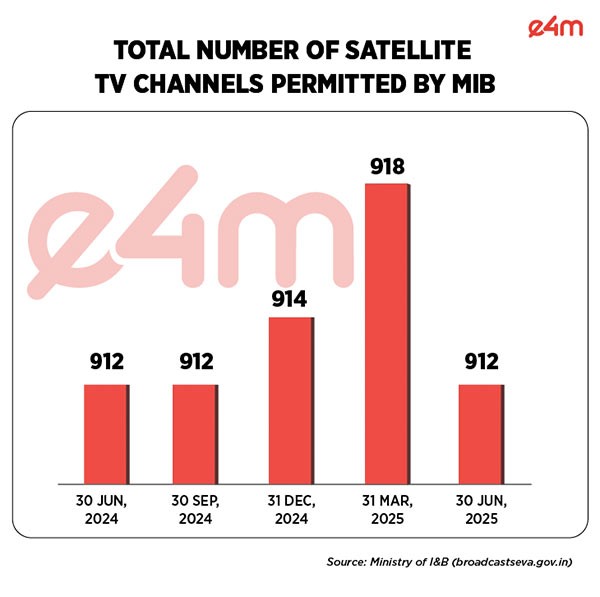

Another telling indicator of stagnation has been the number of permitted satellite TV channels. At the end of June 2024, India had 912 channels. This number remained unchanged by September 2024, rose slightly to 914 by December 2024, and reached 918 in March 2025. However, by June 2025, the count had slipped back to 912, exactly the same as a year earlier. The plateau in channel growth reflects the shifting focus of broadcasters, who are increasingly investing in digital-first content strategies rather than adding new linear TV channels, where returns appear limited.

Taken together, these figures paint a picture of a sector at a critical juncture. The period from June 2024 to June 2025 has been marked by a steady erosion of subscribers, a flattening of channel growth, and growing financial stress for leading operators. Market leaders such as Tata Play and Bharti Telemedia continue to anchor the industry, but their long-term prospects depend on how quickly they can diversify and adapt. Operators are increasingly experimenting with hybrid set-top boxes that integrate OTT platforms with satellite television, offering bundled services to retain subscribers. Rural expansion remains another lever, given that urban households are adopting connected TVs at a rapid pace.

As consumer habits evolve, with more viewers turning to smartphones, smart TVs, and high-speed broadband to access content on demand, the DTH industry is under pressure to reinvent itself. The next few years are likely to determine whether traditional satellite television can remain relevant as part of India’s media ecosystem, or whether it will be steadily sidelined by digital platforms. What is clear is that the era of unchallenged growth for DTH is over, and the sector must embrace innovation and transformation to arrest decline and secure its place in the country’s evolving entertainment landscape.

Read more news about Television Media, Digital Media, Advertising India, Marketing News, PR and Corporate Communication News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News