PMAR 2026: FMCG largest contributor to TV advertising, spends fall 4%

According to the Pitch Madison Advertising Report 2026, the data shows that the pressure on television was not limited to one or two sectors

by

by

Published: Feb 24, 2026 6:11 PM | 3 min read

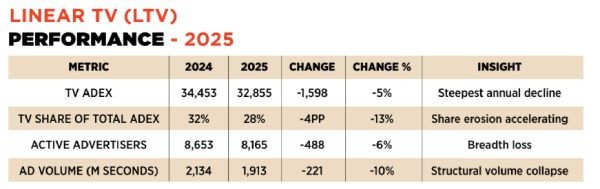

Television advertising in 2025 witnessed a broad-based contraction, with total spends declining 5% year-on-year to ₹32,855 crore from ₹34,453 crore in 2024. The slowdown was structural rather than cyclical, cutting across multiple sectors and reshaping the role of the large screen in media strategy.

As per the Pitch Madison Advertising Report (PMAR) 2026, FMCG, the largest contributor to TV advertising, saw spends fall 4% to ₹15,183 crore, accounting for 42% of the total decline. E-commerce dropped 4% to ₹5,125 crore, contributing 15% to the overall fall. Real Estate declined 5%, Consumer Durables fell 8% marking one of the sharper pullbacks, BFSI was down 4%, Telecom recorded the steepest drop at 10%, and the ‘Others’ category contracted 6%. Auto was the only major category to post marginal growth, rising 1% year-on-year.

The data indicates that the pressure on TV was not limited to one or two sectors. The decline was broad-based, reflecting deeper shifts in media allocation and advertiser priorities.

Despite lower volumes, the strategic role of Large Screen (LTV) is evolving rather than diminishing. Television is no longer positioned as a blanket, year-round GRP engine. Instead, it is increasingly being deployed as a high-attention, high-impact canvas — used selectively when the stakes justify the cost.

LTV is now best deployed around premium genres such as sports, premium GEC programming and high-impact tentpoles, rather than as a 52-week continuity vehicle. Connected TV (CTV) is playing a complementary role by delivering affluent, digitally savvy households with stronger measurability and integration into broader digital journeys.

Deployment is also becoming category-specific. FMCG and Auto are likely to lean on sports and tentpole properties for mass impact. Digital-first brands and BFSI may weight more heavily toward CTV and targeted premium content. Regional brands can leverage regional impact properties and Free-to-Air reach engines. From a systems perspective, Large Screen is increasingly sitting alongside digital video in upper and mid-funnel roles, with print, OOH, radio and performance ecosystems orchestrated around it based on category objectives.

For TV-heavy advertisers, particularly FMCG, the imperative is to tighten TV usage to its most productive roles: major launches, new variants, brand events and a focused set of high-ROI properties such as sports and premium tentpoles. Low-yield, continuity spends are gradually shifting into performance-centric digital, retail media and data-rich CTV environments.

For digital-first advertisers, Large Screen is emerging as a powerful second step rather than a default starting point. It can be layered on top of established digital systems to build cultural impact, strengthen trust and amplify brand-building moments through selective sports and tentpole deployment.

The common thread is selectivity. Advertisers who continue to treat TV as a year-round default medium may struggle to justify ROI. Those who treat Large Screen as a precision impact tool — combining LTV and CTV while integrating tightly with digital — are likely to extract significantly greater value from every rupee invested.

Read more news about Internet Advertising India, Marketing News, PR and Corporate Communication News, Digital Media News, Television Media News

For more updates, be socially connected with us onInstagram, LinkedIn, Twitter, Facebook YouTube & Google News